Happy Monday!

China has released a draft of its policy priorities and allotments for the next five years, and it’s juicy. We’ve got a breakdown below.

In deals, $3bn for renewable energy development, $500m for co-packaged optics (CPO) solutions, and $240m for nuclear fusion development.

In other news, Iran and energy markets, Terrapower’s next-gen nuclear milestones, and deep sea mining approvals.

Thanks for reading!

📩 Submit deals and announcements for the newsletter at hello@ctvc.co.

💼 Find or share roles on our job board here.

CTVC is powered by Sightline Climate, the tactical market intelligence platform for energy and investment decision-makers.

China's 15th FYP: From the world's factory to advanced manufacturing

With so much going on in the world right now, last Thursday, China released the draft outline of its 15th Five-Year Plan (2026-2030), its central economic planning framework. The 15th FYP isn’t just an important-sounding document, it’s the CCP’s top-down blueprint for mobilizing capital, talent, and policy over the next half-decade.

Read on for the topline breakdown of the 15th FYP. We’ll also have a deep dive this Friday on how Chinese industrial policy funnels across all levels of the public and private sectors as part of our ongoing China coverage.

What’s in this plan

💰 Fiscal: GDP growth target dropped to 4.5-5% range (the first time it’s been below 5% since 1991); budget deficit maintained at historic high of 4% of GDP, broad deficit ~9.5%

📈 Priorities: "Modern industrial system” is first – differing from previous FYPs that led with “tech innovation”; R&D spending at $61.8bn, up 10% YoY

🏭 Industries: Goal to upgrade traditional industries (metals, machinery, textiles, chemicals) via automation, digitalization, and green tech, while expanding advanced industries (aerospace, new materials, drones); Future industries include quantum computing, humanoid robots, 6G, brain-machine interfaces, nuclear fusion, biomanufacturing, embodied intelligence

🤖 Artificial intelligence: Sweeping "AI+ action plan" to embed AI across manufacturing, healthcare, logistics, robotics; $70bn for semiconductor incentives and $137bn for AI supply chain

💨 Emissions: Shift from controlling “energy consumption” to controlling “carbon emissions” directly; 17% carbon intensity reduction target, slightly weaker than 14th FYP's 18%

