China’s Grip on Critical Mineral Refining

See visuals like this from many other data creators on our Voronoi app. Download it for free on iOS or Android and discover incredible data-driven charts from a variety of trusted sources.

Key Takeaways

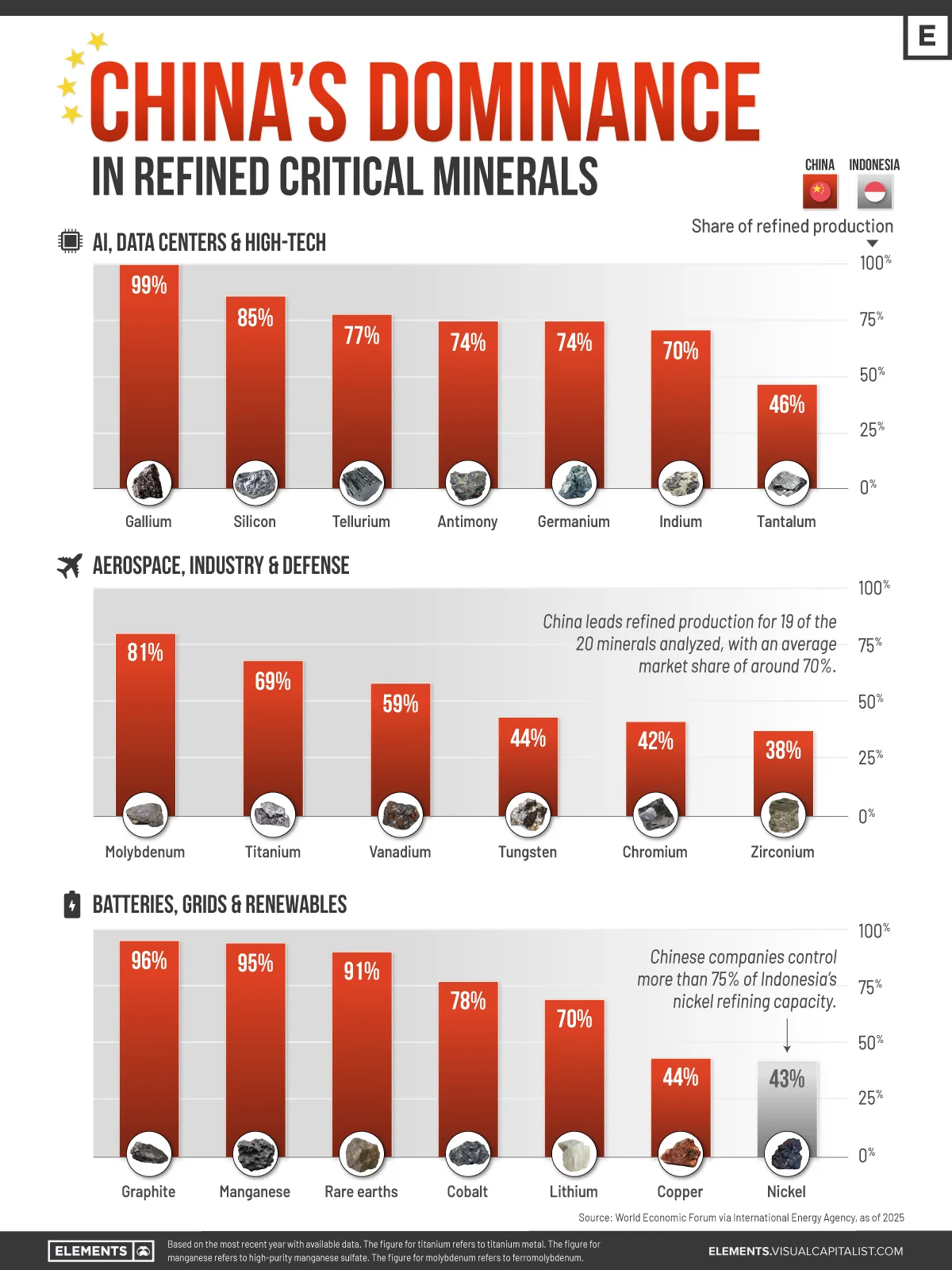

- China leads refining for 19 of the 20 critical minerals analyzed, including materials essential for AI chips, EV batteries, and defense systems.

- China controls 99% of gallium refining and more than 90% of graphite, manganese, and rare earth processing.

- Refining capacity is far more concentrated than mining, creating major supply chain dependencies for the U.S. and Europe.

China has become the world’s dominant processor of critical minerals, refining the materials that power everything from AI chips and data centers to electric vehicles and military hardware.

In many cases, China’s control extends far beyond mining. The country leads refined production for 19 of the 20 minerals analyzed in this visualization, including gallium, graphite, rare earths, and lithium.

The data for this visualization comes from the World Economic Forum, using International Energy Agency figures as of 2025.

China’s Grip on Battery and Electrification Materials

China’s dominance is strongest in the materials powering the global energy transition. The country controls most refining capacity for graphite, manganese, cobalt, lithium, and rare earths, creating major dependencies in EV and battery supply chains.

