See more visualizations like this on the Voronoi app.

See more visualizations like this on the Voronoi app.

Where Venture Capital Money Is Going: AI vs. Everything Else

See visuals like this from many other data creators on our Voronoi app. Download it for free on iOS or Android and discover incredible data-driven charts from a variety of trusted sources.

Key Takeaways

- AI and machine learning have helped prop up venture capital as funding for other sectors cooled.

- AI accounted for 52% of global VC deal value in Q4 2025.

- Investment accelerated sharply in 2024 as large funding rounds flowed into AI infrastructure and model developers.

Venture capital activity has slowed since its pandemic-era peak, but artificial intelligence remains a major exception.

Investment flowing into AI and machine learning (ML) has surged over the past two years, helping sustain overall venture funding even as deal activity in other sectors weakened.

This graphic visualizes data compiled by BestBrokers, using information from PitchBook, CB Insights, and LIQUiDITY, showing how venture capital has increasingly concentrated around AI.

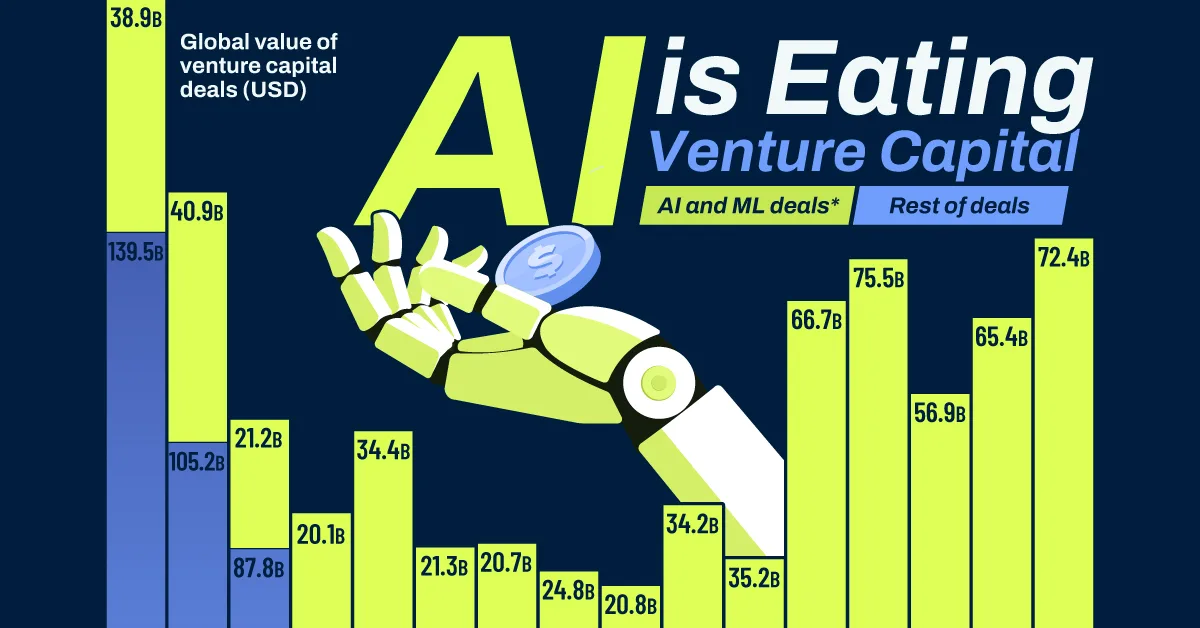

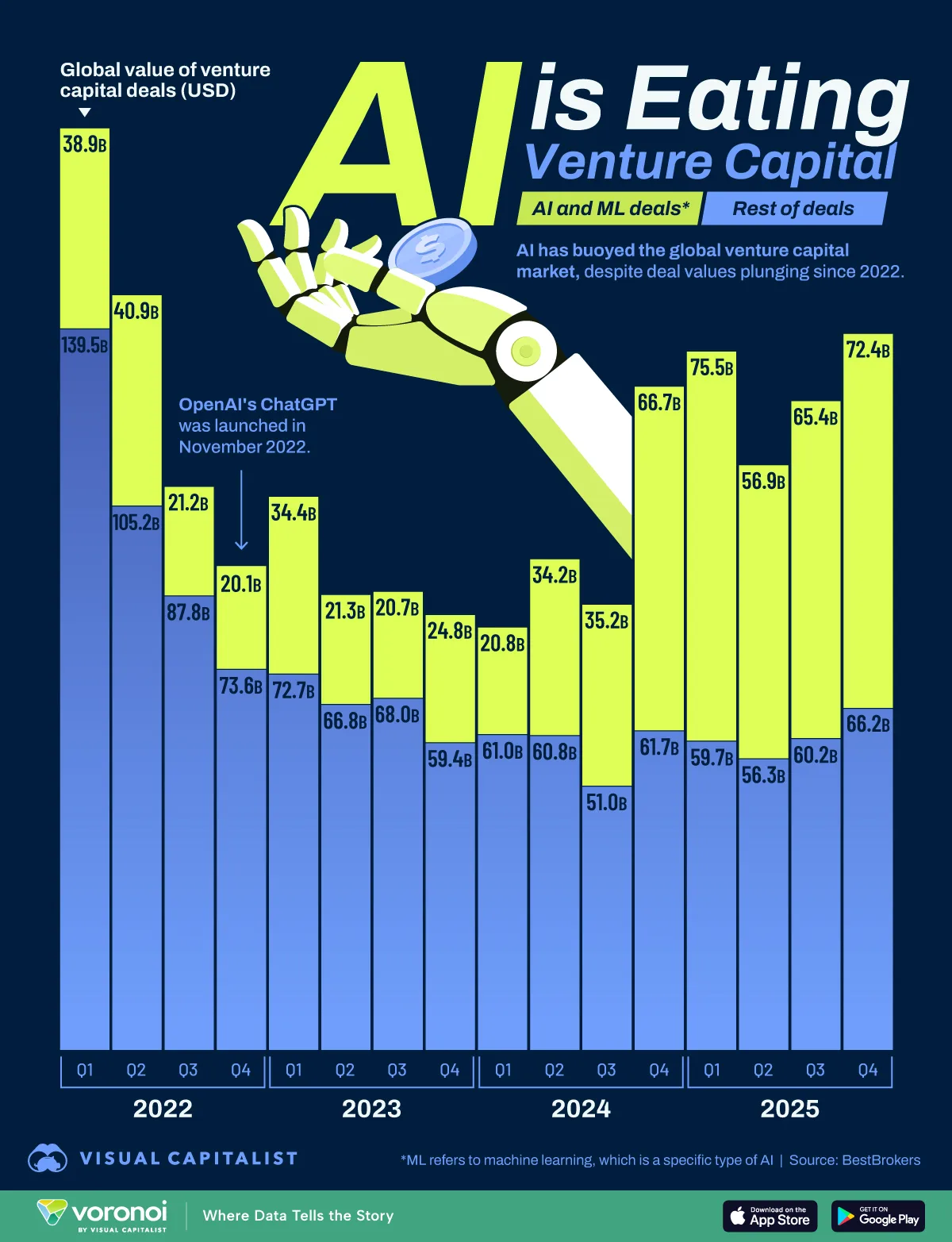

AI Takes a Larger Slice of the Pie

The quarterly data from 2022 to 2025 shows how the balance between AI and non-AI venture investment has shifted.

| Quarter | AI and ML deals ($B) | Rest of Deals ($B) | % Share (AI) |

|---|---|---|---|

| Q1 2022 | 38.9 | 139.5 | 21.8% |

| Q2 2022 | 40.9 | 105.2 | 28.0% |

| Q3 2022 | 21.2 | 87.8 | 19.4% |

| Q4 2022 | 20.1 | 73.6 | 21.5% |

| Q1 2023 | 34.4 | 72.7 | 32.1% |

| Q2 2023 | 21.3 | 66.8 | 24.2% |

| Q3 2023 | 20.7 | 68.0 | 23.3% |

| Q4 2023 | 24.8 | 59.4 | 29.5% |

| Q1 2024 | 20.8 | 61.0 | 25.4% |

| Q2 2024 | 34.2 | 60.8 | 36.0% |

| Q3 2024 | 35.2 | 51.0 | 40.8% |

| Q4 2024 | 66.7 | 61.7 | 51.9% |

| Q1 2025 | 75.5 | 59.7 | 55.8% |

