The global aviation industry is facing a new climate challenge. Airlines might soon face challenges in getting enough quality carbon credits to follow international emissions rules. This could lead to an extra $127 billion in costs over the next ten years.

An MSCI Carbon Markets analysis, as first reported by Financial Times, warns of a carbon credit shortage. This shortage under the Carbon Offsetting and Reduction Scheme for International Aviation (CORSIA) could drive prices near $100 per metric ton by 2035. That would be a big jump from current levels. It could raise compliance costs for airlines around the world.

Why CORSIA Is Reshaping Aviation’s Climate Strategy

The warning comes as international air travel continues to recover. The International Air Transport Association (IATA) predicts that global passenger numbers will surpass 5.2 billion in 2025. Airline revenues are also expected to exceed $1 trillion. More flights also mean more emissions, increasing demand for high-quality carbon credits.

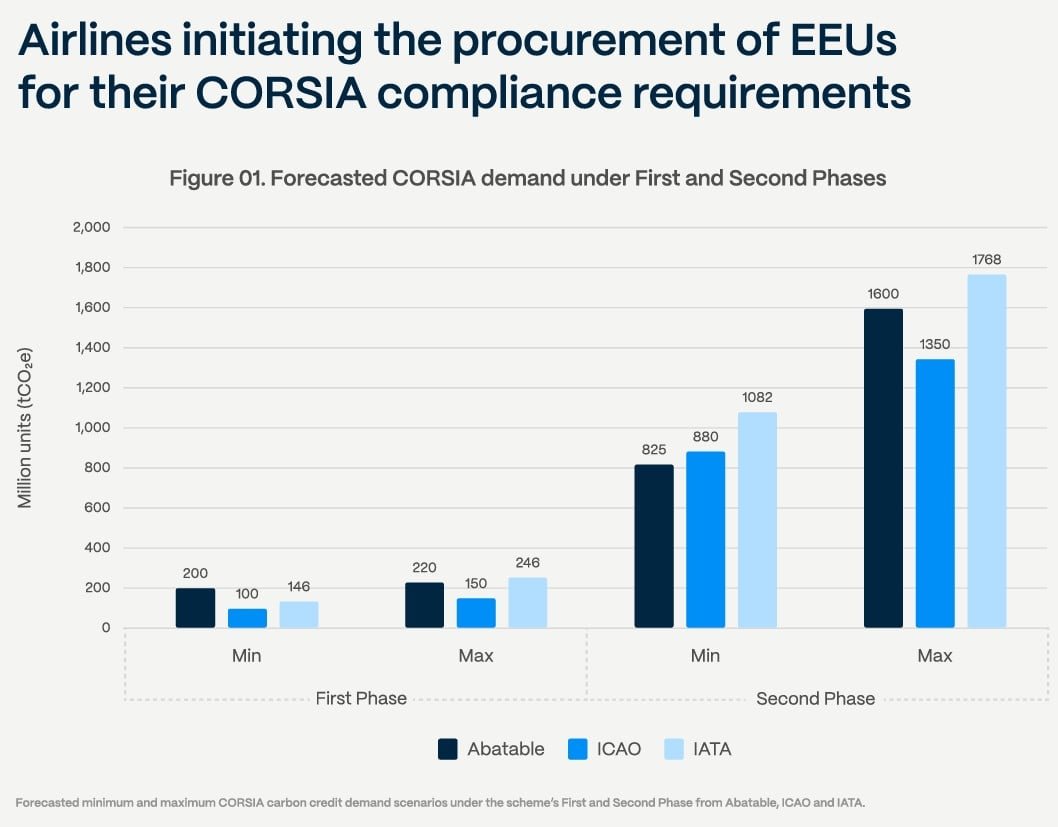

CORSIA is the world’s first global market-based system designed to reduce emissions from international aviation. The International Civil Aviation Organization (ICAO) created a rule that requires airlines to offset emissions growth on eligible international routes. They must do this by buying approved carbon credits.

The program entered its first compliance phase in 2024 and will expand over the coming years as more countries participate. More than 120 nations have committed to CORSIA, making it one of the world’s largest international carbon markets.

CORSIA is different from the broader voluntary carbon market (VCM). It only accepts credits from programs that follow strict standards. These include environmental integrity, permanence, transparency, and independent verification. ICAO has approved only a limited number of carbon credit standards and methodologies.

As a result, airlines cannot simply buy the cheapest credits. They must compete for a much smaller pool of eligible credits, increasing the risk of shortages as demand grows.

