By: Abigail Hunter, Executive Director of SAFE’s Center for Critical Minerals Strategy, and Zubeyde Oysul, Policy Manager for SAFE’s Center for Critical Minerals Strategy

- The G7 has finally put a number on rare earth diversification. Its commitment to cut reliance on any single non-allied supplier below 60% by 2030 is more than another communiqué flourish, but the real test is whether announced projects can be built, commissioned, and operating at scale before the deadline arrives.

- The capacity pipeline is promising, but the middle of the supply chain remains the choke point. New separation projects could put North America and Europe within reach of the target, yet metallization, alloying, magnet production, heavy rare earth supply, and skilled industrial capacity are all racing the same four-year clock.

- Building mines is not enough. Without durable demand for allied magnets and protections against Chinese price suppression, new projects risk becoming the next cautionary tale. The path forward runs through coordinated procurement, allied-content incentives, recycling, and price mechanisms designed to keep viable projects alive when markets get strategically inconvenient.

- Japan’s challenges and Molycorp’s bankruptcy show why diversification cannot survive on ambition alone. Tokyo’s post-2010 push still left it sourcing roughly three-quarters of rare earths from China, while Molycorp’s collapse after prices normalized illustrates the central risk: new supply chains can be strategically necessary and commercially fragile at the same time. We break down how to draw lessons from history to repeat past mistakes in addressing this high-stakes, multilateral game of chicken.

G7 leaders have announced a commitment to reduce reliance on any single non-allied supplier of rare earths and permanent magnets to below 60% by 2030, with an ambition to reach 50% as soon as possible. Released via a joint statement at the summit on June 17 in France, the objective is focused on addressing China’s global market dominance and control of roughly 90% of global rare earth separation and metallization capacity.

The critical minerals space is awash with multilateral agreements and oftentimes vague commitments, so this time-bound, numeric threshold is a welcome development. Reaching the target is challenging but could be achievable — and imperative for the group’s collective security.

The 60% Target: Signal vs. Reality

The 60% by 2030 target gives G7 partners a shared benchmark, enables better coordination, and sends a durable signal to investors and developers who need policy certainty to finance long-lead projects. The global rare earths market is relatively small in comparison to other commodity sectors, so just a few projects can meaningfully shift the market.

