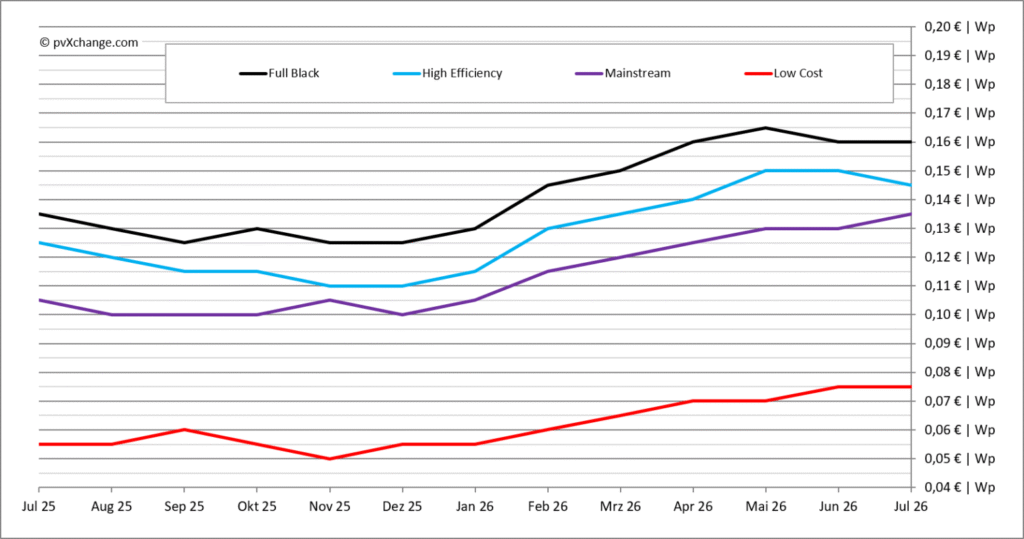

For the second time this year, solar module prices across the various technology classes have not increased across the board compared with the previous month. Price movements for full-black and low-cost modules were negligible, while changes in other segments were also marginal. Availability across most power classes has improved significantly again. The only exception is back-contact modules with efficiencies above 24%, where demand continues to exceed supply, resulting in shortages in the higher power categories. However, as this technology still represents only a small share of the overall market, price developments in this segment have little impact on the overall index.

The niche status of back-contact cells and modules is unlikely to last much longer. Nearly all major Asian manufacturers are developing the technology and preparing to launch corresponding products on the European market in the coming months. This trend was evident at this year’s Intersolar trade fair in Munich in June, where almost every leading manufacturer presented a mass-production module based on back-contact cells. Interest in these products is particularly strong in the residential rooftop segment, as they combine high efficiency with an almost entirely black appearance.

However, minor patent disputes over back-contact module production processes continue among manufacturers, most of which are based in China. In addition, many companies are reluctant to convert production lines that have only recently been optimized for TOPCon technology, as such changes would require significant modifications and additional investment. As a result, only three Chinese manufacturers—AIKO, Longi, and TCL, which remains relatively unknown in Europe—are currently producing back-contact modules at scale. Other brands rely on these companies to varying degrees for OEM production. TCL appears to be the only manufacturer actively seeking to license its patents to other companies rather than focusing solely on white-label manufacturing.

Against this backdrop, many manufacturers are already looking toward the next stage of solar cell and module development: perovskite technology. The material offers potential for both transparent modules in building-integrated applications and high-efficiency tandem modules that combine perovskite layers with crystalline silicon cells for rooftop and utility-scale installations. The underlying physics suggests efficiency levels above 30%. However, manufacturing remains challenging, and the long-term stability of perovskite layers has yet to be fully demonstrated. Under certain climatic conditions, still poorly understood effects can accelerate degradation, complicating the transition to mass production.

Nevertheless, perovskite technologies were prominently showcased at Intersolar and The smarter E, providing a glimpse of future developments in the solar industry. Initial pilot customers are already receiving products from Brandenburg-based company Oxford PV. Its tandem modules, which currently achieve efficiencies slightly above 25% and are targeting 27% next year, are undergoing extensive field testing and monitoring. Across Europe, numerous research institutes and private companies are also working to advance the technology and prepare it for commercial deployment. The first mass-market products incorporating perovskite technology are expected to become available by late 2027 or early 2028 at the latest.

Despite rapid progress, significant challenges remain. Although the pace of innovation in solar cell variants and module formats has accelerated considerably in recent years, manufacturers must still recover investments in existing production facilities while securing capital for the next generation of technologies. This balancing act is becoming increasingly difficult.

Growing demand for higher-performance module categories—enabled by recent technological advances—is forcing manufacturers to maximize utilization of their production capacities, including their continuously upgraded TOPCon lines. At the same time, production cuts previously introduced to support prices have proven costly, as idle capacity generates financing expenses without corresponding revenue. Such measures are therefore unlikely to remain sustainable over the long term.

As a result, existing production lines must be ramped up and operated at high utilization rates, particularly amid strong pressure to increase output. In a market that is stagnating or expanding only marginally, this is contributing to overproduction and declining prices.

Further price increases are therefore unlikely this year, at least for TOPCon modules. Prices for these products have already stabilized and are showing a slight downward trend. By contrast, strong demand and limited supply for modules based on back-contact cells are expected to support stable or slightly higher prices.

The price gap between modules used in small-scale residential rooftop systems and those deployed in commercial rooftop and ground-mounted installations is therefore likely to widen again.

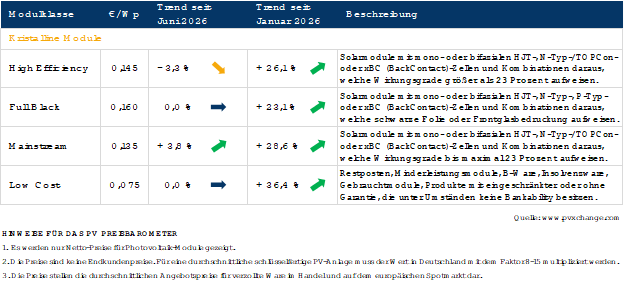

Overview of module price levels by technology for July 2026, including monthly changes (as of July 15, 2026):

About the author: Martin Schachinger has studied electrical engineering and has been active in the field of photovoltaics and renewable energy for almost 30 years. In 2004, he set up the pvXchange.com online trading platform. The company stocks standard components for new installations and solar modules and inverters that are no longer being produced.

The post Rise in solar module prices comes to a halt appeared first on pv magazine Global.