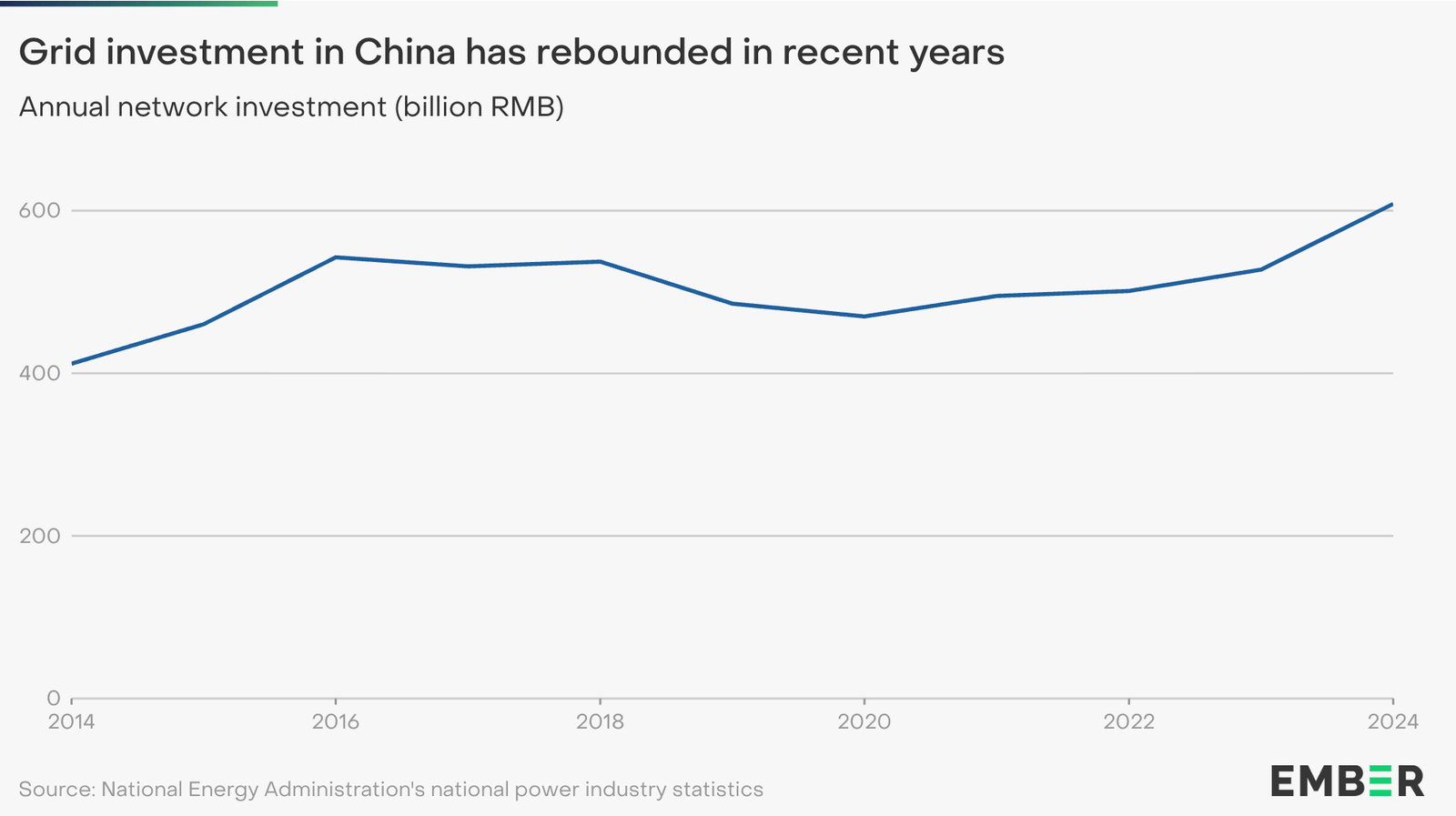

⚡ Energy mix: Aim to double non-fossil energy in 10 years; $5tn combined grid investment; Coal language walked back from "gradually reduce" to "promote peaking"; ~100 zero-carbon industrial parks, 10,000km zero-carbon transport corridors; $116bn in policy financial instruments with green/low-carbon as a priority area

🔒 Security: Extreme contingency planning; Food self-sufficiency and stable energy production framed as "extreme-scenario preparedness;” Defense budget up 7% to $275bn

Why it matters

The world cannot decarbonize without China. It is simultaneously the largest emitter and the largest builder of clean energy, installing more solar, wind, and batteries each year than the rest of the world combined and manufacturing many of the key parts behind these technologies.

But the 15th Five-Year Plan comes at a critical juncture: China is facing an economic slump amid heightening geopolitical fragmentation. Its traditional growth engines (real estate and infra) are slowing while manufacturing margins are getting squeezed by years of overcapacity (involution) and trade barriers, as we wrote in China’s electrostate readiness breakdown.

So now, China appears to be taking its foot off the gas on near-term economic stimulus (i.e. setting its lowest GDP growth target in 35 years). Instead, this FYP emphasizes science and technology, focusing on innovation, which faces no cuts. Beijing is betting on the next frontier of industries such as energy tech, AI, semiconductors, and aerospace to drive growth, aiming to be both self-sufficient and lead on the global stage, rather than relying primarily on traditional carrot/stick policy levers like boosting domestic consumption or loosening monetary policy.

Key takeaways

- Carbon accounting shift. China is shifting from controlling energy consumption to directly managing carbon emissions. It seems like a setback, but a dual-control framework for the 15th FYP centers on emissions intensity and has overall emissions caps, alongside stronger carbon accounting, product carbon-footprint management, and carbon-label certification. This embeds climate policy more deeply into industrial planning, investment decisions, and local government performance metrics.

- But the grid is the big bet. State Grid plans $574bn in investment during the 15th FYP, up 40% from the last cycle. Add China Southern Power Grid's expected $145bn, and combined grid capex nearly doubles the 13th FYP. It makes sense: in 2025, China installed 315GW of solar and 119GW of wind in 2025 alone; energy storage capacity growth (75GW) exceeded peak electricity demand growth (55GW) for the first time. Post-2028, grid investment tilts toward smart infrastructure: software, controls, sensors, distribution, and microgrids.

- It’s not 2020 anymore. China’s next climate-industrial wave should not be read through a 2020 lens. It’s not just about scaling solar, batteries, and EVs, the more interesting layer is integration: storage, smart grids, flexible loads, industrial energy systems, carbon-management software, power electronics, and advanced manufacturing for the tools that connect electricity, data, and industrial operations more effectively. (Plus the planned industrial parks that are deployment testbeds for it.) This slots in nicely with the state’s focus on “AI+.”

- Energy security first, and green fuels count. This FYP reflects a consistent Chinese policy instinct: decarbonize while preserving system reliability, industrial continuity, and geopolitical flexibility. Western observers may debate the balance, yet it is clearly part of how Beijing is sequencing the transition. And as the Iran war squeezes energy markets, China is leaning into treating green fuels as instruments of energy security, industrial upgrading, and renewable integration. That’s even broader framing than the one often heard in Europe or North America.

