Charted: The Global Stock Selloff as Oil Fears Rise

Key Takeaways

- Major global stock indexes have fallen between 5% and 10% over the past month as war rattles the Middle East.

- Energy market disruptions—especially around the Strait of Hormuz—have become a central driver of volatility.

- European and Asian markets saw deeper declines than U.S. equities, reflecting heightened exposure to energy shocks.

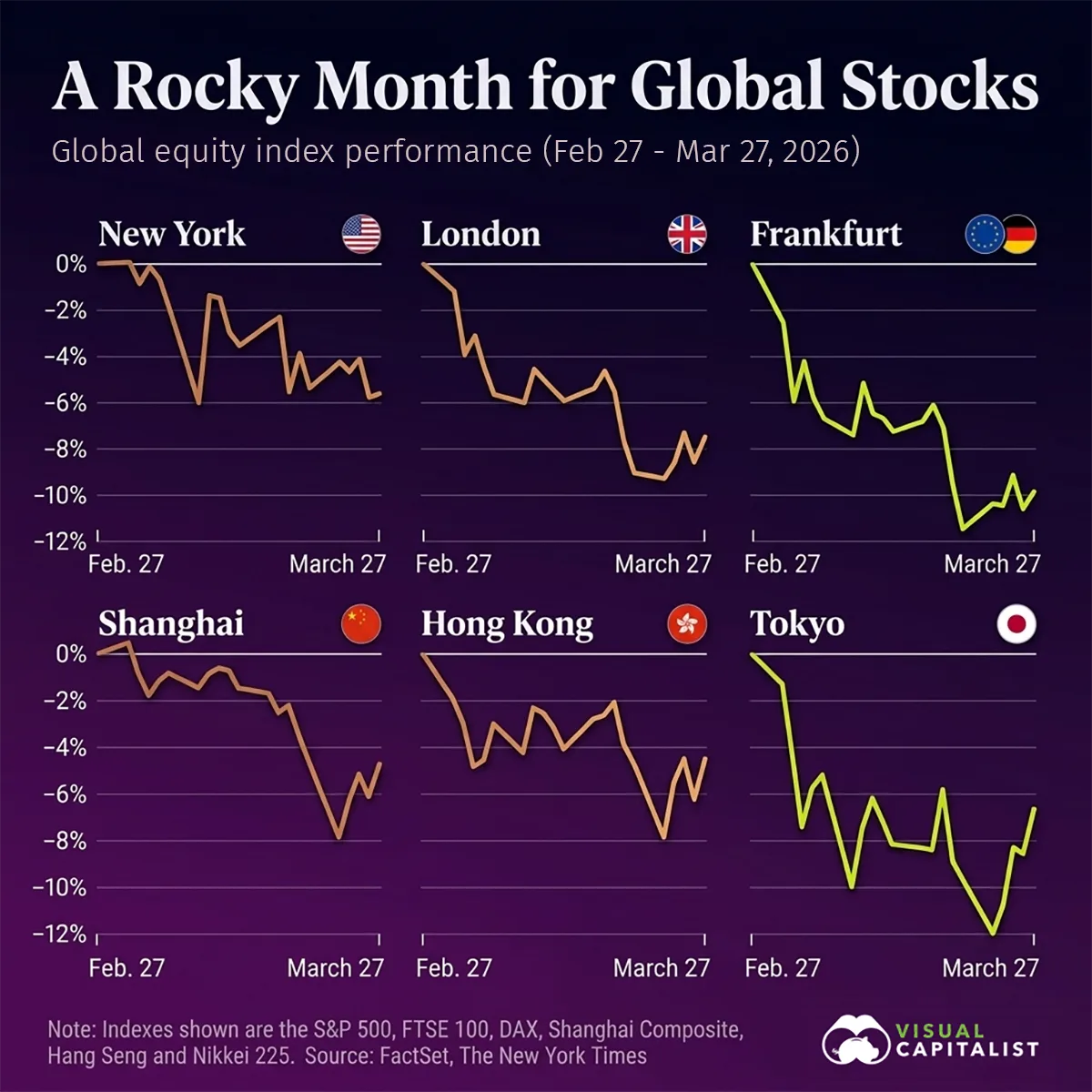

Global equities had a turbulent month as markets reacted to the economic fallout from the ongoing Iran war. According to FactSet data via the New York Times, investors grappled with rising uncertainty, supply disruptions, and the growing risk of a broader regional conflict.

Below, we break down how major stock indexes performed over the past month.

| Index | Location | Monthly Low | Decline (Feb 27 to Mar 27, 2026) |

|---|---|---|---|

| S&P 500 |  |

–6% | –6% |

| FTSE 100 |  |

–9% | –8% |

| DAX |  |

–11% | –10% |

| Shanghai Composite |  |

–8% | –5% |

| Hang Seng |  |

–8% | –5% |

| Nikkei 225 |  |

–12% | –7% |

Across the board, markets declined, with Frankfurt and Tokyo among the hardest hit. While New York saw relatively milder losses, nearly every index ended the period firmly in negative territory.

Energy Markets at the Center of the Storm

At the heart of the selloff is energy. The Iran war has intensified concerns over oil supply, particularly as attacks on infrastructure and shipping routes threaten global flows.

The Strait of Hormuz—a critical chokepoint for roughly a fifth of global oil shipments—has emerged as a major flashpoint. Any disruption here has immediate ripple effects across energy prices and investor sentiment.

Rising oil prices have compounded inflation concerns, forcing central banks and investors alike to reassess growth expectations. As well, institutions like the IEA are warning of a “major threat” to global growth and economists already flagging downward GDP revisions in energy-importing regions.

Why Global Markets Are Reacting Differently

Not all markets have responded equally. European indexes like Frankfurt have seen sharper drops, reflecting the region’s heavier reliance on imported energy. Similarly, Asian markets, particularly Japan, have shown heightened sensitivity due to energy dependency and trade exposure.

Meanwhile, U.S. markets have been somewhat more resilient, supported by domestic energy production and relatively diversified economic drivers.

Still, volatility remains elevated across all regions, with investors increasingly pricing in geopolitical risk.

Investor Uncertainty and What Comes Next

Beyond energy, the broader concern is uncertainty. Markets tend to dislike unpredictability, and the evolving nature of the Iran conflict, combined with risks of escalation, has made forecasting particularly difficult. Notably, many analysts had entered 2026 expecting double-digit gains for the S&P 500, making the conflict a significant curveball to those early-year projections.

Investors are closely watching for signs of stabilization, whether through diplomatic developments or improved security around key infrastructure. Until then, markets are likely to remain sensitive to headlines, especially those tied to energy supply disruptions.