U.S. President Donald Trump signed new agreements on rare earth and critical minerals with Japan and some Southeast Asian countries. The deals were finalized during his October 2025 Asia tour. They aim to lower reliance on China, which leads to global production of these key materials.

Rare earth elements are vital for many things, including electric vehicles (EVs), wind turbines, smartphones, and defense systems.

Global demand is rising fast as countries invest more in clean energy and digital technologies. These new partnerships are among the biggest efforts yet to build alternative supply chains for critical minerals.

Japan Deal: Strengthening Industrial and Energy Security

On October 28, 2025, Trump and Japanese Prime Minister Sanae Takaichi signed a key deal. This agreement aims to secure supplies of rare earths, lithium, cobalt, and nickel. The agreement expands past U.S.–Japan cooperation and includes new plans for joint investments, technology sharing, and transparent supply management.

Under the deal, both countries plan to:

- Build processing and refining plants for rare earths and battery minerals.

- Create strategic stockpiles and improve recycling systems.

- Support magnet production for EVs and defense industries.

- Explore nuclear fuel supply cooperation for next-generation reactors.

Japan still relies on China for about 65% of its rare earth imports, even after years of trying to diversify. The new deal aims to cut this dependence by sourcing from U.S. allies like Australia and Vietnam. Also, it will process materials locally or in partner nations.

The plan supports Japan’s economic security law, which pushes companies to find new material sources. Tokyo has set aside about ¥400 billion (US$2.7 billion) in funding to help domestic rare earth and battery material projects through 2027.

Southeast Asia: Expanding the Network Beyond China

Trump also announced new cooperation deals with Malaysia, Vietnam, Thailand, Cambodia, and Indonesia. These countries hold key mineral reserves and play important roles in regional trade.

Malaysia already operates one of the world’s few large rare-earth processing plants outside China. Vietnam has about 22 million tonnes of rare-earth reserves, second only to China. Indonesia and Thailand are major producers of nickel and tin, vital for EV batteries.

The Southeast Asia deals aim to:

- Bring in U.S. and Japanese investments for mining and refining projects.

- Train local workers and improve technical skills.

- Cut tariffs and export barriers that slow regional trade.

- Support cleaner and safer mining technologies under ESG standards.

Experts say these efforts could create an “Indo-Pacific mineral corridor.” This would link mines in Australia, processors in Southeast Asia, and manufacturers in Japan. This network would help reduce China’s control over the middle stages of the supply chain.

Why Rare Earths Matter: A Market Under Strain

Rare earths are a group of 17 metals used in many high-tech and clean energy products. The most valuable are neodymium, praseodymium, and dysprosium. These elements are essential for strong magnets used in EV motors, drones, and wind turbines.

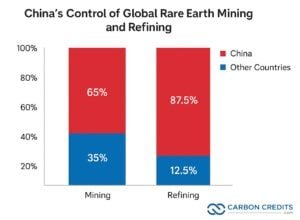

China controls around 60–70% of mining and 85–90% of refining for rare earths. This gives Beijing major influence over countries that depend on these materials.

In 2024, the world produced about 350,000 tonnes of rare earth materials. The International Energy Agency (IEA) expects demand to reach over 500,000 tonnes by 2030. Market value could rise from $13 billion in 2024 to over $25 billion by 2030.

The U.S. currently makes about 12% of global rare earth ore, mostly from the Mountain Pass mine in California. However, much of it is still sent to China for processing. That dependence makes the new deals with Japan and Southeast Asia even more important.

Strategic and Economic Significance

For the United States, these deals mark a new stage in mineral diplomacy. Washington aims to safeguard clean energy and defense industries. It plans to do this by securing long-term supply agreements in Asia to help protect against disruptions.

Japan gains stronger support for its automotive, electronics, and robotics sectors. The country is restarting its rare earth recycling programs. These programs slowed down after Chinese export limits in 2010 made prices rise sharply.

For Southeast Asian nations, the agreements promise foreign investment, new jobs, and technology sharing. Malaysia and Vietnam might become key centers for refining and magnet production. This could create jobs for thousands of skilled workers.

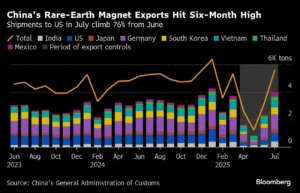

The deals also back U.S. efforts to counter China’s export restrictions. In 2024, China limited exports of gallium, germanium, and certain rare earth magnets for “national security” reasons. Those actions disrupted supply chains and forced manufacturers in Japan, Europe, and the U.S. to look elsewhere for materials.

Rare Earth Market Outlook: Rising Demand, Tight Supply

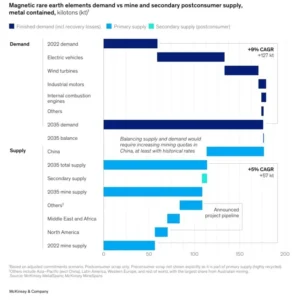

Demand for rare earth magnets, especially neodymium-iron-boron (NdFeB) magnets, might triple by 2035. This rise is fueled by electric vehicles (EVs) and wind turbines. Each electric vehicle needs 1–2 kilograms of these magnets, while one offshore wind turbine can use up to 600 kilograms.

The price of neodymium oxide has climbed from about US$70 per kg in 2020 to more than US$120 per kg in 2025, showing strong pressure on supply. China’s quota limits and environmental checks have made availability uncertain.

The U.S., Japan, and the European Union are expanding recycling programs. They aim to recover rare earths from old motors and electronics. This helps reduce reliance on mined materials. Yet, recycling currently provides less than 5% of total global demand.

The Cost of Breaking Free from China

Building alternative supply chains is difficult. Several challenges include:

- High costs: Rare-earth plants are expensive and take years to build.

- Environmental risks: Poor waste management can pollute water and soil.

- Financing issues: Price swings make investors cautious.

- Geopolitical tensions: China may respond by lowering prices or tightening exports.

Experts say that without strong government support, new producers may not compete with China’s scale and low costs. Both the U.S. and Japan are studying tax credits and loan programs to help new projects move forward.

Forging a New Indo-Pacific Supply Chain

These rare earth agreements send a clear message: the U.S. and its allies want to reshape global supply chains around trusted partners. The next steps include choosing priority projects, securing funding, and coordinating trade rules.

If successful, these efforts could shift 15–20% of global refining capacity away from China by the early 2030s. That would mark the biggest industry shift in decades.

For the U.S., Japan, and Southeast Asia, the deals combine economic security, industrial growth, and clean energy goals. They also show how the energy transition and geopolitics are now closely linked.

In the long run, building diverse and stable rare earth supply chains could make clean energy industries stronger and less dependent on any single country.

- FURTHER READING: MP Materials (MP Stock): The Rare Earth Magnet Powering America’s Clean Energy and Climate Goals

The post Trump Inks Rare Earth Deals with Japan and Southeast Asia to Secure Supply Chains appeared first on Carbon Credits.