On a Manhattan rooftop during NY Tech Week, we brought together the people working on physical AI for a sunny, lively breakfast. Co-hosted by Sightline, Planeteer Capital, Blackhorn Ventures, and Foley Hoag, it drew the builders, funders, and operators behind robotics (even if the robots couldn't make it).

Robotics is having a moment right now. The money is flowing in, the videos of humanoids doing backflips are going viral. But beyond that, it's the Waymo in your city, the drone on a wind farm, the warehouse system rerouting itself at 3am.

We know, we know. "Is a robot something you should read about in a climate tech newsletter?" "Why are we even writing about this?" Because the sectors where autonomous robots are most needed – manufacturing, energy infrastructure, construction, mining – are the same ones central to the energy transition.

At Sightline Climate, we've been deep in this space with clients. And this Physical AI x Robotics at NY Tech Week conversation was so good that we wanted to bring it to CTVC readers. So here, we’re bringing you an explainer of the robotics market, some takeaways from the event, and (bonus!) a market map with the startups doing the work.

Why robotics, why now

A robot used to mean a machine programmed to do one thing, perfectly and repeatedly. Now, with physical AI as the intelligence layer, machines can perceive their environment, make decisions, and act, without being explicitly programmed for every situation they encounter.

For a climate tech newsletter, they’re a big deal. Robots are, at the same time, new load (every robot running real-time inference at the edge needs cheap, clean, reliable power); a potential efficiency unlock (autonomous inspection drones on wind farms, robots doing solar O&M, predictive maintenance cutting industrial energy waste); and a supply chain bet (reshoring manufacturing only works if automation can compensate for labor that’s aging and disappearing).

So how’d we get here? A lot has to do with physical AI getting meaningfully better. Perception, task planning, and real-time decision-making are good enough now to push into environments that were too unpredictable to automate a few years ago. Meanwhile, aging and demographic shifts mean that labor is disappearing. The US faces a 2.1m manufacturing worker shortfall by 2030, and half the mining workforce retires by 2029. Construction needs 500,000 new workers this year alone. And reshoring, a political priority across both Biden and Trump, can’t happen without a labor force. Still, capital is flowing in. Global robotics funding nearly doubled in 2025. The entire industrial robotics market is worth roughly $20bn.

The headwinds are there too, though. The humanoid hype is getting ahead of the market. Pre-revenue humanoid company Figure AI was last valued at $39bn, roughly twice the size of the entire industrial robotics market.

Automation already has an approval problem. AI has a lower approval rating than Congress right now, and the jobs narrative isn't helping. "As investors and builders, we should insist on measuring two things in every deployment: net job quality and wage impact, and real safety outcomes," Micah Kotch of Blackhorn Ventures said at the event.

And deployment costs more than it looks. Most factories weren't designed for robots. If the robot costs $100, budget another $100 for integration and another $100 for lifecycle support, panelists said. And even once deployed, pilots run at 80-90% reliability, but production requires 95-99%. And that's all before the China supply chain dependency.

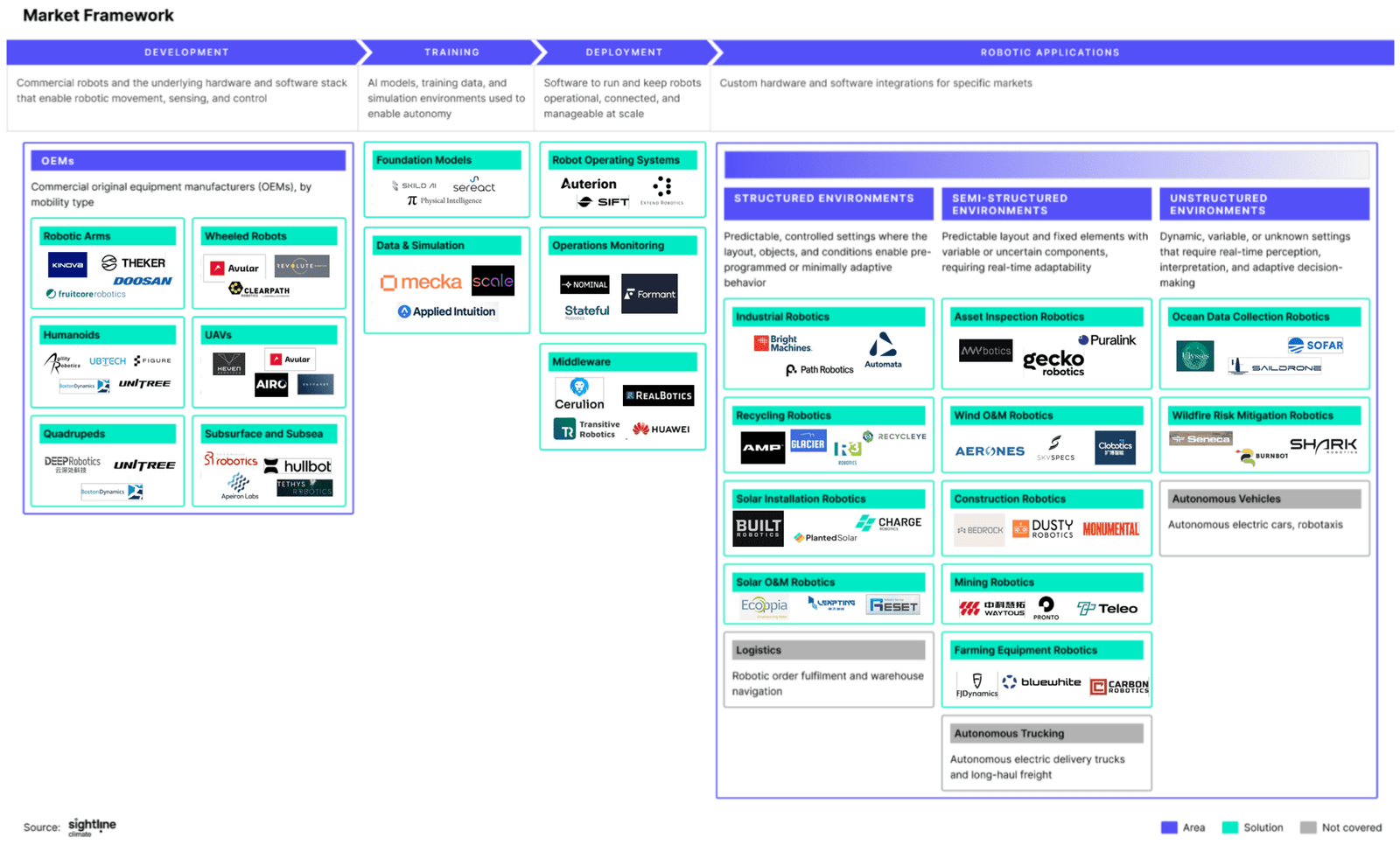

How the market works

The robotics market spans the full stack from hardware to application, and where value accrues is still being worked out. At one end, OEMs building the physical hardware: robotic arms, humanoids, drones, wheeled robots. Then the intelligence layer: foundation models, simulation, data. Then deployment infrastructure: operating systems, monitoring, middleware connecting robots to enterprise systems. And finally the applications themselves, organized by environment complexity. China owns much of the hardware end of that stack already.

China vs. the West on robotics

You can't have a robotics conversation without talking about China. We’ve been to China twice in the last six months visiting EV, battery, solar, and robotics companies. The thing that stood out most: full consumer and corporate adoption of AI and robotics in a way that doesn't have a US equivalent. BYD, the world's leading EV company, now tests new AI and technology in China first, then exports whatever goes mainstream internationally.

The policy machine is a big part of it. China's new five-year plan names physical AI and robotics as a national priority (the same playbook it ran on EVs, solar, and batteries) The government plays three roles at once: regulator, anchor customer, and venture partner. Local governments build factories, provide offtake agreements, and lease facilities back to companies at a discount. The result is a coordinated national framework covering data, deployment, standards, and procurement that the US simply doesn't have.

The hardware gap is big and growing: Unitree, a Chinese robotics company that has become shorthand for how quickly Chinese hardware has closed the capability gap with the West, produces 25,000 robots a year, roughly five times the output of all US-native providers combined. The one lane where the West retains advantage is in sensitive industrial environments where security concerns make Chinese open-source models a non-starter, and in high-mix, low-volume applications like defense and aerospace, as an audience member said. But that window isn't open forever.

What we heard

1. Deployment is the bottleneck. The room largely agreed that the biggest challenge is getting robots onto factory floors and keeping them running. "Deployment is the bottleneck," Kotch said. “We get really excited about companies that are solving for that deployment challenge, because fundamentally there's a lot of kinetic risk in deploying these systems in the real world, whether that's on the factory floor or within utility infrastructure or at a warehouse or what have you.”

The most interesting response from the market isn't always better hardware, it's business model innovation. Charging an hourly rate for robot output rather than selling hardware upfront, the PPA equivalent for robots, is the model Blackhorn has backed and believes in.

2. Incumbents are treating AI as an annuity, not a feature. Large industrial players aren't racing to build new robots. They're layering AI on top of existing physical assets – anomaly detection, predictive maintenance, OEE optimization – and generating recurring software revenue from hardware bases worth tens of billions. "Whoever owns the data on the line and understands the upgrade cycle, that's where the value ultimately accrues," Kotch noted. But he added that while most of these companies know how to sell hardware, selling software is a different motion entirely.

3. The physical singularity is coming, just not yet. As Stephan Cizmar of Blackhorn Ventures said: "The jobs to be done are substantially larger and more complex in the real world." Software AI will hit its inflection point first. But physical AI's compute and inference demands will ultimately be larger — every robot running real-time inference at the edge needs cheap, clean, reliable power. The opportunity is enormous. The timeline is longer than the valuations suggest.

4. The knowledge gap is as big as the labor gap. It's not just that workers are retiring — it's that they're taking decades of expertise with them. "Physical work still has to happen," one operator said at the event. "You've got an older generation that's leaving and a younger generation coming in, and that gap is a real challenge." One multinational company mentioned that this is its main use case for deploying physical AI today.

Thanks to Micah Kotch and Stephan Cizmar of Blackhorn Ventures for their insights, as well as Planeteer Capital and Foley Hoag for hosting a great event!

CTVC is powered by Sightline Climate, the tactical market intelligence platform for energy and investment decision-makers.