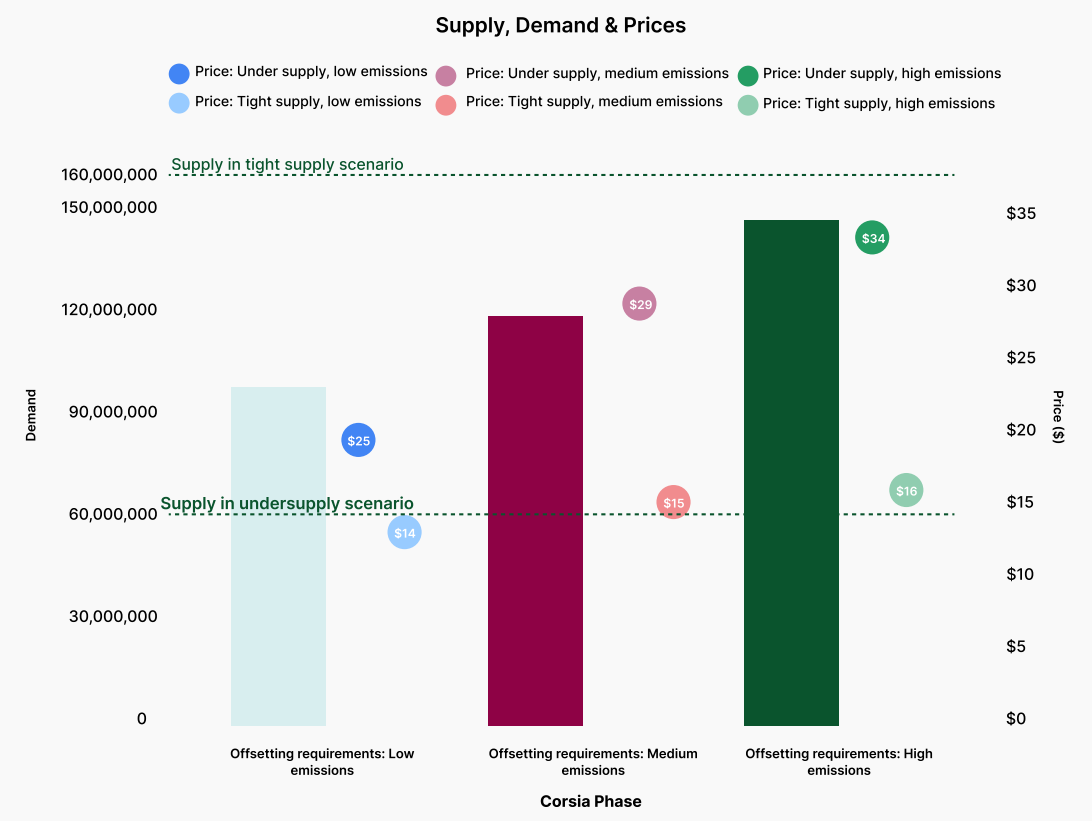

MSCI Carbon Markets says the market might get tight after 2027. This is when more airlines will need to comply, and demand will rise.

A Growing Gap Between Supply and Demand

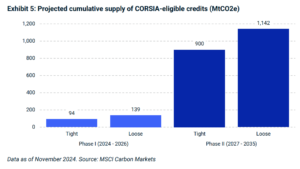

The expected shortage is not caused by a lack of carbon projects. Instead, too few projects meet CORSIA’s eligibility requirements.

The VCM has issued billions of carbon credits over the past two decades. However, many older credits do not qualify under ICAO’s stricter rules. At the same time, developers need years to create, validate, verify, and register new projects before credits can reach the market.

MSCI estimates this imbalance could leave airlines competing for a limited supply of eligible credits throughout the 2030s. Under its tighter supply scenario, compliance costs could reach $127 billion between 2024 and 2035.

The report predicts that CORSIA-approved credits might reach nearly $100 per metric ton by 2035. This is much higher than the current prices in the wider voluntary carbon market.

Some airlines face greater exposure than others. Long-haul international carriers like Emirates, Qatar Airways, and United Airlines will likely need the most eligible credits. This is due to their vast global networks.

- Emirates could face $8 billion in compliance costs, followed by Qatar Airways ($6 billion) and United Airlines ($5 billion), per FT report.

The challenge comes as many airlines are already dealing with higher fuel costs, aircraft shortages, and growing investments in sustainability.

