By Abigail Hunter, Executive Director, SAFE’s Center for Critical Minerals Strategy; Skip Estes, , Director, SAFE’s Government Relations; and Zoe Oysul, Policy Manager, SAFE’s Center for Critical Minerals Strategy

Most U.S. policy to address our dependence on China for rare earths and permanent magnets has chipped away at the problem one link at a time. The Magnets Value Chain Support Act takes a different approach: establishing production incentives across the entire permanent magnet supply chain, from mining and refining through to the motors and defense systems that depend on them. Introduced on June 9th by House Select Committee on China Chairman John Moolenaar (R-MI) and Ranking Member Ro Khanna (D-CA), the bill establishes a new Section 45BB tax credit supporting domestic rare earth oxide production, magnet metal and permanent magnet manufacturing using domestic and partner country inputs, and an end-use credit for manufacturers that purchase U.S.-produced permanent magnets—covering rare-earth-based and rare-earth-free magnets alike.

Permanent magnets are required for myriad defense and civilian applications due to their extremely strong, naturally generated magnetic fields and heat resistance. For example, the energy and transportation sectors rely on permanent magnets for electric generators, sensors, power steering systems, electric motors, and transformers. Permanent magnets also enable defense technologies like precision-guided munitions, aircraft electrical systems, missile defense systems, and smart bombs.

Unfortunately, the United States is over 90% import reliant on China for permanent magnets and their material supply chains—a country that not only dominates production along various supply nodes but is also the largest source of demand, giving it unparalleled influence over the global market. China has already used its dominant position and global overreliance on imports as a tool of geopolitical manipulation. In April 2025, China restricted export of permanent magnets and materials. These export restrictions were so dire, U.S., European, and Japanese auto manufacturers scrambled to find alternative sources, with some even halting production.

How does this compare to existing rare earth policies?

The Magnet Value Chain Support Act fills a gap in rare earths policy. While the current Section 45X production tax credit supports certain separated and refined rare earth materials that meet statutory purity requirements, it provides little support for the downstream steps where much of the value is created. In fact, the Inflation Reduction Act that created Section 45X never once used the word “magnet”—its eligible components run from solar and wind parts to battery cells and critical minerals, but stop short of the magnets some of those eligible minerals ultimately become. We need to support the development of the demand for processed rare earths, especially as new upstream minerals projects receive support from the U.S. government week after week. These refined materials need a domestic market to flow into; without one, efforts to decrease our vulnerabilities will fall short.

Overview of the incentives

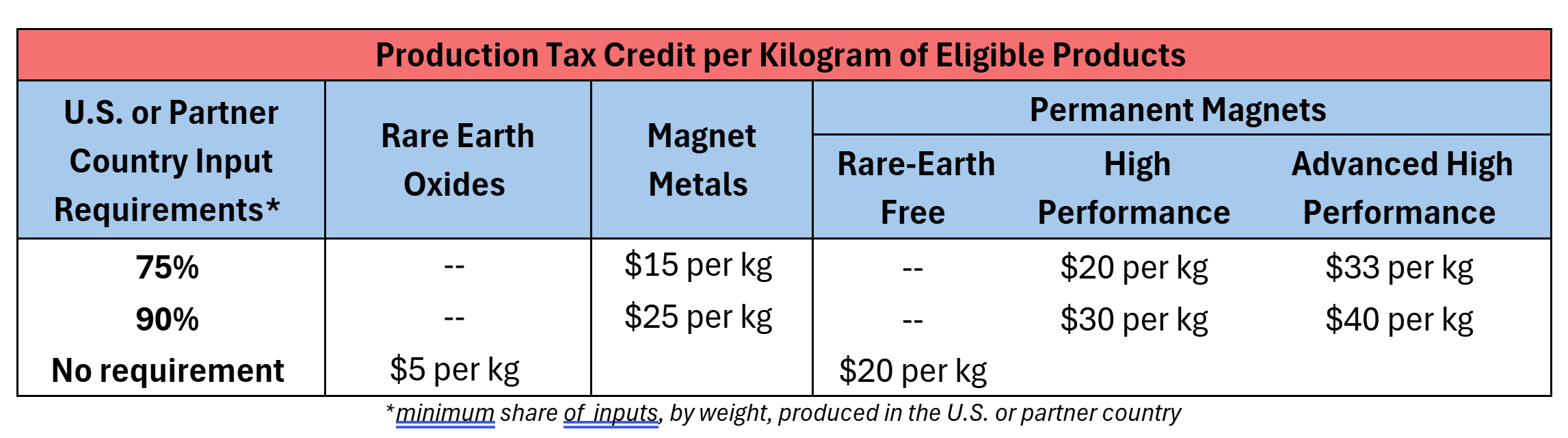

The Magnets Value Chain Support Act establishes new production tax credits, available through the end of 2038, across multiple stages of permanent magnet manufacturing, while encouraging sourcing from the United States and trusted partners. The bill also takes a technology-neutral approach by extending incentives to rare earth-free permanent magnets.

