Water and energy are inextricable. You can't produce energy without water (for cooling, for processing, for steam), and you can't treat or move water without energy. They're the twin inputs to practically everything industrialized societies do.

But while energy has captured the attention, water has remained, as Echo River Capital's Peter Yolles puts it, "underinvested and overlooked."

That's starting to shift. Data centers are getting pushback on water consumption. Semiconductor fabs are facing hard questions about ultra-pure water supply and wastewater circularity. Layer on intensifying climate risks, from extreme heat and drought to increased storm frequency and intensity. There's not enough water where you need it, too much where you don't, or not good enough quality.

And as the infrastructure to handle it, much of the water infrastructure in the West has reached or surpassed maturity — in the US, subsurface assets were built to a ~40-year useful life, and the country largely stopped investing in them at the end of the 1970s. Meanwhile, in the Global South, much of it hasn't been built at all. It’s no surprise that the critical investment gap is expected to grow from $94bn in 2024 to $146bn by 2043.

To help make sense of the scale of the problem — and what can be done — Sightline Climate released a new Water Sector Compass for clients, a primer that covers the sector’s full value chain, market structure and dynamics, regulatory landscape, cost and performance benchmarks, key players, and more. This gives investors and corporates a quick-start framework for understanding where the opportunities and risks sit.

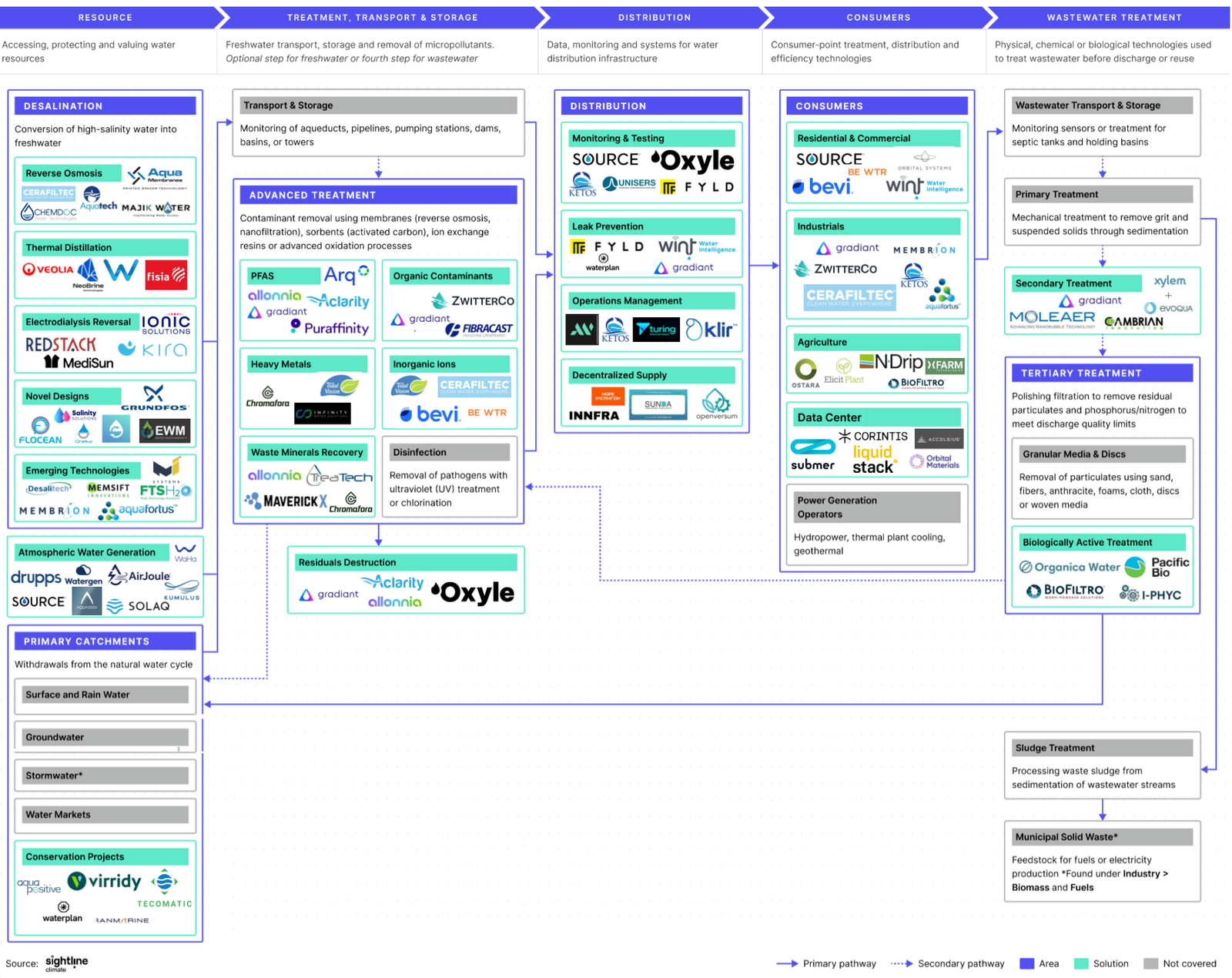

How the water sector works

The water value chain spans five broad segments, each with distinct technology gaps and investment dynamics.

- Resource covers how water is accessed and valued: desalination, groundwater pumping, atmospheric generation, and the emerging water markets that attach financial instruments to supply.

