Plastic has become indispensable to modern life, yet the way we manage it tells a different story. Despite a growing focus on circularity, only 9% of plastic waste is ultimately recycled and less than 10% of global plastic production in 2022 came from recycled material, underscoring the world’s continued dependence on virgin fossil-based plastics. The rest largely ends up incinerated or in landfill.

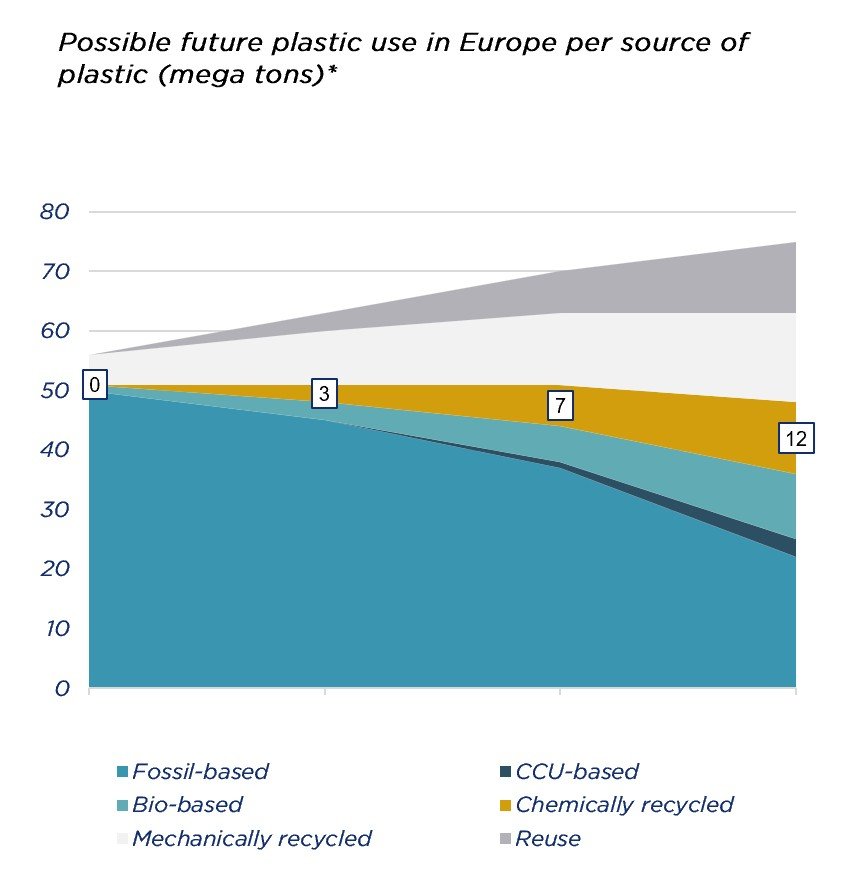

The gap between ambition and reality is stark. Global plastic consumption continues to rise, while recycling systems struggle to keep pace. Mechanical recycling cannot process all waste streams, leaving substantial volumes without a viable end-of-life solution. From an impact perspective, the circularity loop should be as short as possible, with reduction and reuse taking priority. But where these options are unavailable, a critical question arises: can chemical recycling truly deliver at scale?

Drawing on direct experience financing circular economy businesses through the Colesco Circular & Climate Credit Impact Fund (C⁴IF), one thing is clear: while chemical recycling is not a silver bullet, it has an important role to play within the broader plastics recycling ecosystem alongside mechanical recycling and more advanced technologies like dissolution or solvolysis.

The Limits of Mechanical Recycling

Mechanical recycling is effective for certain thermoplastics, particularly when waste streams are clean and homogeneous. However, this is rarely the case in practice.

Mixed plastics, multi-layer packaging and contamination pose significant technical and economic barriers. Even when mechanical recycling is feasible, achieving virgin-grade quality, especially for contact-sensitive applications, remains difficult. Consequently, mechanical recycling addresses only a fraction of total plastic waste streams, while the remainder, particularly contaminated and mixed plastics, is still predominantly incinerated.

This gap highlights the specific role that chemical recycling can fulfil.

