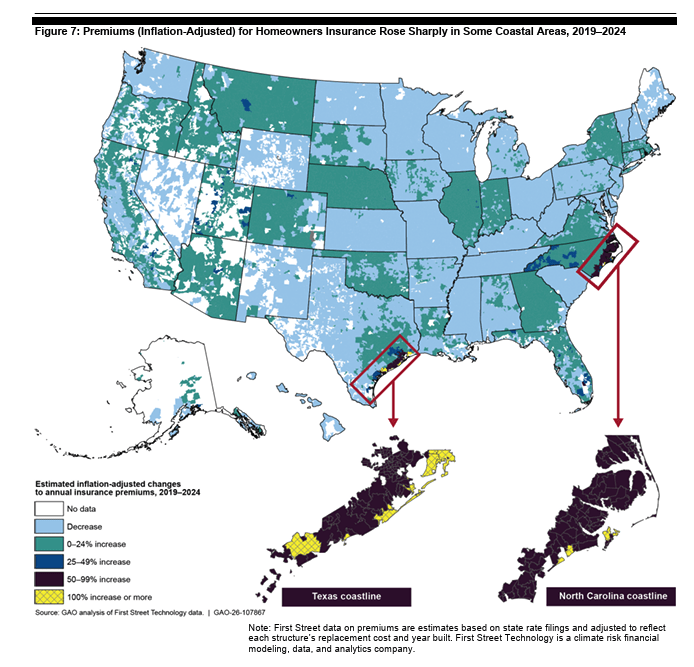

In parts of coastal North Carolina and Texas, homeowners who were paying one rate for property insurance in 2019 are now paying double, and that’s after adjusting for inflation.

A February 2026 report from the U.S. Government Accountability Office, the most thorough federal analysis of homeowners insurance markets in years, confirms what many Americans in hurricane, wildfire, and tornado-prone areas already know: the cost and availability of home insurance now depends on climate risk. Nationally, premiums only slightly outpaced inflation from 2019 to 2024. But in high-risk areas, homeowners are seeing price jumps that are changing where people can afford to live, own property, and even stay insured.

The National Average Hides the Real Story

At first glance, the national data seems manageable. The GAO found that the average U.S. homeowners’ insurance premium, adjusted for inflation, rose only 3 percent between 2019 and 2024, going from $2,743 to $2,829 in 2024 dollars. The South reported higher premiums than other regions, but the national average stayed mostly steady.

But when you look at the data by ZIP Code, the story changes. In the same period, many coastal areas in North Carolina and Texas saw premium increases of more than 50 percent after adjusting for inflation. Some places in Palm Beach County, South Florida, also had big jumps. At least 10 ZIP Codes in North Carolina, Texas, Utah, Florida, and California saw increases over 25 percent above inflation in just the last five years.

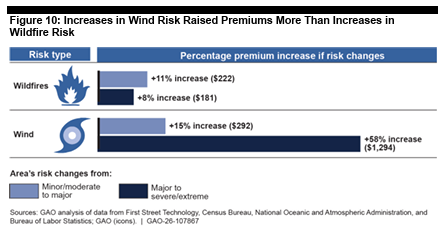

Wind Costs Far More Than Wildfire — For Now

The GAO used statistical modeling to show how disaster risks raise premiums, and the results are clear. Homes in areas with severe or extreme wind risk pay about 58 percent more, or $1,294 extra per year, compared to similar homes with only major wind risk. Moving from major to severe wildfire risk adds about 8 percent, or $181 per year, to premiums.

This difference shows how much damage wind events like hurricanes can cause. According to GAO data, ZIP Codes with severe or extreme wind or wildfire risk saw premiums rise 6 to 10 percent each year since 2021. In comparison, areas with major risk saw increases of only 1 to 4 percent per year. Over six years, an 8 percent annual increase adds up to a total increase of 59 percent.