China accounts for 96% of refined graphite production and 95% of manganese refining, both of which are crucial for battery chemistry and energy storage systems.

| Mineral | Top Refiner | Share of Refined Production | Sector |

|---|---|---|---|

| Graphite |  China China |

96% | Batteries, grids and renewables |

| Manganese | China |

95% | Batteries, grids and renewables |

| Rare earths | China |

91% | Batteries, grids and renewables |

| Cobalt | China |

78% | Batteries, grids and renewables |

| Lithium | China |

70% | Batteries, grids and renewables |

| Copper | China |

44% | Batteries, grids and renewables |

| Nickel |  Indonesia Indonesia |

43% | Batteries, grids and renewables |

| Gallium | China |

99% | AI, data centers and high-tech |

| Silicon | China |

85% | AI, data centers and high-tech |

| Tellurium | China |

77% | AI, data centers and high-tech |

| Antimony | China |

74% | AI, data centers and high-tech |

| Germanium | China |

74% | AI, data centers and high-tech |

| Indium | China |

70% | AI, data centers and high-tech |

| Tantalum | China |

46% | AI, data centers and high-tech |

| Molybdenum | China |

81% | Aerospace, industry and defense |

| Titanium | China |

69% | Aerospace, industry and defense |

| Vanadium | China |

59% | Aerospace, industry and defense |

| Tungsten | China |

44% | Aerospace, industry and defense |

| Chromium | China |

42% | Aerospace, industry and defense |

| Zirconium | China |

38% | Aerospace, industry and defense |

Rare earth processing is another major advantage.

China refines 91% of global rare earth output, materials essential for permanent magnets used in electric vehicles and wind turbines. Even in copper refining, where the market is more diversified, China still leads globally with a 44% share.

Indonesia stands out as the only non-China leader in the dataset, controlling 43% of nickel refining.

However, Chinese companies reportedly control more than three-quarters of Indonesia’s refining capacity, extending Beijing’s influence even where production occurs overseas.

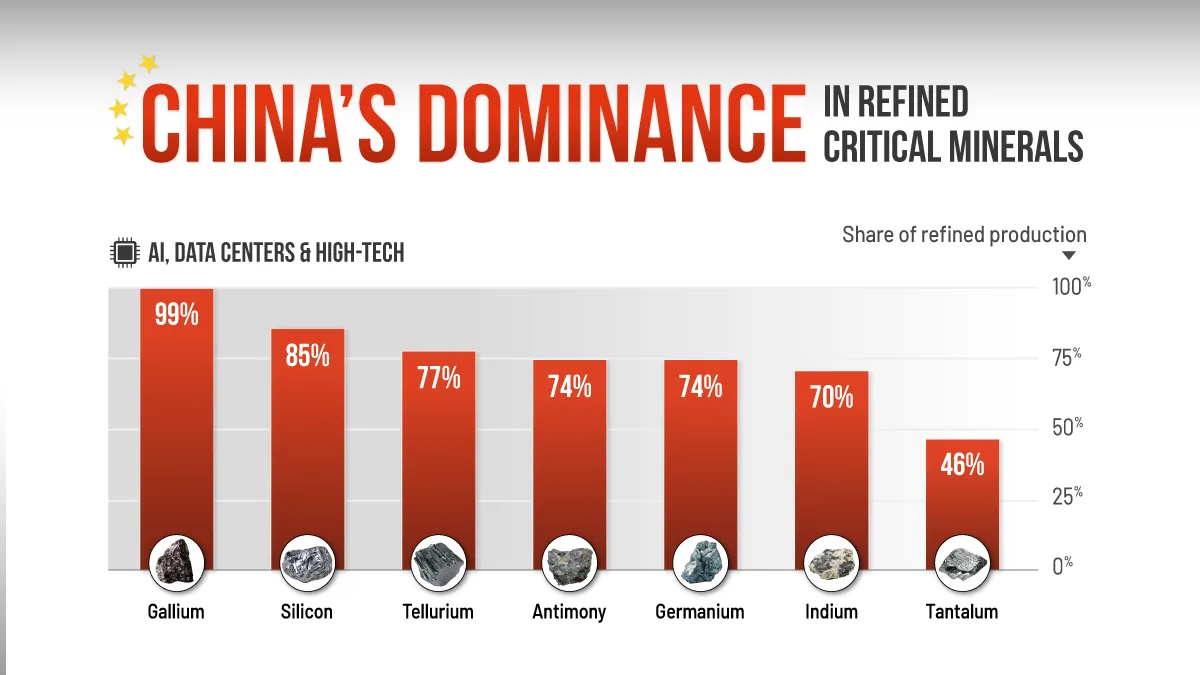

Critical Minerals Powering AI and Semiconductors

The AI boom is rapidly increasing demand for specialized minerals used in semiconductors, fiber optics, power systems, and data center infrastructure. China dominates refining for nearly all of these materials, including gallium, germanium, silicon, and indium.

Gallium is especially notable because China controls 99% of refined production.

The mineral is used in semiconductors, telecommunications equipment, and military electronics. Similarly, germanium and indium are important for fiber optics, solar panels, and advanced chips.

China’s control over these supply chains has become increasingly strategic amid growing technology competition with the United States and Europe.

Export restrictions on minerals such as gallium and germanium have already demonstrated how refining dominance can translate into geopolitical leverage.

Defense and Industrial Supply Chains Remain Concentrated

China also leads refining across minerals tied to aerospace, heavy industry, and defense manufacturing. This includes molybdenum, titanium, vanadium, tungsten, and zirconium.

Many of these materials are essential for producing jet engines, military hardware, industrial machinery, and high-strength alloys.

China controls 81% of molybdenum refining and nearly 70% of titanium refining, giving it substantial influence over industrial supply chains.

While many countries are expanding mining investment, refining remains the hardest part of the supply chain to rebuild. That leaves China in a powerful position across industries tied to AI, energy, semiconductors, and defense manufacturing.

Building new processing facilities can take years, require significant capital investment, and often face environmental and regulatory hurdles. That means China’s current lead may persist even as governments increase investment in domestic mining and supply chain resilience.

Learn More on the Voronoi App

If you enjoyed today’s post, check out Visualizing EU’s Critical Minerals Gap by 2030 on Voronoi.