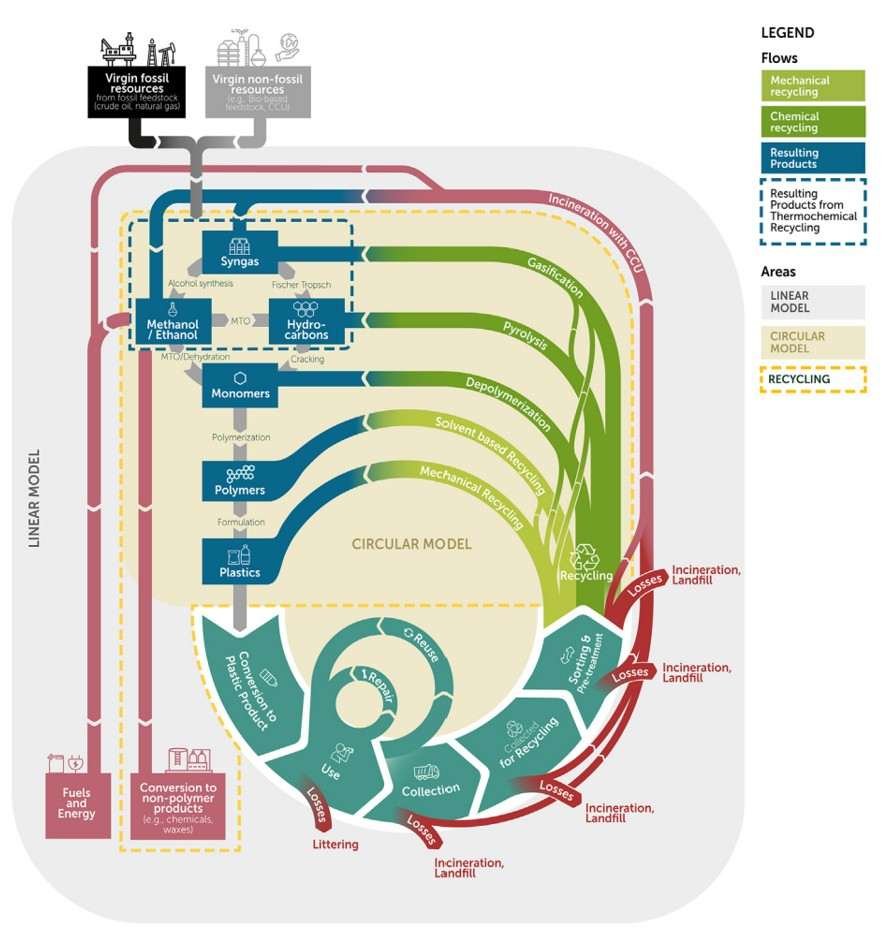

Picture source: Ragaert et al. (2023) – Clarifying European terminology in plastics recycling