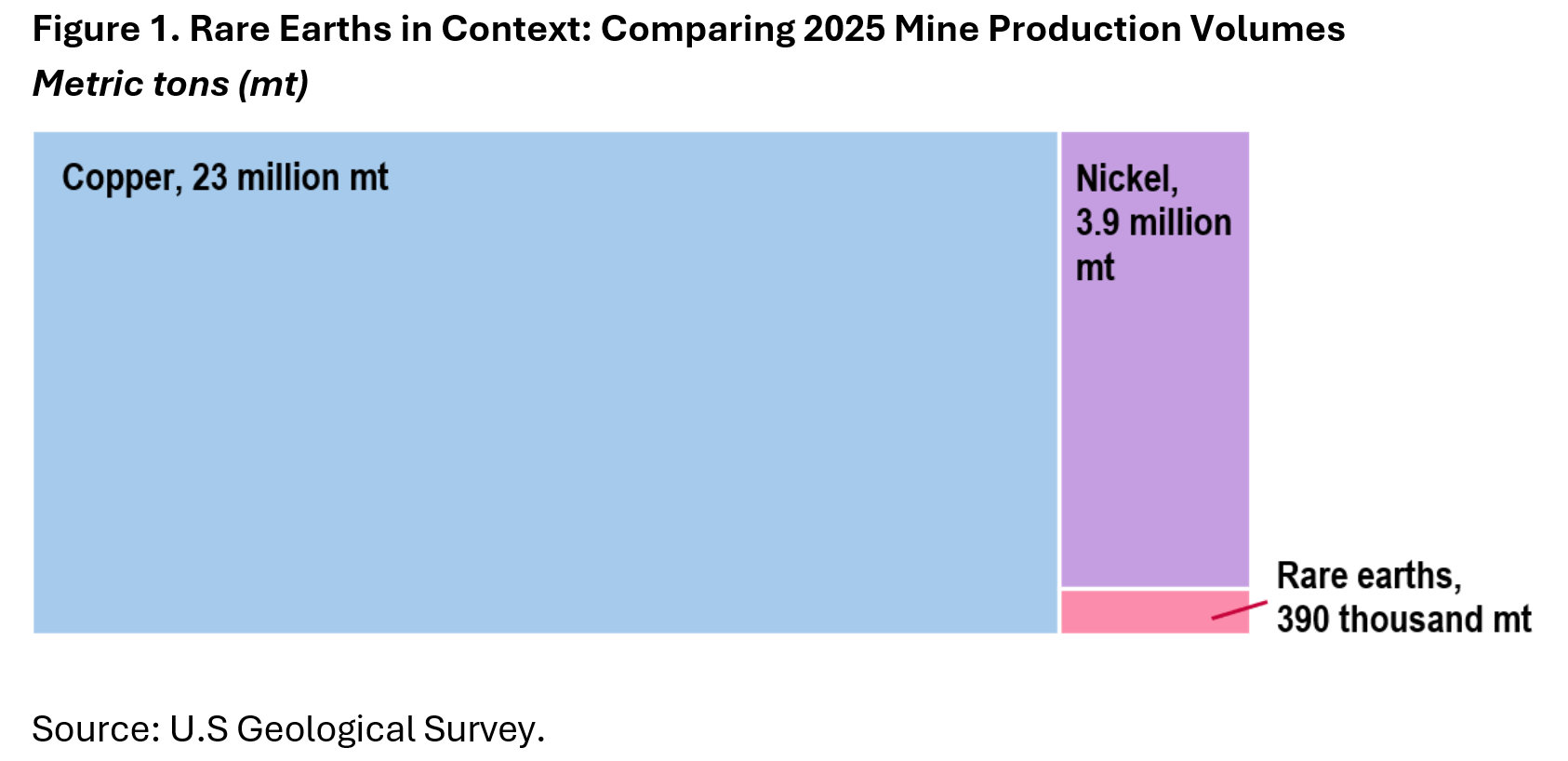

However, there are significant bottlenecks, particularly in separation, metallization, and alloying. The IEA estimates that China accounts for roughly 60% of global mined rare earth production yet controls more than 90% of global refined rare earth output and over 94% of permanent magnet manufacturing. The midstream stages can take years to scale outside of China — timelines may be extended as the West has to simultaneously rebuild “muscle memory” in equipment, process engineering, and skilled labor.

The good news is that necessary projects have kicked off to meet the target. Based on announced rare earth separation projects and offtake agreements that SAFE is tracking, the pipeline of rare earth oxide separation capacity can be broadly sufficient for North America and Europe to achieve the target for magnet rare earths—the key question is if all these projects can be built, commissioned, and ramped within the next four years. If all projects begin operating, average utilization of approximately 50% by 2030 would be sufficient to meet 40% of regional demand. If fewer projects come online, the facilities would need to operate at substantially higher utilization rates.

This aggregate assessment, however, masks diversification challenges for individual rare earth oxides. Benchmark Mineral Intelligence expects China and Myanmar to still account for nearly 80% of global supply of heavy rare earths, specifically dysprosium and terbium into the early 2030s. The scale of the current gap is stark: in Q1 2026, Lynas produced just eight tonnes of dysprosium and terbium combined, while global demand runs into thousands of tonnes annually. MP Materials is expected to have their Pentagon-funded heavy rare earth circuit come online this quarter and start producing heavies later this year. Across the board though, McKinsey projects an overall shortfall of up to 30% in magnetic rare earth supply globally by 2035 unless the rest of the world sharply accelerates production.

Additionally, the announced project pipeline highlights the continued importance of coordinated investments across the value chain. U.S. and European investments in separation capacity total 44 KT (kilotonnes) of separated rare earth oxides, compared with 28 KT oxide equivalent in metallization capacity. The growing consolidation of leading rare earths companies, particularly in the United States through strategic acquisitions, can help better align investments, secure feedstock, and create downstream demand across multiple mine-to-magnet production stages. But it will still require the same companies to simultaneously develop mining, separation, metallization, and magnet manufacturing capacity to achieve the diversification target across the value chain.