- Treatment and storage handles contaminant removal and transport, from advanced filtration for PFAS and heavy metals to the pipelines, pumping stations, and reservoirs that move and hold clean water.

- Distribution operates as an infrastructure layer: monitoring water quality, preventing leaks in aging pipe networks, and managing operations across mature areas (billing, metering) to new ones (digital twins, etc).

- Consumers span residential, commercial, industrial, and agricultural end users, each with different efficiency and reuse challenges; data centers are a fast-growing category here, driven by cooling demand.

- And wastewater treatment closes the loop, cleaning water for discharge or reuse through primary, secondary, and tertiary treatment processes, plus sludge processing and biosolids recovery.

The case for investing in water, from Burnt Island Ventures and Echo River Capital

Water represents roughly $12 trillion in global annual economic activity, but fragmentation and inefficiency can hold back innovation in the sector. The US alone has 88,000 utilities, most serving fewer than 500 people. Non-revenue water averages ~30% of supply domestically and exceeds 50% in some cities. Reuse rates sit below ~15% in the US and Europe (varying by industry and region), but in Singapore and Israel, nearly 100% of water is collected and treated.

And yet, among the more than 1,000 investors who have made bets in the water space over the past decade, only about 5% have done more than one deal. The dedicated water tech investor ecosystem is still small, a handful of specialist funds collaborating informally to build out a capital stack across stages. We spoke to two of them from both sides of the spectrum to hear why they’re bullish, and what’s bubbling up for them.

Tom Ferguson, Burnt Island Ventures

Tom's thesis is based in physics: As global temperatures have crossed 1.5°C, hydrological disruptions have accelerated sharply. "Everything that we have put together – from where we live to where we've chosen to build – is predicated on the availability of water,” he says. “And we've rolled a hand grenade into the middle of that stasis."

That broken stasis creates the opportunity: new infrastructure being built and old infrastructure being replaced, at the same time. "We have not only permissive pricing, but we've got a $1.6 trillion market in both capex and opex, with Overton windows opening all over the place."

Crucially, the founders have arrived. "In 2020, that's exactly what we finally had — a critical mass of really smart people starting to build companies within water." Burnt Island saw 928 companies last year to make eight investments, Tom said, and is now raising a growth fund alongside a second seed fund, because the companies that were seeded around 2020 have, "as if by magic, built the companies that they said they would." Just as there was no dedicated Seed fund when those founders first emerged, there's no dedicated growth fund for them now, so Burnt Island is building one.

On willingness to pay, a common concern in the space, Tom’s blunt: "There is nothing wrong with water's willingness to pay. None." Large utilities have massive operating budgets, like LADWP's, which is in the billions annually. "If you give those people a really good excuse to lift it out of one bucket of spending and just drop it into another, they're going to do it." The key is founders who can diagnose the pain, build the product, and navigate the go-to-market. Selling to utilities has a reputation as impossible, but Tom calls that "utterly garbage. Once you're in, they never uninstall you."

Looking ahead, Tom sees radical decentralization on both the drinking water and wastewater sides, a transformed desalination capacity, and water becoming a larger input cost for businesses – potentially more expensive than energy in parts of central and southern Europe within 15 years. On the financial side, he expects water to be separated from industrials and treated as its own portfolio category: "The economic behavior of companies that derive their revenues from water actually function very differently relative to the business cycle." Private equity deal activity in water has already increased 7x since 2021, and more generalist funds will build water expertise, "probably by hiring people in."

Peter Yolles, Echo River Capital.

Peter has been in water for over 30 years. He doesn't think of water as an industry. He thinks of it as an investment lens, an input into energy, food, chemicals, transportation, human health, and everything else. "If climate change is a shark, then water is its teeth."

Echo River's thesis is built around solving the three Ds. Digitize: water is analog, unlike electricity which is natively digital. Converting water information into usable data is necessary for managing any of it. Decentralize: the future of new water systems will be largely on-site supply and recycling, moving off the high cost of connecting to centralized grids. Decarbonize: about 10% of global greenhouse gas emissions come from human management of water. Half from moving, heating, and treating it in the built environment, half from direct emissions of superpollutants like methane and nitrous oxide in irrigated agriculture, reservoirs, and desiccated wetlands.

Where Peter gets most animated is decentralization. He envisions buildings and developments that are off-grid for water from day one. "If we combine atmospheric water harvesting with water recycling and low-flow appliances, we're almost to the point where we can get to self-sufficient or even water-positive industrial, commercial, and residential developments."

On desalination, Peter sees three vectors: seawater reverse osmosis (15,000 plants already installed globally, with Israel planning to triple capacity over 15 years), brackish groundwater desalination (critical for new development in Texas and similar regions), and produced water treatment from oil and gas operations.

Peter's vision for the next decade and a half: "How do we live in an era of water abundance rather than water scarcity? That's what I think we'll achieve in the next 10 to 15 years." A world where data centers produce water instead of consuming it, and water-stressed communities welcome development rather than fearing it.

We're overflowing with gratitude to Tom Ferguson from Burnt Island Ventures and Peter Yolles from Echo River Capital for their support on this piece.

Sightline Climate clients can access the full Water Sector Compass on the platform. Not a client yet?

Sightline Climate runs CTVC. Not a subscriber yet?