Aviation’s Climate Challenge Continues to Grow

The pressure reflects aviation’s broader emissions challenge.

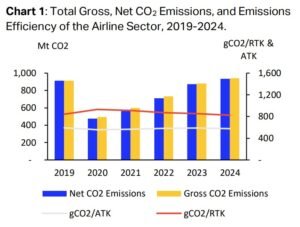

According to the International Energy Agency (IEA), aviation accounts for around 2% of global energy-related carbon dioxide emissions. Yet, it remains one of the fastest-growing transport sectors because passenger demand continues to outpace efficiency gains.

The Air Transport Action Group (ATAG) estimates that in 2024, commercial aviation emitted around 942 million metric tons of CO₂. This is nearly back to pre-pandemic levels. Without stronger climate action, emissions could keep rising over the coming decades.

The industry has responded with ambitious climate goals. Through IATA, airlines have committed to reaching net-zero emissions by 2050. To reach that target, we need better aircraft, sustainable aviation fuel (SAF), operational upgrades, hydrogen and electric planes, and carbon removal.

Most experts agree that carbon credits will still be vital during the transition. This is especially true for emissions that we can’t eliminate yet.

Sustainable Aviation Fuel Cannot Close the Gap Alone

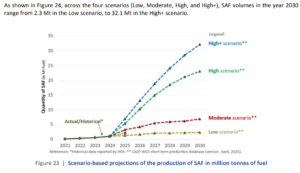

The aviation industry sees sustainable aviation fuel as its biggest long-term tool for cutting emissions. Depending on the feedstock and production method, SAF can reduce lifecycle greenhouse gas emissions by up to 80% compared with conventional jet fuel.

However, supply remains well below demand.

According to IATA, SAF production reached about 2.4 million metric tons in 2025, or roughly 2.5 billion liters. Despite rapid growth, it will supply only about 0.7% of global jet fuel demand this year.

The industry aims to expand production much faster. Under IATA’s net-zero roadmap, SAF could deliver about 65% of aviation’s emissions reductions by 2050. Reaching that goal will require hundreds of billions of dollars in investment and a major expansion of production capacity worldwide.

Until then, airlines will continue relying on carbon credits to offset emissions that cannot yet be avoided. That is why analysts expect demand for high-quality credits to remain strong over the next decade.

Higher Credit Prices Could Reshape Carbon Markets

Growing CORSIA demand could affect the broader carbon market. In recent years, voluntary carbon markets have struggled with low prices and concerns about credit quality. Many lower-quality credits traded for only a few dollars per metric ton as buyers became more selective.

CORSIA could help reverse that trend.

ICAO only accepts credits that meet strict environmental standards. This gives developers a strong reason to create high-quality carbon removal and avoided-emissions projects. These projects can then qualify for compliance markets.

This change could boost investment in several areas:

- Reforestation,

- Afforestation,

- Direct air capture (DAC),

- Bioenergy with carbon capture and storage (BECCS),

- Improved soil carbon, and

- Other lasting carbon removal projects.

Market analysts expect buyers to continue prioritizing quality over low prices. That trend is already visible as companies pay premiums for credits backed by stronger verification and long-term climate benefits.

Higher prices could help project developers. This change can improve project economics and make it easier to fund carbon removal technologies that have had trouble attracting investment.

The Aviation Transition Will Require More Than Offsets

Carbon credits alone will not solve aviation’s climate challenge. Airlines need to invest in:

- Fuel-efficient aircraft,

- Sustainable aviation fuel,

- Operational improvements, and

- Future technologies like hydrogen and electric aircraft, when possible.

Governments will also need to support SAF production, modernize air traffic systems, and encourage investment in low-carbon aviation infrastructure. Even so, carbon markets will remain an important bridge during the transition.

The growing shortage of CORSIA-eligible credits reflects a broader shift across global carbon markets. Buyers are no longer looking for the cheapest offsets. They increasingly want credits that meet higher standards for quality, transparency, and measurable climate impact.

For airlines, this means climate compliance is becoming more complex and more expensive. For the carbon market, it signals a move toward higher-value credits backed by stronger environmental integrity.

If current projections prove correct, the next decade will not be defined by how many carbon credits are available. Instead, it will depend on how many truly high-quality credits the market can deliver.

- READ MORE: Carbon Markets Go Financial with Abatable Launching First Forward Pricing Curve for Carbon Credits

The post Airlines Face a $127 Billion Carbon Credit Bill as CORSIA Supply Tightens appeared first on Carbon Credits.