| Q2 2025 | 56.9 | 56.3 | 50.3% |

| Q3 2025 | 65.4 | 60.2 | 52.1% |

| Q4 2025 | 72.4 | 66.2 | 52.2% |

Venture capital boomed in 2021, but sentiment shifted in 2022 amid geopolitical uncertainty, rising interest rates, and a slowing exit market. Deal value dropped 47% between the first and fourth quarters of 2022, and AI represented only a small share of overall funding at the time.

OpenAI’s ChatGPT launched in November 2022, sparking a wave of interest in generative AI. Funding for AI and ML rose in early 2023 even as other venture deals stagnated.

The real step-change arrived in 2024. AI dealmaking accelerated throughout the year and surged in the fourth quarter, when the sector attracted $66.7 billion in funding—surpassing the $61.7 billion invested across all other sectors combined.

This growth reflects both rising investor optimism and the capital-intensive nature of AI infrastructure, including chips, data centers, and large-scale model development.

By Q4 2025, venture deals totaled $138.6 billion globally, with AI and ML accounting for 52% of the total—the first time the sector made up more than half of deal value in the dataset.

Fears of a Bubble

The surge in AI investment has split investors across public and private markets, with some warning the industry may be in a bubble while others remain highly optimistic about its long-term potential.

Concerns have also been raised about opaque private funding and circular dealmaking among major AI players. Strong earnings from companies such as Nvidia, however, have helped sustain investor enthusiasm.

How disruptive AI ultimately proves to be remains uncertain, and venture capital flows will likely continue shifting as investors respond to technological breakthroughs and broader global events.

Learn More on the Voronoi App

To learn more about how the AI industry is creating a large cap boom, check out this graphic.