Why Pyrolysis Is Leading the Way

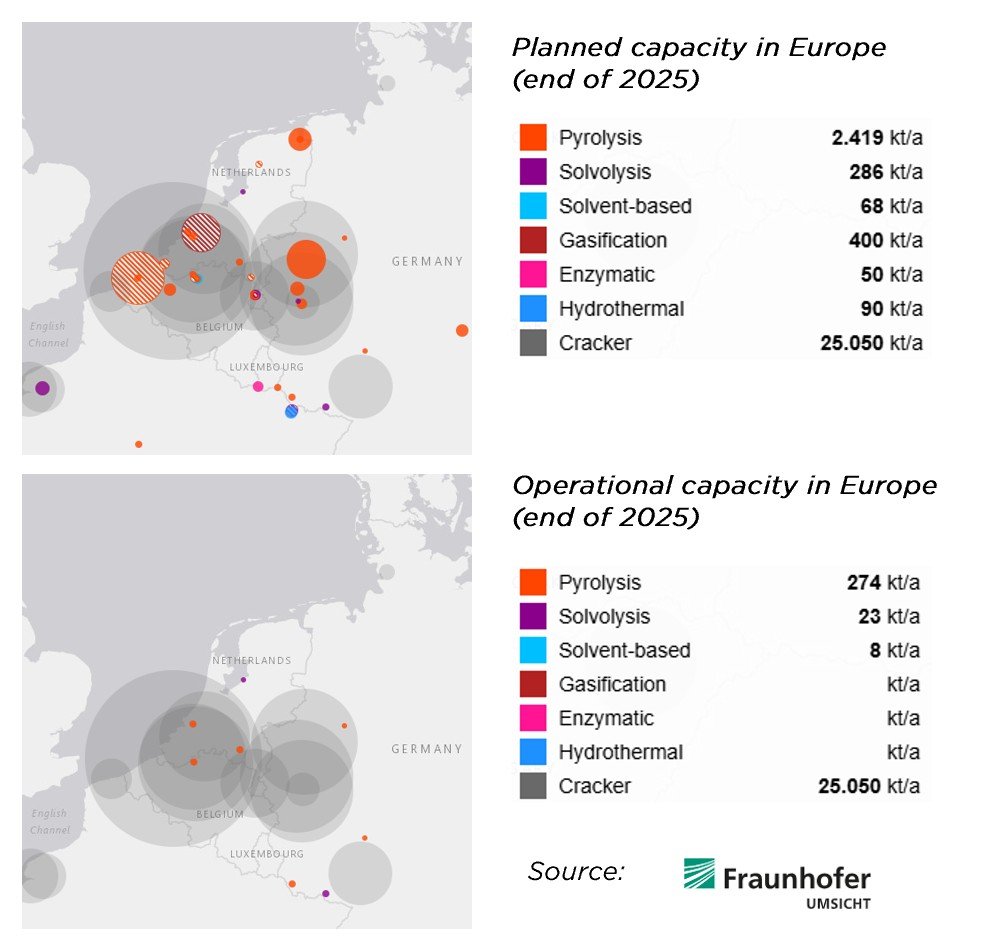

Of the chemical recycling technologies currently being developed, pyrolysis is generally regarded as one of the most commercially mature, although the sector remains at a relatively early stage of industrial scale-up. According to nova-Institute research, around 80 pyrolysis technology providers have been identified globally, compared with approximately 24 solvolysis providers, with pyrolysis facilities also operating at materially larger scale. Individual plants are already reaching capacities of around 40,000 tonnes per annum, while solvolysis facilities are typically much smaller. This scale advantage underpins a growing view that pyrolysis could serve as an important complement to mechanical recycling for mixed plastic waste streams that are otherwise difficult to recycle.

The process works by heating plastic waste in the absence of oxygen, breaking it down into pyrolysis oil, a feedstock that can be used in naphtha crackers to produce new chemicals and plastics. For the fractions and applications mechanical recycling cannot process, pyrolysis is increasingly seen as a missing link in reducing what ultimately ends up in incineration.

Europe is at the forefront of pyrolysis development, with several commercial-scale facilities under development and clusters emerging in port areas and chemical parks mainly in the Benelux region and Western Germany. These locations benefit from proximity to existing petrochemical infrastructure, enabling more efficient integration into established value chains. For example, Colesco finances Xycle through C⁴IF. Xycle is currently constructing its first industrial-scale plant in the Port of Rotterdam. The facility will supply output to Dow, which operates several nearby plants. The number of planned projects significantly exceeds those already operational, though even combined, capacity is unlikely to meet accelerating demand.

