The Middle East and North Africa (MENA) is rapidly transforming from a fossil fuel-dominated region into one of the world’s fastest-growing clean energy markets. Governments are investing heavily in solar, wind, and green hydrogen while setting ambitious climate targets that are reshaping their long-term energy strategies.

The region’s combination of abundant sunshine, strong wind resources, competitive project costs, and supportive government policies is attracting billions of dollars in investment. As renewable projects move from planning to construction, MENA is positioning itself as a global leader in the clean energy transition.

Renewable Targets Are Driving a Regional Energy Shift

Climate ambition across MENA has accelerated significantly over the past few years. According to the International Energy Forum’s (IEF) Progress Report for MENA NDCs and Climate Action, most countries in the region have strengthened their renewable energy commitments under their Nationally Determined Contributions (NDCs).

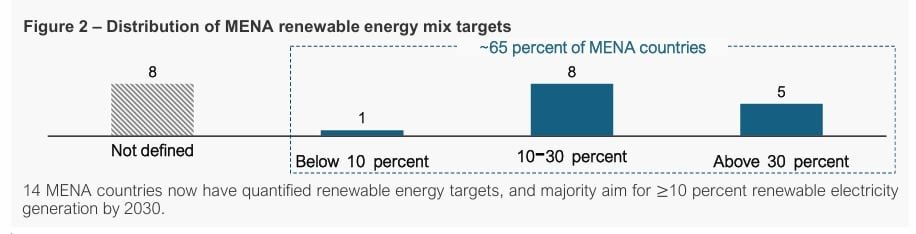

As of 2024, 14 MENA countries had included explicit renewable energy targets in their climate plans. Twelve countries expressed these goals as a share of electricity generation, with many aiming for renewable electricity to account for at least 30% of their power mix by 2030. Four countries instead adopted capacity-based targets measured in gigawatts (GW).

Beyond their 2030 commitments, many governments have also introduced long-term strategies extending to 2050. These plans include net-zero emissions goals and higher renewable energy shares, signaling that clean electricity is becoming a central pillar of national economic development rather than simply a climate initiative.

Although each country follows its own pathway depending on its resources and existing energy system, the overall direction is consistent. Governments are working to diversify electricity generation, improve energy security, reduce emissions, and create new industries that support long-term economic growth.

Together, these commitments represent a structural shift in how the region plans its future energy system.

Solar Leads an Unprecedented Expansion

Solar power has become the engine behind MENA’s renewable energy growth.

- The IEF estimates the region could install between 220 GW and 450 GW of solar photovoltaic (PV) capacity by 2035, allowing solar to provide roughly 25% of regional electricity generation.

This rapid expansion is supported by some of the world’s most competitive renewable energy markets. Public auctions held across the region have consistently produced record-low electricity prices.

In 2024, utility-scale solar projects achieved prices between $10 and $13 per megawatt-hour, while onshore wind projects secured bids ranging from $16 to $17 per megawatt-hour.

Several factors explain these exceptionally low costs:

- Excellent solar irradiation across desert regions

- Large-scale project development

- Long-term power purchase agreements

- Strong government support that lowers investment risk

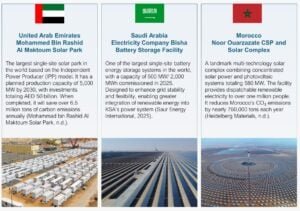

The region is also home to several of the world’s largest renewable energy developments. Dubai’s Mohammed bin Rashid Al Maktoum Solar Park, for example, is expanding toward 5 GW of installed capacity, demonstrating how MENA countries are building renewable projects at a scale rarely seen elsewhere.

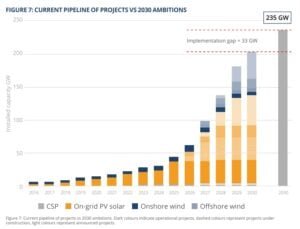

Project Pipeline Shows Strong Momentum

Recent data from Dii Desert Energy indicates that the region has entered what it describes as an “exponential growth phase.”

Operational renewable capacity reached 43.7 GW by the end of 2025, while the total development pipeline climbed to approximately 202 GW. This growing pipeline places the region much closer to achieving its renewable energy ambitions for 2030.

Solar continues to dominate the expansion.

Installed solar PV capacity increased to 34.5 GW by the end of 2025, representing a sharp rise compared with previous years. Even more impressive is the development pipeline, where solar accounts for roughly 130 GW of future capacity.

Together, these figures suggest that renewable deployment across MENA is accelerating rather than slowing, with utility-scale projects driving most of the growth.

Saudi Arabia and the UAE Are Setting the Pace

Several countries are emerging as regional leaders, but Saudi Arabia has become the primary growth engine.

- The kingdom nearly tripled its renewable capacity within a single year, increasing operational capacity to 11.7 GW.

- Massive investments, supported by the country’s Vision 2030 strategy, continue to drive renewable deployment at an unprecedented pace.

Saudi Arabia also boasts some of the world’s lowest renewable electricity costs, helping attract both domestic and international investors.

The United Arab Emirates remains another major clean energy leader.