To qualify for the credits, producers of magnet metals and permanent magnets must source a minimum share of their direct inputs from the United States or partner countries. The value of the credit increases as a greater share of qualifying inputs are sourced from these preferred sources. There are no preferential sourcing requirements for rare earth oxides and rare-earth free permanent magnets. However, the bill requires eligible rare earth oxides to be produced under a binding offtake agreement for downstream processing into magnet metals, alloys, or permanent magnets in the United States or a partner country. In the case a product is eligible for both the proposed Section 45BB and the existing Section 45X credits, only one tax credit may be claimed.

Additional design features include:

- Prohibited foreign entity (PFE) restrictions: Eligible products may not be produced by PFEs, produced using inputs sourced from PFEs, or sold to PFEs. The bill allows producers to obtain a 90-day waiver if no commercially viable alternatives for material inputs are available. For rare earth oxide production, the bill also importantly aligns with PFE restrictions under Section 45X by prohibiting the use of technology or services from PFEs in the separation process.

- Stacking: Vertically integrated producers have the ability to “stack” production tax credits if they produce magnet metals, rare earth oxides, or metallic precursors for use in permanent magnet production. For example, if a firm produces rare earth oxides, processes them into magnet metals, and then manufactures such metals into a permanent magnet, they can claim all three production tax credits included in this bill. This provision incentivizes a comprehensive permanent magnet supply chain by encouraging companies to invest in all stages of the manufacturing supply chain.

- Transferability: Like 45X, the new credits are transferable, improving access to financing for new market entrants and early-stage manufacturers that may not yet have sufficient tax liability to fully utilize the credit.

Finally, the bill strengthens demand for domestic permanent magnets by rewarding manufacturers of motors, generators, and other high-performance equipment that use them. The credit is equal to an applicable percentage of a taxpayer’s qualified expenditures on domestically produced permanent magnets. Eligibility is limited to strategic applications such as data storage systems, robotics, unmanned aerial vehicles, munitions, and other critical industrial, energy, and defense technologies. Unlike the other proposed credits, which remain available through the end of 2038, this domestic magnet input usage credit phases down over time. The table below summarizes the applicable percentages and phase-out schedule.

Understanding the Preferential Sourcing Provisions

“Partner countries” covered under the preferential sourcing provisions include North American countries (Canada and Mexico), NATO allies, Japan, South Korea, and Australia. In addition, the Secretary of the Treasury, in consultation with the Secretaries of War and Commerce and the U.S. Trade Representative, may designate specific facilities in non-partner countries as qualifying sources.

Additional flexibility is provided for rare earth oxide production. Unlike magnet metal and permanent magnet production, rare earth oxide production is not subject to preferential sourcing requirements. The credit is fixed at $5 per kg regardless of the origin of upstream feedstocks. This reflects a simple reality: the rocks are where the rocks are. While the bill reserves its stronger sourcing preferences for the later production stages, where location decisions are more responsive to policy incentives, domestic rare earth oxide producers retain the flexibility to source concentrates from around the world without requiring facility-specific designations.

The bills’ approach toward preferential sourcing is consistent with broader U.S. efforts to diversify rare earth supply, including the U.S. International Development Finance Corporation’s support for rare earth mining projects in Brazil, South Africa, and other jurisdictions outside the “partner country” list.

Conclusion

Permanent magnets provide the foundation for modern industries, like electric motors, power generation, and advanced weapons system that the American economy and national defense rely on. The United States’ current overexposure to Chinese manipulation place these at risk, and China has already demonstrated the ability to leverage this geopolitical power. To maintain strategic independence, the United States must develop alternative sourcing options for permanent magnets and precursor materials. The Magnets Value Chain Support Act is the next step in effective policy to encourage a domestic supply chain from mine to magnet.

The post Magnet Supply Chains Attract Bipartisan Focus appeared first on The Fuse.