Hot off the press, China released its 15th Five Year Plan (2026-2030) earlier today. It comes at a critical juncture for climate, energy security, and … the global balance of power.

Keep in mind, the world cannot decarbonize without China. It is simultaneously the largest emitter and the largest builder of clean energy, installing more solar, wind, and batteries each year than the rest of the world combined. Not to mention, it manufactures many of the key parts behind these technologies for the rest of the world.

Yet, China’s been facing an economic slowdown. Its traditional growth engines – real estate, manufacturing, and infrastructure – have been slowing, with manufacturing margins getting squeezed by years of overcapacity (involution) and global trade barriers. Add on top of that: an aging workforce, capped domestic demand, and most of all, increasingly volatile energy and industrial supply chains (read: Strait of Hormuz).

Despite all this, clean energy in China has been on a tear over the last few years. Clean energy sectors now make up 11.4% of China’s GDP, nearly doubling since 2022. In other words, without clean energy growth, China would have missed its last 5% annual GDP growth target.

As we wrote in China’s electrostate readiness breakdown, “China’s mandate to build clean energy industries has been primarily driven by energy security and economic leadership, not decarbonization”. So it’s no surprise that China’s latest Five-Year Plan (FYP) doubles down on its ambitions to be self-sufficient and a global tech powerhouse. Anything that cuts across both themes – like AI, semiconductors, and clean energy – will be the likely bets. And above all, China is betting on itself: on energy, on tech, on innovation.

How China sets industrial policy: Five Year Plans

China’s Five Year Plans aren’t just planning documents, they’re the CCP’s top-down blueprints for mobilizing capital, talent, and policy over the next half-decade. These plans have underpinned China's rise from post-Cultural Revolution doldrums to superpower status.

In our previous piece on China’s electrostate readiness, we covered how China's motivation (energy security first, industrial leadership second), its engineering-vs.-lawyerly-state divide, and its policy certainty propelled it to the top of clean energy manufacturing ranks. But several of you asked the obvious follow-up: how does China's industrial policy actually work in practice?

Here’s how. There are two uniquely “Chinese characteristics” to its industrial policy.

First, policy is certain and long-horizon.

When the government sets its sights on something, it usually achieves it. In 2015, China unveiled its Made in China 2025 (MIC25) strategy, a ten-year plan to transform the country into a high-tech powerhouse and reduce foreign import dependency. As of 2025, Chinese companies dominate every segment of the solar value chain, make most of the large-capacity batteries that power electric vehicles, and have commanding positions in wind turbines and hydrogen electrolyzers.

The killer combo of longer horizon planning (beyond four-year election swings) and ruthless prioritization means that local governments, businesses, and investors/lenders all have the priority blueprint they need to place, build, and finance their bets – at speed and scale.

However, the same killer combo also has a tendency to overheat industries. Case in point: in 2009, China launched a series of "New Energy Vehicle" (NEV) policies including billions in production subsidies where companies received tens of thousands of RMB for every vehicle produced.Cities like Shenzhen and Hefei offered cheap land, low-interest loans, and industry funds to EV startups. Fast forward to 2025: over 100 Chinese EV companies compete with one another, driving the average profit margin for Chinese autos to 4.4%. In 2026, China switched camps and shifted to an “anti-involution” stance on EVs, setting minimum price floors and removing the EV purchase tax exemption.

Second, China operates like a company more than anything else.

The general secretary of the CCP, Xi Jinping, is the "CEO" with the Politburo functioning as the exec team, using the Five-Year Plan to set their top-down goals every five years. The most promising political leaders are put in charge and rotated through different jurisdictions, with those demonstrating the best performance relative to the FYP’s objectives moving up the ranks of the CCP – just like in a company. So…ironically, despite China being nominally socialist, the governing system embraces the principles of capitalism.

Think of it like a corporate pyramid that acts top-down and bottom-up. The Five Year Plan process starts roughly two years before the plan begins. First bottom-up: each province submits its own five-year research with its own targets (e.g. Anhui province says "we can produce 1 million high-end EVs by 2030”) that informs the national target. During drafting, the government solicits input from millions of private businesses, universities, or public online consultations.

Then top-down: a couple of months before the release, the Central Planning Committee (CPC) will then release their top-down guidelines. For instance, in Oct 2025, the CPC set its recommendations focusing on fostering a “modern industrial system” – aka moving away from cheap low-quality manufacturing towards high-end tech like AI, solid-state batteries, semiconductors, etc. With the official 15th Five Year Plan released today, the targets set for 2026-2030 will now cascade down to China’s divisions of local governments, banks, SOEs, investors, and businesses to figure out how to work together to meet its Five Year KPIs.

Here’s how to think about it: The central government acts as the exec team, the provincial governments as the regional business units, banks and lenders as the finance division, with SOEs and startups like experienced vs new employees. Similar to regional managers, provincial and local governments will assess the Five Year Plan’s goals and set their own objectives based on their region’s unique strengths and advantages. For example, Shanghai may lean into its density of high-talent and finance whereas Inner Mongolia has an abundance of land and sun, and has bet big on net-zero industrial parks featuring massive solar farms and data centers. Many will then develop industry funds in partnership with SOEs or the private sector to incubate these sectors (like government CVCs), or build and lease low-cost factories to attract companies in those sectors.