Construction is underway on a groundbreaking 5.2 GW solar project paired with 19 GWh of battery storage, designed to provide 1 GW of continuous baseload renewable electricity. The project demonstrates how large-scale battery storage is becoming an essential component of the region’s renewable energy strategy by improving grid reliability and reducing dependence on conventional power generation.

Wind Energy Continues to Gain Ground

Although solar dominates new installations, wind energy is steadily expanding across the region. Operational wind capacity reached 7.4 GW, while another 65 GW remains under development.

- Egypt currently leads MENA with more than 3 GW of installed wind capacity, followed by Morocco with approximately 2.4 GW.

Much of the recent growth came from Egypt, where two major projects entered operation during 2025.

The Amunet Wind Farm added 505 MW, while the Red Sea Wind Energy Phase II project reached its full 650 MW capacity. Morocco also expanded its renewable portfolio by completing the 60 MW Dakhla Desalination Wind Farm.

- Looking ahead, Saudi Arabia is expected to become one of the largest wind markets in the region. Several major projects have already secured financing, including the 2 GW Starah Wind Project and the 1 GW Shaqra Wind Project. Both developments are expected to begin operations between late 2027 and early 2028.

Although wind deployment is progressing more slowly than solar, the growing pipeline indicates that it will remain an important part of MENA’s diversified renewable energy mix.

Green Hydrogen Is Becoming the Next Growth Opportunity

Beyond electricity generation, MENA is increasingly positioning itself as a future global supplier of clean hydrogen.

The International Energy Forum notes that hydrogen has become a central feature of regional climate strategies since 2022. Governments increasingly view hydrogen as both a decarbonization tool and an opportunity to build entirely new export industries.

Hydrogen can help reduce emissions in sectors that are difficult to electrify, including steel production, chemicals, aviation, shipping, and heavy industry. It can also improve energy storage and strengthen long-term energy security.

Green hydrogen, produced using renewable electricity and electrolysis, dominates regional plans. According to the International Renewable Energy Agency (IRENA), more than 85% of announced hydrogen capacity across MENA involves green hydrogen projects.

However, several Gulf countries are also investing in blue hydrogen, which combines natural gas with carbon capture technologies. Policymakers see blue hydrogen as a practical transition pathway that can generate export revenues while renewable electricity capacity continues expanding.

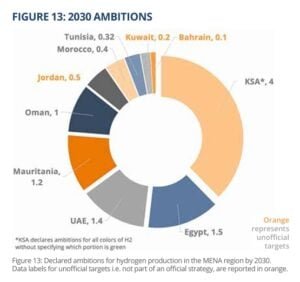

Today, 17 MENA countries have launched hydrogen-related initiatives through national strategies, pilot projects, partnerships, or memoranda of understanding.

- Many governments envision producing between 5 million and 10 million tonnes of clean hydrogen annually by 2040, aligning these plans with broader net-zero commitments extending to 2050.

Projects Are Advancing, but Challenges Remain

Despite ambitious announcements, commercial hydrogen deployment remains in its early stages. According to Dii Desert Energy, only two pilot projects are currently operational across the region. Both are located in the UAE.

DEWA Green Hydrogen Pilot Plant

The first is the DEWA Green Hydrogen Pilot Plant, which operates a 1.25 MW PEM electrolyzer. The second is the Masdar–Emirates Steel demonstration project, which uses green hydrogen to produce low-carbon steel.

By the end of 2025, only five hydrogen projects had reached financial close and moved into construction or early implementation.

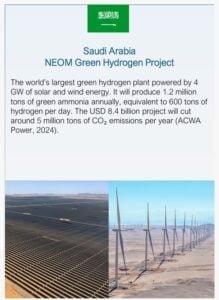

NEOM Green Hydrogen Project

The flagship project remains Saudi Arabia’s NEOM Green Hydrogen Project, currently about 80% complete. Scheduled for commissioning during the first quarter of 2027, the facility will become the world’s largest green hydrogen project.

The project combines 4 GW of dedicated solar and wind power with 2.2 GW of electrolyzers to produce approximately 1.2 million tonnes of green ammonia annually, creating one of the largest renewable-powered industrial complexes ever developed.

Ambition Is High, but Execution Must Accelerate

While long-term goals remain impressive, implementation has not kept pace.

Current estimates place MENA’s planned electrolyzer capacity between 200 GW and 230 GW, although much of this is concentrated within a handful of mega-projects. The 17 largest projects alone account for approximately 118 GW of proposed capacity.

Developers are also scaling back some of the earliest announcements to improve project feasibility. Mauritania’s Project Megaton Moon, for instance, was originally proposed at 35 GW but has since been reduced to 6 GW, reflecting more realistic financing and construction timelines.

Regional hydrogen strategies still target around 10 million tonnes of annual clean hydrogen production by 2030, with green hydrogen expected to contribute the majority of output.

However, progress has been slower than expected. Limited final investment decisions, financing delays, regulatory uncertainty, and infrastructure challenges have pushed back several projects. As each year passes without significant construction activity, achieving the 2030 production target becomes increasingly difficult.

Even so, MENA’s overall clean energy trajectory remains firmly upward. Rapid solar deployment, expanding wind capacity, competitive renewable electricity costs, and growing hydrogen investments are steadily reshaping the region’s energy landscape.

The post From Oil to Renewables: How MENA Is Reshaping the Global Energy Future appeared first on Carbon Credits.