State-level disaster costs also play a role. The GAO found that when a state’s average disaster-related costs rose from $25 billion to $35 billion between 2018 and 2023, premiums went up by about 8 percent, or $170 more per year. This happens because insurers update their loss estimates after big disasters. One insurer told the GAO it raised its wildfire risk assumptions for California after the major fire seasons in 2017 and 2018, even before the devastating 2025 Los Angeles wildfires.

Affordability Is Worst Where Income Is Already Stretched

Premium burden, which is the cost of insurance compared to median household income, highlights how climate change is hitting low-income communities hardest. In 2023, Florida, Louisiana, and Oklahoma had the highest premiums relative to income, just as they did in 2019. According to the GAO, states where premiums take up more than 10.6 percent of median income are considered to have a “very high” burden. Florida falls into this category.

The people paying the most for insurance are often those who have the fewest options to move or insure themselves. High insurance costs in risky areas often go hand in hand with lower incomes, older homes, and less access to federal help. Researchers call this a climate-driven affordability crisis.

When Private Insurance Disappears

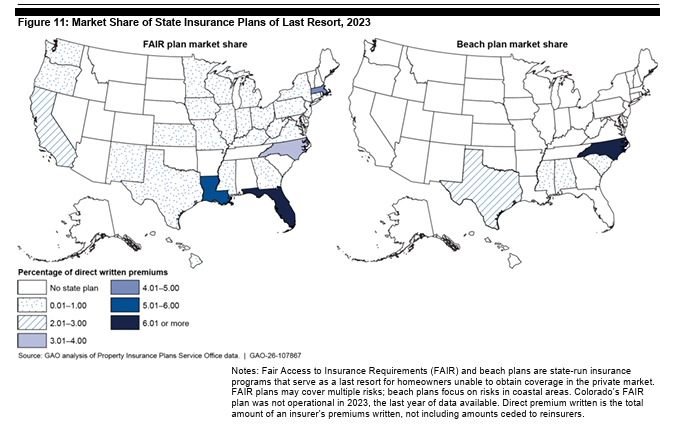

Rising premiums are just one issue. In some high-risk areas, private insurers are not only raising prices but also leaving the market. The GAO tracked the market share of state FAIR plans and beach plans, which are the “insurers of last resort” for homes that can’t get regular insurance, from 2019 to 2023. Nationally, their combined market share almost doubled, going from about 1.4 percent to 2.5 percent of homes.

California’s numbers tell the story. The state’s FAIR Plan, which covers wildfire risk, grew from about 200,000 residential policies in 2020 to around 450,000 by 2024. About 78 percent of this growth happened in ZIP Codes with major or severe wildfire risk. After the January 2025 Los Angeles fires, enrollment jumped another 43 percent between September 2024 and December 2025, according to Insurance Journal. Even low-risk urban properties are ending up on the FAIR plan as insurers withdraw from whole regions.

Florida and Louisiana have the highest FAIR plan market share among states with these programs. North Carolina’s beach plan, which covers coastal areas, leads all beach plans by market share. All three states face high Atlantic hurricane risk.

Regulation Is Part of the Problem Too

Insurance policies are regulated by each state, and the GAO found that how long it takes to approve premium increases affects policy availability. States where regulators take longer to approve these requests often have more homeowners who can’t get private insurance. The GAO found that every extra 60 days in approval time was linked to about a 0.5 percentage point increase in the state’s FAIR plan market share.

Colorado’s median approval time from 2020 to 2024 was 331 days, the longest in the country. California’s was 305 days. When insurers can’t adjust rates quickly enough to reflect actual risk, some of them exit the market rather than underwrite policies at a loss. This is the dynamic that partly drove the California insurance exodus before the state’s Sustainable Insurance Strategy reforms announced in 2023, which allowed catastrophe modeling and reinsurance costs to be factored into rate-setting, practices already standard in most other states.