So therein lies the rub. China’s industrial policy has its faults (like driving involution) but it's a ruthless machine that builds consensus from the top-down and bottom-up. It sets a clear target for local government officials, private sector, and lenders to sprint together. As we all know too well, the maturity curve for climate tech takes years, if not decades. This is the industrial policy machine designed for climate tech and hardtech. The Five-Year Plan gives people an incentive and mandate. The consistency of five-year terms is what makes it work.

What's in the 15th Five-Year Plan

Economic: The lowest GDP growth target in 35 years

Conservative targets. The headline GDP growth target of 4.5–5%, presented as a range for the first time, is lower than the historical 5% benchmark and traditional growth engines (real estate, infrastructure, export manufacturing on thin margins) are slowing down.

Involution: stronger language but unclear enforcement. The plan signals intent to eliminate outdated industrial capacity and avoid destructive overcompetition but it remains a political challenge with heavy industry mostly state-owned and a mixed track record on actually disciplining overcapacity. The consequences of not acting, though, are becoming harder to ignore with a solar industry that dominates market share globally but destroys value domestically.

Looking external. The external dimension is just as important. Premier Li Qiang’s work report pairs higher-level opening with digital trade, green trade, cross-border e-commerce, overseas warehouses, stronger international logistics, and a larger role for intermediate-goods trade. The language suggests a more selective and strategic openness, intending to attract capital, technology, and industrial participation on terms that fit China’s broader development agenda.

Energy: Security first, then green.

Security first. China is driven by energy security first, and global industrial leadership second, not decarbonization (the New Joule Order applied). China aims to reduce dependence on foreign energy and position itself as the dominant power in the next energy era. The green economy is now a big pillar of the Chinese economy, but it's also soft power.

Building a new energy system. China's next climate-industrial wave has shifted from generation to system-level. Long-duration storage, smart grids, flexible loads that connect electricity, data, and industrial operations are high on the priority list. The plan's emphasis on building a "new-type electricity system" (新型电力系统) and "new-type energy system" (新型能源体系) signals long-term, entire system-level planning that reaches into new sectors: industrial decarbonization, green fuels, grid flexibility, to drive both security and growth.

Grid signals. This is the biggest investment signal: State Grid, which serves 80% of China (Southern Grid covers the other 20%), is the world's largest utility in terms of coverage area and one of the top five companies by revenue in the world. On January 15th, it announced plans for ¥4 trillion over the 15th Five-Year Plan period ($25.1bn), up 40% compared to the 14th Five-Year Plan.

Green fuels as a security hedge. As the Iran conflict squeezes energy markets, China is leaning into treating green fuels as instruments of energy security, echoing the framing now heard in Europe or North America. Green hydrogen is listed in the “new quality productive forces” category and a “central strategic priority. Green fuels are also a “new growth point.” Beyond sustaining supply-side support, the coming years will see regulators launch a major policy push to address lackluster demand, primarily by pressuring key industries to ramp up green fuels consumption.

Sector support towards site-specific deployment. Zero-carbon parks and zero-carbon factories, alongside support for a low-carbon transition fund, green and low-carbon equipment, hydrogen power, and green fuels. The 15th FYP aims to establish ~100 zero-carbon parks and create 10,000 kilometers of zero-carbon transportation corridors. There’s also zero-carbon factories, low-carbon equipment, all supported by the transition fund. This matters because deployment environments often shape outcomes more powerfully than individual subsidies. Industrial parks and factory clusters allow policymakers to combine renewables, storage, power management, industrial software, carbon accounting, and logistics in one place.

Climate: Underpromise and underwhelming, but potential to overdeliver

Less ambitious on decarb goals. Officials set a 17% carbon intensity reduction target, weaker than the 14th FYP's 18% which China had fallen short of during the 2020-2025 period (due to loosening emissions restrictions post-COVID). Partway through that plan period, authorities had quietly revised their calculation methodology, arriving at a reported 17.7% reduction that masked how far short China had actually fallen.

Interestingly, analysis from CREA suggests China’s CO2 emissions may have already peaked – they’ve been flat or falling for 21 months, and the NRDC has quietly acknowledged that this trajectory should continue.

From energy control to carbon control. The most consequential language shift is the move from controlling energy consumption and intensity (能耗双控) to controlling carbon emission intensity and total carbon amount (碳排放双控). A dual-control framework for the 15th FYP centers on emissions intensity with overall emissions caps, alongside stronger carbon accounting. By 2035, China will reduce economy-wide net greenhouse gas emissions by 7-10% from peak levels and establish a “climate-adaptive society”. The Government Work Report's verb changed from "accelerate constructing" the system (2025) to "implement" it (2026) which means they will embed climate policy more deeply into industrial planning, investment decisions, and local government performance metrics.