Regulation Is Accelerating Demand

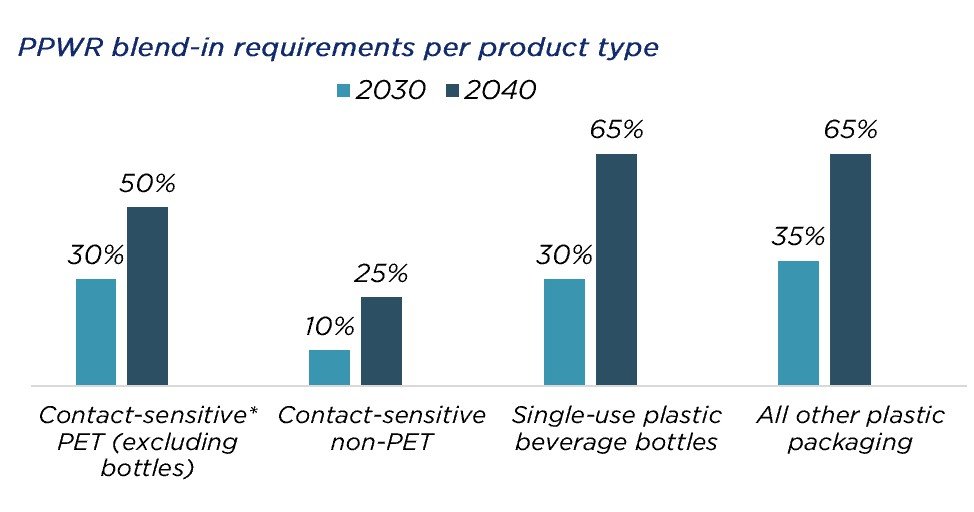

Policy is a major driver of this momentum. The European Union’s Packaging and Packaging Waste Regulation (PPWR), which entered into force in February 2025, sets mandatory recycled content requirements, particularly for packaging. By 2030, once the PPWR is fully phased in, compliance with EU regulation is expected to require over 5 million tonnes of chemically recycled plastic annually in Europe, with demand set to rise further towards 2040.

Supply, however, is lagging. Even with rapid growth, chemical recycling capacity in Europe is projected to reach only about 3.4 million tonnes per year by the end of the decade.

While demand for recycled content is increasing, the market remains in an early stage of development. Some long-term offtake agreements have been signed at premium prices, although pricing transparency remains limited and commercial conditions continue to evolve.

Recent developments in the sector also highlight that scaling chemical recycling is far from straightforward. Several projects across Europe have faced operational, financing and commercial challenges, reinforcing the importance of technology validation, feedstock security, reliable offtake arrangements and disciplined project execution.