Insurers Are Losing Money — Just Not How You Think

Insurers lost money on homeowners insurance underwriting in 22 out of 30 years from 1995 to 2024, with an average annual loss of 4.2 percent. The worst years matched up with major disasters like Hurricanes Fran (1996), Sandy (2012), Harvey, Irma, Maria (2017), and the Maui wildfires (2023).

However, insurers offset underwriting losses with investment income, so the situation isn’t as bad as it seems—they are still highly profitable. In 2024, homeowners insurance had a $1.8 billion underwriting loss, but $8.8 billion in investment income turned it into a $6.9 billion profit overall. The industry is still profitable, even as rates rise and coverage becomes harder to obtain. Insurers say risk-based pricing is needed for long-term stability, but critics believe profitable insurers could do more to keep coverage available in high-risk areas.

Allianz SE board member Günther Thallinger told Capital&Main.com that climate change is a “systemic risk that threatens the very foundation of the financial sector,” and added that “a house that cannot be insured cannot be mortgaged.” The insurance crisis is a credit crisis in slow motion.

What States and the Federal Government Can Do

The GAO asked state regulators, insurance industry groups, and consumer advocates about eight possible federal policy options. Most agreed that the best approach is to focus on mitigation programs that help homeowners make their properties more disaster-resistant.

The GAO recommends Alabama’s Strengthen Alabama Homes program as a model. Since 2011, it has given grants to about 10,000 homeowners to upgrade their roofs to FORTIFIED standards, and another 45,000 have upgraded without grants. Alabama requires insurers to give premium discounts for FORTIFIED homes, making the upgrades a good investment. A 2025 study found that FORTIFIED roofs had fewer and less severe losses after Hurricane Sally, even with higher wind speeds. The National Institute of Building Sciences found benefit-cost ratios from 1.5 to 28, depending on wind speed.

As of now, at least 18 states have introduced bills in 2026 to reform insurance programs and include mitigation measures. These efforts build on a 2025 Colorado law (HB25-1182) that requires insurers to be open about their risk models and to discount premiums for homeowners who take mitigation steps.

The GAO listed eight federal policy options that Congress could consider, and your opinion matters. These options include tax deductions or credits for mitigation upgrades and insurance premiums, federal funding for infrastructure, a federal reinsurance program, community-based disaster insurance, and changes to how insurers’ reserves are taxed.

You can contact your U.S. senators and representative to share your views on where federal money should go. Mitigation incentives have wide support and are the most practical short-term step. Direct federal insurance programs are more debated, but if you think the private market has failed in your area, make that clear. The House Financial Services Committee and Senate Banking Committee are the main places for these discussions. You can find your members at congress.gov.

What You Can Do Now

- Check your disaster risk. First Street Technology’s Risk Factor tool gives property-level wildfire, flood, and wind risk scores. This is the same data source the GAO used.

- Look into the FORTIFIED standards. The Insurance Institute for Business & Home Safety (IBHS) certifies FORTIFIED construction for roofs, homes, and commercial buildings. Some states offer grants or require insurers to give discounts for certified homes.

- Learn about your state’s FAIR plan. If you can’t find private coverage, your state might have a FAIR plan or beach plan as a last resort. These plans usually offer less coverage and cost more than private insurance, but they provide insurance when no other options exist.

- Review your current insurance coverage. Many homeowners don’t realize they are underinsured. Check your dwelling coverage limit and compare it to current replacement costs, which have gone up a lot since 2020 due to construction inflation.

- Get involved with your state legislature. Insurance reform is happening in many states right now. Colorado, Washington, Oregon, and Hawaii are working on bills that link insurance to mitigation in 2026. You can find your state insurance commissioner at naic.org.

- Support federal funding for mitigation. FEMA runs several pre-disaster mitigation grant programs. Community investments in things like firebreaks, levees, and better building codes help lower the basic risk that affects everyone’s insurance premiums.

The post How Climate Disasters Are Breaking the Homeowners Insurance Market appeared first on Earth911.

- Source: https://earth911.com/home-garden/how-climate-disasters-are-breaking-the-homeowners-insurance-market/