Watch your inboxes Friday, for an even deeper dive as part of our China series. We’ll unpack how China’s industrial policy machine works and what it means for climate capital.

Deals of the Week (3/2-3/9)

VC / Growth

⚡ SHINE Technologies, a Janesville, WI-based nuclear fusion developer, raised $240m in Growth funding from NantWorks, Deerfield Management, Fidelity Management & Research Company, Oaktree Capital Management, Pelican Energy Partners, and other investors.

🏗 Gropyus, a Vienna, Austria-based sustainable homes developer, raised $116m in Series C funding from Vonovia, Semapa Next, FAM AB, and State of Michigan Retirement System.

🚗 Oxa, an Oxford, England-based autonomous driving software and services provider, raised $103m in Series D funding from National Wealth Fund (UKIB), Hostplus, IP Group, NVentures, and bp Ventures.

🏠 Renewable Iron Fuel Technology (RIFT), an Eindhoven, Netherlands-based iron fuel heat generation developer, raised $96m in Series B funding from PGGM, Brabantse Ontwikkelings Maatschappij (BOM), Energie transitie fonds Rotterdam, Invest-NL, OostNL, and other investors.

🥩 Verley Food, a Lyon, France-based precision fermentation dairy protein developer, raised $38m in Series A funding from Alven, Blast Club, Bpifrance, CapTech, Founders Future, and other investors.

🔋 UniverCell, a Kiel, Germany-based custom battery cell manufacturer, raised $35m in Series B funding from DeepTech & Climate Fonds (DCTF), IKA, WIKA Group, and European Innovation Council (EIC).

⚡ Micopower, an Anseong, South Korea-based solid oxide fuel cell (SOFC) hydrogen specialist, raised $27m in Seed funding from Meritz Securities and AFW Partners.

⚡ Zeno, a Nanyuki, Kenya-based battery-as-a-service platform for two-wheeled vehicles, raised $20m in Series A funding from Congruent Ventures, Active Impact Investments, and Lowercarbon Capital.

⚡ Reykjavik Geothermal, a Reykjavík, Iceland-based geothermal power producer, raised $20m in Series B funding from Summa.

🧪 PlasmaLeap Technologies, a Sydney, Australia-based zero-emissions chemical reactor developer, raised $20m in Series A funding from Bill & Melinda Gates Foundation, Investible, Yara Growth Ventures, Agnition Ventures, Artesian Capital Management, GrainCorp Ventures, and other investors.

⚡ Photoncycle, an Oslo, Norway-based residential renewable energy systems provider, raised $17m in Series A funding from NordicNinja, Voima Ventures, Eviny Ventures, Lifeline Ventures, Luminar Ventures, and Momentum.

🧪 Shellworks, a London, England-based sustainable plastic alternatives developer, raised $15m in Series A funding from Alter Equity, Founder Collective, JamJar Investments, LocalGlobe, Nat Friedman (NFDG), and other investors.

⚡ BeyondMath, a London, England-based AI-driven physics simulation developer, raised $10m in Seed funding from Cambridge Innovation Capital, InMotion Ventures, Insight Partners, and UP.Partners.

🥩 Mezcla, a New York City, NY-based plant-based protein snack bar manufacturer, raised $10m in Series B funding from Bluestein Ventures, Grupo DMI, Habitat Partners, Lever VC, Redwood Consumer – Santatera, Steve Platt, and Tonic Ventures.

🏗 baCta, a Paris, France-based biosynthetic rubber producer, raised $8m in Seed funding from Daphni, LocalGlobe, and OVNI Capital.

Project Finance / Debt

⚡ Atlas Renewable Energy, a Miami, FL-based renewable energy developer, raised $3bn in Debt funding from Global Infrastructure Partners, BNP Paribas, Crédit Agricole CIB, Goldman Sachs, MUFG Bank, Morgan Stanley, Natixis Corporate & Investment Banking, and Santander.

🔬 Ayar Labs, a San Jose, CA-based co-packaged optics (CPO) solutions developer for AI scale-up, raised $500m in Growth funding from Neuberger Berman, 1789 Capital, Advent Global Opportunities, Alchip Technologies, AMD Ventures, and other investors.

⚡ Avantus, a San Diego, CA-based renewable energy developer, raised $150m in PF Debt funding from Banco Bilbao Vizcaya Argentaria and Canadian Imperial Bank of Commerce (CIBC).

🧪 EverWind Fuels, a Halifax, Canada-based green hydrogen and ammonia producer, raised $88m in PF Debt funding from Nuveen.