What Else is Needed?

Even with significant public support — including the at least $5 billion in U.S. direct federal rare earth commitments and about ~$8 billion combined across G7 members — the timeline is tight. Reuters reported in November 2025 that the U.S. may be on course to meet about 95% of its own demand for magnet-making rare earths (neodymium, praseodymium, dysprosium and terbium) domestically, but that outcome does not necessarily extend to the rest of the G7 and depends on U.S. projects remaining on schedule.

Even with new supply — and this will come as no surprise to our readers — connecting demand remains the real challenge. The G7 needs to simultaneously build a larger base of buyers for rare earth magnets and ensure those buyers have strong incentives to source from non-Chinese suppliers. New mining and refining projects are necessary and have ample challenges, but the more urgent policy lever is demand: creating commercial conditions under which manufacturers have a reason to source outside China.

The most effective approach combines public financing with allied-content incentives, defense-sector procurement mandates, and recycling support. In the United States, the bipartisan Magnets Value Chain Support Act offers a useful model. It would support the full magnet supply chain through production tax credits at multiple stages, with higher credits for producers that source a greater share of inputs from the U.S. or allied countries — a structure that rewards integration rather than just extraction. Downstream incentives for U.S. manufacturers using domestically produced permanent magnets, paired with restrictions on sourcing from prohibited foreign entities, complete the architecture.

Other G7 nations should therefore consider options that emulate existing U.S. defense procurement restrictions that prohibit the procurement of permanent magnets and magnet alloys produced in China, Russia, North Korea, and Iran for defense applications. These Defense Federal Acquisition Regulation Supplement (DFARS) restrictions are set to expand to the upstream to cover the full supply chain from mine to magnet starting on January 1, 2027 (see our separate analysis on the DFARS restrictions and proposed congressional reforms here). While important to secure supply chains for the defense industrial base, defense demand alone is insufficient to justify major investments in new rare earths and magnet production capacity, highlighting the importance of the G7’s diversification target, the need to harmonize defense procurement restrictions, and other policies aimed at commercial markets.

Recycling also deserves attention. It can generate a non-China feedstock stream faster than developing a new mine, and it does not carry the same permitting risk. The challenge is that collection and sorting infrastructure remains underdeveloped, and material recovery technologies need further investment. Incorporating recycling explicitly into G7 diversification strategies — not as an afterthought but as a near-term supply source — would meaningfully accelerate progress toward the 2030 goal.

The bottom line: demand-side pull measures and supply-side investment are complements, not substitutes. A strategy that relies entirely on building new capacity without creating a durable commercial market for non-China supply will reproduce the failures of the past.

Japan’s Case Study Demonstrates Need for Multilateral Efforts

Japan is the most instructive case study available. Following China’s de-facto rare earth export ban in 2010, Tokyo launched one of the most serious diversification efforts any government has attempted — investing in overseas projects, funding R&D, and pushing efficiency improvements to reduce rare earth consumption per unit. Tokyo backed the push with a ¥100 billion supplemental budget dedicated to supply-chain resilience. However, 16 years later, Japan still sources roughly 76% of its rare earths from China.

That is not a failure of ambition. It is a demonstration that no one country can go it alone. Bringing new capacity online required years of patient capital, sustained policy support, and technical assistance to projects that faced cost overruns, operational delays, and a steep learning curve in competing against entrenched market incumbents. When China allowed prices to normalize after the 2010 episode, the commercial case for diversification weakened and investment dried up.

In the face of such market dominance, allied collaboration — pooling resources, sharing technical expertise, and aggregating demand — is necessary. It also reduces the risk of governments funding parallel projects that collectively outpace demand, undermine each other’s commercial viability, and ultimately fail to attract private capital. The G7 coordination platform referenced in the Leaders’ Statement is exactly the kind of institutional mechanism that could prevent that outcome, if it is used seriously.