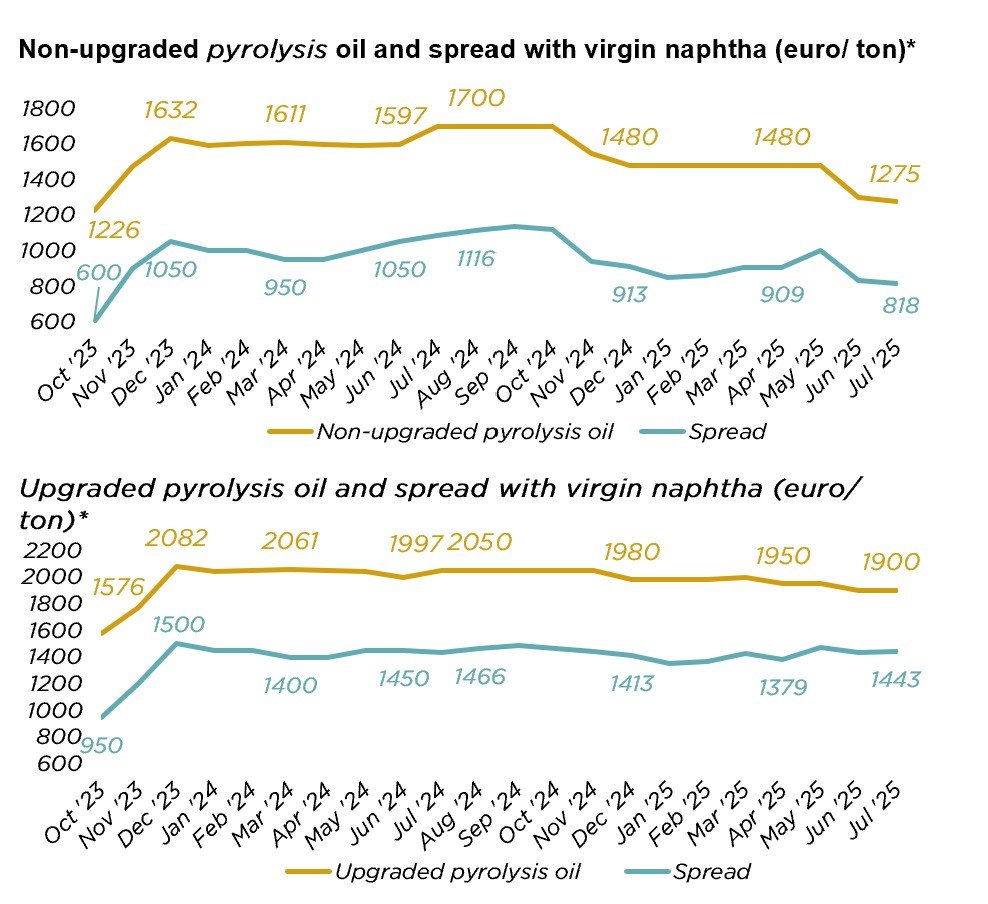

Economics: Attractive but Uncertain

Pyrolysis oil currently commands high prices, often at a premium to fossil-based alternatives. However, the market remains relatively opaque. Prices vary depending on feedstock and processing quality and there is no standardised benchmark. Furthermore, these premiums are highly dependent on recyclers being able to deliver on-spec materials.

Source: ICIS

While current market conditions are favourable, long-term certainty is less clear. Some offtakers are cautious about committing beyond 2030, reflecting uncertainty around regulation, technology maturity and future cost competitiveness. Petrochemical companies and brand owners are delaying investment decisions and large offtake commitments while the details of PPWR are still under finalisation and fines for non-compliance remain unknown. However, brand owners are expected to push for compliance to minimise reputational risk, driving increased demand for the offtake of recycled contents up the value chain.

Feedstock as a Bottleneck

One of the most critical challenges is securing consistent feedstock. While mixed plastic waste is available in large volumes, ensuring consistent quality and reliable supply is considerably more complex. With pyrolysis processes sensitive to feedstock composition, feedstock quality is essential to ensure on-spec output.

In the Netherlands, for example, mechanical recycling capacity has fallen in recent years, which may limit the availability of pre-sorted waste streams. At the same time, competition for suitable feedstock is intensifying as additional pyrolysis projects become operational.

To manage these risks, companies are pursuing long-term supply agreements, investing in sorting infrastructure and developing technologies capable of processing more variable feedstock. Even so, feedstock security remains a significant obstacle to scaling the industry.

Financing the Scale-Up

Scaling chemical recycling requires significant capital. Projects are infrastructure-intensive, with long development timelines and regulatory uncertainty. This makes financing challenging.

Many projects fall into a gap between venture capital and traditional project finance, too large and capital-intensive for the former, yet not sufficiently de-risked for the latter. As a result, access to capital has become a critical bottleneck in the development of chemical recycling projects.

Specialised investors, including impact credit funds, may play an important role in bridging this financing gap by providing flexible, long-term capital tailored to the risk profile and development timelines of circular economy infrastructure.

Not a Silver Bullet, yet a Necessary Part of the Solution

Chemical recycling does not replace the need to reduce plastic consumption, enhance mechanical recycling, or develop advanced recycling technologies. It also comes with its own distinct environmental and economic trade-offs.

However, chemical recycling addresses a segment of plastic waste that would otherwise be incinerated, thereby filling an essential gap within the waste management system.

The next decade will be critical. Regulation is driving demand, technology is advancing and early projects, particularly in the Netherlands, show that progress is possible. A growing number of early adopters are constructing and operating commercial-scale plants, helping to test both the technical feasibility and economic viability of scaling these technologies. Whether the sector can ultimately scale in a commercially sustainable way will depend on continued technological progress, supportive regulation, stable end-market demand and access to long-term capital. Without sufficient investment and coordinated action across the value chain, chemical recycling risks falling short of its potential.

Chemical recycling isn’t a silver bullet, but in a world where plastic demand continues to grow, and achieving true circularity at scale remains challenging, its necessity is growing. While pyrolysis alone cannot close the loop, chemical recycling has a clearly defined role within the broader system.

To continue the conversation around scaling circular technologies, Ward Heij, Business Development Manager at Colesco Capital, will be speaking at Bio Innovations Europe which takes place on 10–11 June in The Hague.

Ward will join a panel discussion hosted by the Bio-based Industries Consortium (BIC) focused on addressing the financing gap facing Europe’s next generation of biorefinery scale-ups. The event brings together industry leaders, investors and policymakers to explore how innovative technologies can move from demonstration to commercial deployment. View the full agenda here.

The post Closing the Plastics Loop: Can Chemical Recycling Deliver on the Promise? appeared first on World Bio Market Insights.