⚡ Commercial Energy South Africa (CESA), a Centurion, South Africa-based sustainable energy solutions provider, raised $39m in Debt funding from Greenpoint Capital and Vantage Capital.

🔋 Zeno, a Nanyuki, Kenya-based battery-swap electric motorbike manufacturer, raised $5m in Debt funding from Camber Road and Trifecta Capital.

Exits

☀️ OMCO Solar, a Phoenix, AZ-based solar mounting structure manufacturer, was acquired by MacLean-Fogg Holdings.

🌊 Lunsemfwa Hydro Power Company (LHPC), a Kabwe, Zambia-based hydropower plant operator, was acquired by Globeleq.

⚡ Geothermie Rupertiwinkel, a Munich, Germany-based renewable energy generator and storage operator, was acquired by ZeroGeo Energy.

💨 Carbon Alpha, a Calgary, Canada-based carbon capture project developer, was acquired by Svante.

Funds

Seraphim Space, a London, UK-based spacetech-focused venture capital firm, raised $100m for Seraphim Space Ventures II from British Business Bank, Eutelsat, NEC, SKY Perfect JSAT, and Arabsat, focusing on Seed and Series A investments in space infrastructure, satellite data applications, and in-orbit computing.

This is a sample of deals available for Sightline clients. Can’t get enough deals?

In the News

Oil and broader energy markets jolted as the widening US-Israel war with Iran disrupted traffic through the Strait of Hormuz, hit Gulf production, and briefly sent Brent crude near $120 a barrel before it pulled back. Beyond the humanitarian implications, market fears rose. Damage to Gulf infrastructure and curbed output could turn a geopolitical shock into a sustained supply crunch, with traders and policymakers warning of renewed inflation and weaker growth. Oil-price spikes strengthen the case for electrification, efficiency, storage, and non-Hormuz supply chains, but they also risk raising financing costs and near-term energy bills.

The head of the International Seabed Authority signaled support for allowing deep-sea mining under a new rulebook with strict environmental limits, a major shift in a long-running debate over whether the industry should proceed at all. This is a strong signal that commercial seabed extraction is moving closer to reality.

The US Nuclear Regulatory Commission approved TerraPower’s construction permit for its Natrium reactor in Kemmerer, Wyoming. The project marks the first commercial-scale Generation IV reactor in the US to receive a construction license, a milestone for next-generation nuclear deployment.

Germany’s installed offshore wind capacity has surpassed 10GW, after new turbines came online in the North Sea. That’s a key milestone in the country’s energy transition, as Berlin pushes toward even larger capacity targets later this decade.

In hydrogen news, Moeve reached FID on a 300MW green hydrogen plant at its La Rábida refinery in Spain, the first phase of its planned 2GW Andalusian Hydrogen Valley. Meanwhile, HydrogenPro completed installation of all 40 electrolyzers for the 220MW ACES Delta hydrogen project in Utah, one of the largest green hydrogen production systems globally, which will convert excess renewable power into hydrogen and store it in underground salt caverns. It can provide long-duration, seasonal energy storage to balance the grid.

A consortium led by BlackRock’s Global Infrastructure Partners and EQT agreed to acquire US power company AES in a deal valuing the utility at about $33bn including debt, taking the company private. The move reflects rising investor interest in electricity infrastructure as power demand surges from AI data centers and electrification.

Pop-up

Geothermal gets major boost from the DOE

Racing against the tax credit clock, battery storage just hit a new record.

The money behind the energy transition gets its annual checkup.

AI infrastructure could be slightly more grid-friendly than feared.

Happy International Women’s Day!

Opportunities & Events

📅 Navigating Down Rounds: Join Enduring Planet and Friends on Zoom from 10:00-11:30 AM PT for a panel on startup valuation and how founders can manage the current trend of down valuation rounds. What can startups do to run a down round deliberately, protect the company, and position themselves to move forward? Learn this and much more at the panel.

💡Startups to Watch: Early-stage climate tech founders can now apply for Startups to Watch a pitch competition run by The Trellis Group focusing on climate adaptation, material innovation, and data center solutions. The competition will culminate in live finals at Trellis Impact 26 this June in San Francisco. Apply by March 27.

Jobs

Investment Associate, @Energy Impact Partners

XIG Imprint Business Development Lead – Vice President @Goldman Sachs

Junior Account Executive, @3V Infrastructure

Summer Research Intern, Senior Associate – Clean Fuels, Principal Analyst – Data Centers and Power Markets, Data Analyst – Late-Stage Finance, @Sightline Climate

Associate, @Prelude Ventures

📩 Feel free to send us deals, announcements, or anything else at hello@ctvc.co. Have a great week ahead!