Beijing’s Response

China is not a static force in this market. The common geopolitical competitor to the G7 retains significant leverage and will not cede market share passively. The obvious tool is the further tightening of export controls on rare earth compounds, metals, and processing technology. Beijing has already moved in this direction, and additional restrictions are plausible, but it would likely strengthen the resolve of the G7 and remind policymakers of the challenge at hand.

The more insidious risk is price suppression. China has the capacity to flood global markets with rare earths and permanent magnets precisely as new non-Chinese facilities approach commissioning, replicating the cycle that contributed to Molycorp’s bankruptcy in the wake of the 2010 episode. Neodymium prices surged from roughly $42/kg to over $283/kg between 2010 and 2011 before collapsing as Beijing eased export controls. Molycorp filed for bankruptcy in 2015. At depressed prices, projects that penciled out at $110/kg NdPr do not survive at $40/kg, and private financing evaporates.

To avoid this outcome, the Pentagon began deploying government-backed offtake agreements and pricing mechanisms designed to insulate emerging producers from market manipulation. The public-private financing package to accelerate MP Materials’ mine-to-magnet expansion includes a 10-year agreement establishing a $110/kg price floor for all NdPr stockpiled or sold. In addition to covering the shortfall whenever market prices fall below that level, the government also offered a guaranteed offtake backstop for all magnets produced. USA Rare Earth and Serra Verde announced a 15-year offtake agreement with price floors for 100% of Phase I production through a special purpose vehicle capitalized by U.S. government agencies. The Pentagon’s $96 million offtake agreement with Lynas also guarantees a minimum price of $110/kg of NdPr. These arrangements are meant to improve project economics by guaranteeing minimum revenue levels and shifting downside price risk from producers to the government.

At an NdPr price of $70/kg, a $110/kg price floor would require approximately $40 million in government support for every 1,000 metric tons of NdPr oxide — roughly equivalent to MP Material’s Q1 2026 sales volume. The short-term costs are modest compared to the economic and national security risks associated with supply disruptions, but government spending can easily balloon as multiple projects rely on similar mechanisms over an extended period. Ultimately, the United States may find itself in a “game of chicken”: how long can China sustain depressed prices, and can the U.S. government maintain support long enough for new supply chains to reach commercial scale? Provisions that allow taxpayers to participate on the upside help reduce the government’s risk exposure. Under the MP Materials arrangement, for example, the U.S. government receives 30% of profits above the $110/kg threshold.

However, U.S. government-directed price supports are likely to remain limited to a small number of projects, rather than serving as a scalable solution for the broader market. These arrangements will support the G7 diversification goal to the extent these companies produce oxides, alloys, and magnets for G7 countries.

At a market-level, the U.S. Trade Representative is pursuing a broader solution through the ongoing plurilateral negotiations with G7+ partners for an Agreement on Trade in Critical Minerals (ATCM). The ATCM seeks to establish a price adjustment mechanism for imported critical minerals to counter market manipulation and prevent artificially low-priced imports from undercutting critical mineral producers in countries party to the agreement. Under such a framework, tariffs or equivalent measures could be applied to materials sold below a designated fair reference price, effectively creating a floor price within the trade zone. Participating countries could continue importing critical minerals from any supplier, including China, provided the material enters the market at or above the reference price. So, these plurilateral agreements are a tool to complement the G7 diversification goal by insulating new projects from market flooding.

The Path Forward

The G7’s 60% target is ambitious but not unrealistic — provided governments treat it as a floor that demands sustained action rather than a headline that substitutes for it. The architecture is clearer than it has ever been: allied coordination to avoid duplication, demand-side policy to create commercial markets for non-China supply, recycling to accelerate near-term feedstock availability, and price-support mechanisms to protect emerging capacity against deliberate market disruption. What has historically been missing is the political durability to see it through. The 2030 deadline creates accountability. Whether governments use it is the variable that matters most.

The post Can the G7 Break China’s Grip on Rare Earths by 2030? appeared first on The Fuse.