New climate funding beyond subsidies. The plan introduces a National Low-Carbon Transition Fund, structured with central fiscal guidance and social capital as the main body, operating under a government-led, market-operated model. It’s a shift away from previous policies doling out direct fiscal subsidies. The same model is playing out in semiconductors, where a new national funding infusion has the government fund acting as an LP into specialized GPs.

Industry: Modernization and innovation above all else

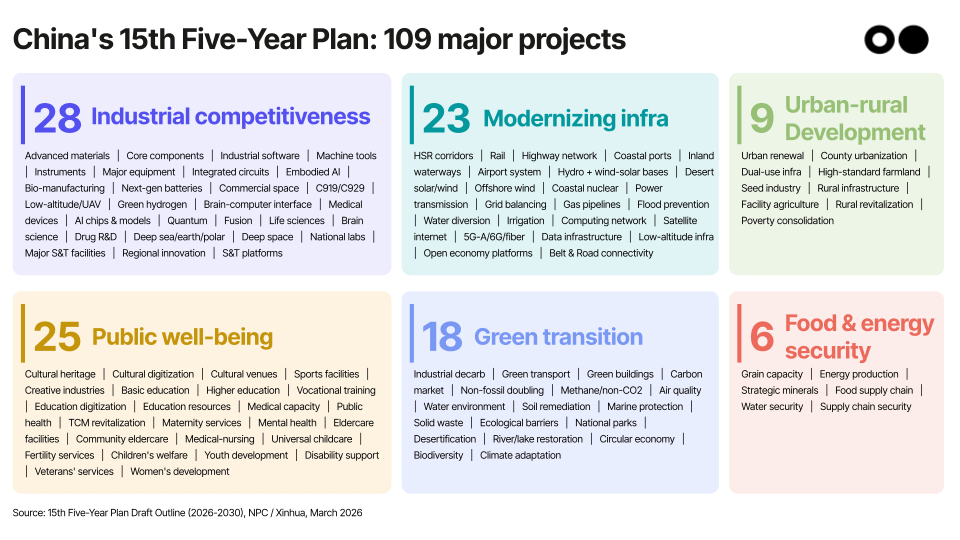

Industrial modernization comes first. The 15th FYP lists building a "modern industrial system" as the first key objective. The plan's 109 major engineering projects place green hydrogen, new-type batteries, and controlled nuclear fusion alongside semiconductors, embodied AI, and commercial spaceflight. Clean energy technology is a core component for industrial strategy and occupies the same spot as chips and AI.

This means both fostering emerging and future industries – aerospace, biomanufacturing, hydrogen, new materials, quantum computing – as well as upgrading traditional industries like mining, chemicals, and machinery. Officials are to accelerate the application of digital, smart, and green technologies in all areas to drive innovation and productivity.

Boosting scientific and technological self-reliance. US export controls and investment barriers have institutionalized China's push into AI, quantum, advanced manufacturing, and what Beijing calls "new-quality productive forces." In many areas, China has shifted from quantity to quality, moved up to mid- and high-end technologies, and wants to win these new scientific and technological races, from AI to fusion to 5G telecommunications to biomedicine.

New directions in 109 major engineering projects, across industrial manufacturing, energy and transport infra, urban-rural development, public well-being, green transition, and food & energy security. The projects range include everything from turning deserts into power plants, to building new offshore wind and coastal nuclear, new power transmission corridors, and inter-regional power exchange.

AI and robotics are the industrial policy enablers. The five-year blueprint promised to build out hyper-scale computing clusters to support AI-open source communities. Robotics and embodied intelligence were also one of China's eight designated strategic industries (a major step up from the 14th FYP), and it’s woven across multiple chapters on manufacturing, digital transformation, and healthcare, signaling its role as a key enabler of the industrial policy across the plan.

Conclusions

China’s path will not be smooth. There will be overcapacity in some segments, uneven provincial execution, and continued dependence on fossil fuels as a stabilizing layer in the energy system. Those tensions are real. Still, they should not obscure the larger point. The center of gravity is shifting toward system design. From the perspective of global climate policymakers, the 15th Five-Year Plan merits attention for reasons that extend far beyond climate issues. It offers a window into how Beijing wants to shape the operating environment for the next stage of growth. It may be underpromising on climate, but looking at lower-level policy and market trends, however, we think it’s poised to overdeliver.

We do not need to romanticize China’s model, but we do need to read it accurately. The most important signal from this FYP is Beijing is trying to make low-carbon capability part of its next industrial base, while embedding that capability inside a broader strategy for technology, security, and trade. For investors, entrepreneurs, and policymakers, that is the signal worth watching.

Special shout-out to our China monthly working group crew, including Sharon Chen, Roger Zhang, Johnny Huang, Pengxin Dong, Brian Yang, and Alex Li.

Keep an eye out for Part 3 on Tariffs and Global Trade, coming next month. And if you're not a subscriber yet, get more insights like this in your inbox every week: