Happy Monday!

Sightline Climate has just released a new report, The Fastest MW, our new analysis covering 700+ generation projects with identified speed advantages, mapped against data centers in development, to understand how to get clean, firm power, ASAP. Download it here and read below for the Powerstack take. And sign up for our webinar on May 29 to hear about it live.

In deals, $275m for vertically integrated space infrastructure and orbital AI systems, $150m for vertical strawberry farming and controlled environment agriculture, and $65m for satellite power network infrastructure.

In other news, the massive utility merger, Crux gets into the investment game, and Ford gets into stationary storage.

Thanks for reading! Not a subscriber yet?

📩 Submit deals and announcements for the newsletter at hello@ctvc.co.

💼 Find or share roles on our job board here.

CTVC is powered by Sightline Climate, the tactical market intelligence platform for energy and investment decision-makers.

The Fastest MW

What happened

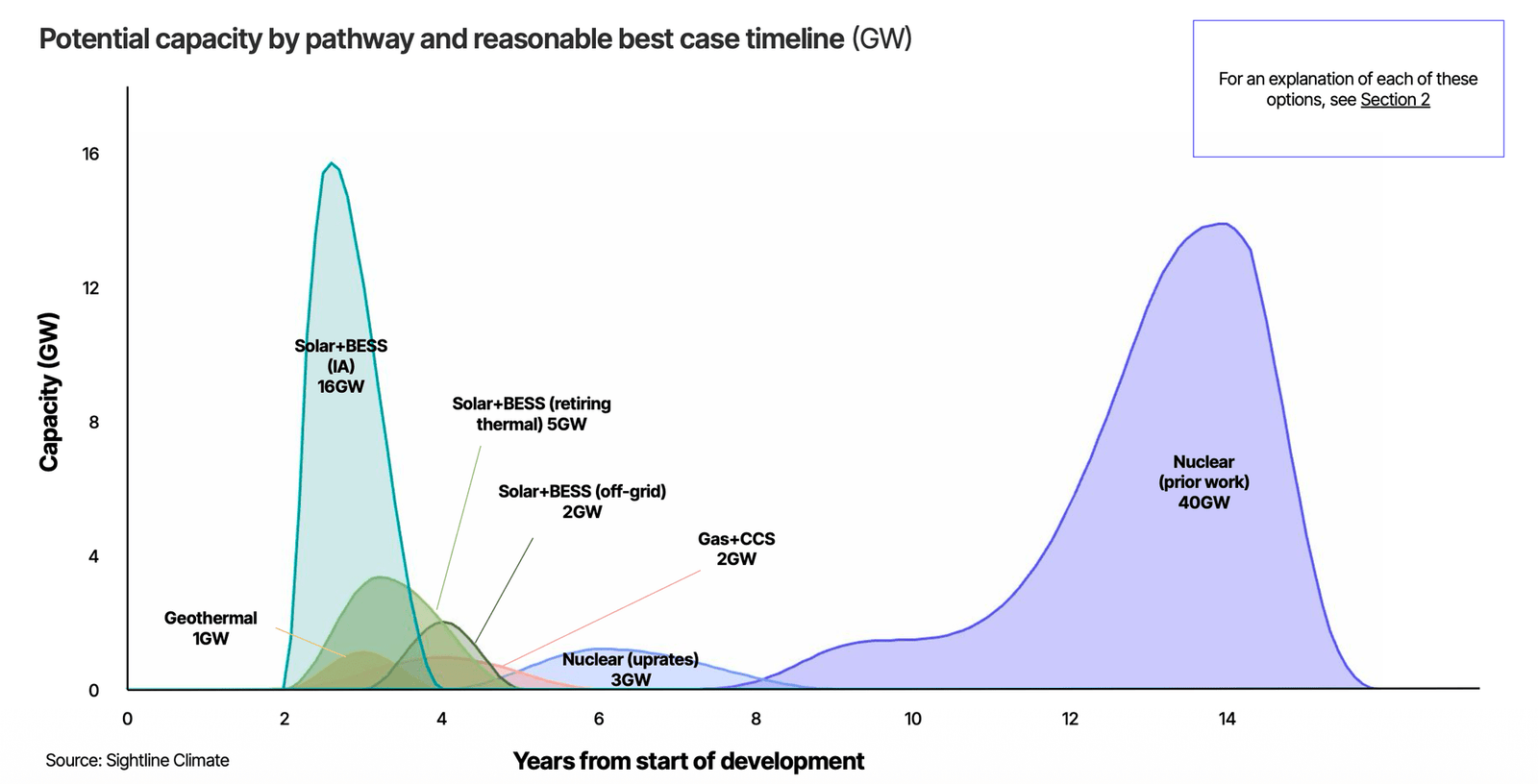

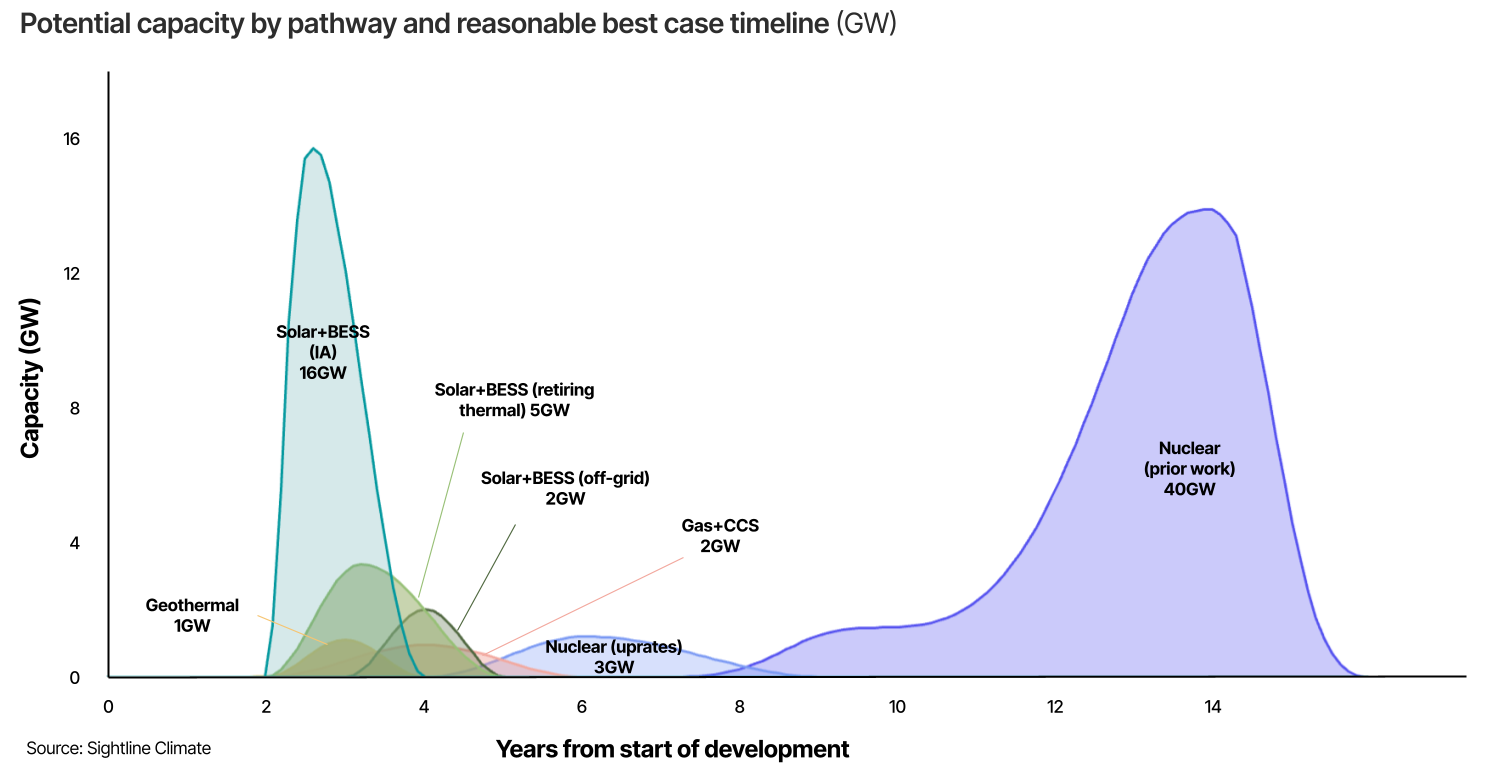

Sightline Climate just released a new report: The Fastest MW.

At this point, two things about AI and data centers are basically table stakes – that the hyperscaler with the most compute has an advantage over its peers, and that the most compute is rate-limited by access to power.

This race to procure the most capacity has put hyperscalers, and pretty much everyone else in the US power market into a stance of what we’ve been calling energy hoarding or, the new gold rush.

But with data center demand expected to be in excess of 100GW across 441 announced grid-connected US data center projects, there are no easy powering options left. Gas turbine lead times are stretching to three years or more, and most off-grid proposals are still hard to finance and harder to build. So power developers, hyperscalers, and utilities are getting creative about where to find that fastest megawatt.

To understand which strategies are proving to be the fastest and cleanest routes to new capacity in the US, we mapped all out – that is, every realistic pathway for grid-connected data center clean power that could yield any speed advantage. Everything from nuclear new builds and uprates to solar + BESS to geothermal to gas + CCS and more. You can download the report here.

The full report with the complete data set for all projects is available for Sightline clients here.

If you’re a hyperscaler, data center developer, or utility we mapped out every possible new generation project – that’s 700+ generation projects mapped, sized, and scored. Talk to our team if you’re interested in the report and dataset.

Mark's Take

We were talking with an investor friend a few weeks ago and they said when it comes to data center development right now, and more specifically, powering data centers, it’s ‘speed, speed, speed, cost, then climate.’ With all the strategies we’ve been covering in Powerstack – from regulatory capture, to off-grid gas – that certainly appears to be true.

Perhaps unsurprisingly, but crucially, one finding from the report is that the fastest MW right now is not a new gas turbine, but a grid connection. This can be an existing connection at a retiring thermal site, or a connection at a new site with an interconnection agreement in place. What this gets you is optionality – to install gas turbines if you have them, or solar plus BESS. The market is figuring this out in real time, resulting in some of the biggest platform plays we’ve seen in awhile, like Google buying Intersect Power for $4.75bn, GIP and EQT buying AES for $10.7bn, and potentially NextEra buying Dominion…more on that in Powerstack this Thursday. 👊

In this new gold rush, interconnection agreement holders first will stake claim on a structural cost and timing advantage that's very hard for others to beat.

Who this helps

- Developers with IA-ready solar+BESS, especially in ERCOT

- Geothermal operators at underperforming existing sites

- Nuclear fleet owners who can offer uprates near planned data center clusters.

Who should be nervous

- Hyperscalers pursuing nuclear as their prime option

- Data center developers caught up in the gas frenzy, defaulting to assuming it was the only fast option

- Off-grid mega-campus boosters whose financing assumptions depend on timelines that the data doesn't support

In the report, we go through each of these options and more to give a picture of what strategies will work, and who stands to win (or, ahem, not win).

Deals of the Week (5/11 – 5/17)

VC / Growth

☀️ Cowboy Space Corporation, a San Carlos, CA-based vertically integrated space infrastructure developer, raised $275m in Series B funding from Index Ventures, Andreessen Horowitz (a16z), Blossom Capital, Breakthrough Energy Ventures, Construct Capital, and other investors.

🌾 Oishii Farm, a Kearny, NJ-based strawberry vertical farming operator, raised $150m in Series C funding from SPARX Asset Management, Mizuho Bank, MISUMI Group, and Nomura Real Estate Development.

🛰 Star Catcher, a Jacksonville, FL-based developer of power networks for satellites, raised $65m in Series A funding from B Capital Group, Cerberus Ventures, Shield Capital, GreatPoint Ventures, Helena, and others.

🏠 Skeleton Technologies, a Tallinn, Estonia-based graphene-based ultracapacitors developer, raised $39m in Growth funding from Axon Partners Group, CBMM, SmartCap, and Taiwania Capital.

⚡ Mantle8, a Grenoble, France-based natural hydrogen exploration technology developer, raised $36m in Series A funding from Sandwater, Breakthrough Energy Ventures, Bpifrance, Calderion, IP Group, and other investors.

🏠 Iceotope, a Sheffield, England-based developer of liquid cooling for data centers, raised $26m in Series B funding from Barclays Climate Ventures, Two Seas Capital, British Business Bank, Edinv, Northern Gritstone, and other investors.

🌿 ECOncrete, a Newark, NJ-based nature-inclusive infrastructure technology provider for coastal and marine construction projects, raised $14m in Series A funding from Builders Vision and Barclays Climate Ventures.

⚡ Casimir, a Houston, TX-based quantum vacuum energy chip developer, raised $12m in Seed funding from Scout Ventures, Cottonwood Technology Fund, Capital Factory, Lavrock Ventures, and American Deep Tech.

⚡ Elvy, a Stockholm, Sweden-based home energy and electrification platform, raised $8m in Seed funding from Essential Capital and Daft Capital.

🌿 Resurrect Bio, a London, England-based crop gene-editing technology provider, raised $2m in Series A funding from Corteva, AgFunder, Calculus Capital, PYMWYMIC, SynBioVen, and other investors.

🧪 Melazyme, a Holladay, UT-based melanin via fermentation producer, raised $2m in Seed funding from SeaX Ventures, Plug and Play Ventures, and Stellaris Venture Partners.

Project Finance / Debt

⚡ MN8 Energy, a New York City-based enterprise solar energy provider, raised $650m in Debt funding from J.P. Morgan Asset Management, Wells Fargo Bank, Bank of America, Crédit Agricole Corporate and Investment Bank (CIB), and other investors.

⚡ Grenergy Renovables, a Madrid, Spain-based renewable energy developer and independent power producer, raised $134m in PF Debt funding from BNP Paribas, KfW IPEX Bank, Natixis Corporate & Investment Banking, Rabobank, and Scotiabank (Bank of Nova Scotia).

💧 Fitt Group, a Sandrigo, Italy-based thermoplastic hoses designer and manufacturer, raised $129m in Debt funding from BNP Paribas, Cassa Depositi e Prestiti (CDP), Crédit Agricole, and UniCredit Group.

Exits

⚡ Fervo Energy, a Houston, TX-based geothermal project developer, completed a $1.9bn IPO at an implied valuation of $7.7bn.

🥩 Unconventional, a Bologna, Italy-based plant-based food developer, was acquired by Amadori for an undisclosed amount.

⚡ Noble Environmental, a Pittsburgh,PA-based waste management provider offering collection, hauling, disposal, and renewable natural gas production, was acquired by Apollo for an undisclosed amount

⚡ Liquid Wind, a Göteborg, Sweden-based commercial-scale electrofuel facilities developer, filed for Bankruptcy/ Out of business.

Funds

🌍 Lightrock, a London, England-based sustainability-focused private equity investor, closed $500m for Accelerate7, a fund targeting growth-stage clean energy access across Sub-Saharan Africa, South Asia, and Southeast Asia.

🌾 S2G Investments, a Chicago, IL-based multi-asset investment firm focused on food & agriculture, energy, and oceans, closed $1bn for Solutions Fund I, its debut independent fund targeting growth-stage companies in the "Missing Middle" across North America and Europe.

This is a sample of deals available for Sightline clients. Can’t get enough deals?

Reading List

⚡ NextEra is reportedly buying Dominion in an all-stock deal valuing the combined company at $420bn, potentially creating a utility serving 10m customers across Florida, Virginia, North Carolina, and South Carolina.

This would give NextEra a direct line to Data Center Alley in Virginia, the densest cluster of data centers on earth. With peak electricity demand expected to rise possibly 20%+ by 2035, NextEra is betting scale is the only play. But regulators and Virginia's governor, who wants data centers to pay more for power, still have to sign off.

💰 Clean energy tax credit transfer market startup Crux raised $500m in debt from Nuveen Energy Infrastructure Credit, which it will use to act as a GP (general partner) in clean energy and manufacturing deals.

Crux was built to serve the new tax credit transfer market the IRA created, but as the OBBB eliminates many of those credits, Crux is evolving. This $500m marks its evolution from deal facilitator to deal investor, as other banks step away from some deals due to Chinese supply chain restrictions. As traditional players pull back and demand surges, the gap gets filled by a new class of specialized capital providers like Crux, which already has all the market data.

🔋 Ford officially launched a US stationary energy storage subsidiary, with front-of-the-meter BESS deliveries to begin in 2027. [Link]

Ford pushing into the FTM, which is a Chinese-dominated market, is notable. Ford likely has a play around domestic content, supply chain security, and bundling with its EV manufacturing footprint.

💸 Heatmap covers the state of early-stage climate tech investing (and our Dry Powder 2026 report), with a look at what's actually getting funded right now and what's not. [Link]

Mostly mid-raise, and the early-stage end of the market, has been the most exposed to the broader VC pullback. Heatmap's framing tracks with what we've heard at Sightline.

💨 Hydrogen electrolyzer company Thyssenkrupp Nucera's financial woes deepen, but there’s some fresh optimism from European buyers. Scale-up issues are driving losses, as well as unforeseen technology upgrades at 160 of their electrolyzers, plus the cancellation of a 20MW pilot in the US. [Link]

🔊 Sightline co-founder and CEO Kim Zou was on the Redefining Energy podcast, discussing how climate tech has evolved — from green molecules to green electrons — and Sightline's work tracking data center construction across hundreds of sites. [Link]

🌡 Climate Central launched a Climate Shift Index dashboard, quantifying how much daily temperatures across the US are being shifted by human-caused climate change. [Link]

🌞 Pakistan set a target of 95% renewable electricity by 2040. [Link]

Opportunities & Events

📅 The Fastest MW: Join Sightline Climate’s webinar on the Fastest MW report on May 29 at 11 AM ET to hear how data centers can find speed to power.

📅 Trellis Impact 26: From Jun 23-25 in San Francisco, Trellis Impact brings together 3,500+ leaders powering the future of sustainable business, from AI-enabled solutions to emerging technologies reshaping decarbonization, energy, circularity, and beyond. Get practical insights and hard-won examples of the technologies and strategies that are influencing sustainable business transformation. Register and you can get 20% off with our partner code: TI26SCP

📅 Entrepreneurs for Impact (EFI): Register for a webinar, "BIPOC Founders in Climate Tech: Capital, Credibility, and Community," on May 20th from 12-1 ET. Three climate CEOs discuss scaling startups without the same inherited networks, pattern-matching advantages, or institutional access as their peers.

📅 Scale For ClimateTech: Join on Tuesday, June 16 in New York City or online for 2026 Demo Day, showcasing the 18 climate tech innovators of Cohort 7 who are developing breakthrough hardware solutions across advanced energy storage, circular resource recovery, grid and transportation infrastructure, next-generation materials, and more.

📅 Cox Cleantech Accelerator: The Cox Cleantech Residency is a new six-week, equity-free program that provides funding, mentorship and hands-on support to help early-stage cleantech founders across the Southeast move promising ideas toward commercialization; applications are open through June 28.

Jobs

Head of Finance, Investor @Gigascale

Analyst Trainee, Program Specialist Trainee, Bureau Chief of Budget & Procurement, Deputy Director of Grid Scale Resources, Deputy Director of Virtual Power Plants, Director of Clean Energy Planning & Analytics, Bureau Chief of Grid Scale Resources – Division of Clean Energy, @New Jersey Board of Public Utilities

Marketing Lead, @Glimpse

Senior Associate – Infrastructure, Capital Projects & Climate Advisory @KPMG

Risk Management – Climate, Nature & Social @JPMorgan Chase

📩 Feel free to send us deals, announcements, or anything else at hello@ctvc.co. Have a great week ahead!