Happy Monday!

We published a new report this week with HSBC, Offtake to Online: How Corporates Drive Innovation. Read on below for the takeaways about how corporate demand unlocks FOAK project development and beyond, and get the full report.

In deals, $29m for electric bike development in Hong Kong; $28m for fast charging battery development in London; and $21m for plant-based protein production in Breda.

In other news, US court cases rule on air quality and departmental independence, and US hydrogen projects take another hit.

Thanks for reading!

Not a subscriber yet?

📩 Submit deals and announcements for the newsletter at hello@ctvc.co.

💼 Find or share roles on our job board here.

CTVC is powered by Currence, market intelligence to power the AI era.

Corporate demand for FOAK

We've been beating the FOAK drum for years. We’ve written about everything from how to speak the language of FOAK financing, how to cross the dreaded valley of death, how to assemble the right team and partners.

And one of the most meaningful forms of partnership is offtake. Your project or product is only real if someone wants to buy it at the price you’re selling it. Firm offtake commitments are the gold standard for whether a technology is de-risked and a project is bankable, unlocking later stage financing like project finance and debt. And it’s not just funding, but also feedback, test runs, and credibility in the market to bring in additional customers.

That's the premise of our new report, produced in partnership with HSBC: Offtake to Online: How Corporates Drive Innovation. It maps where corporate demand is coming from, how big it could get, and what it takes to turn a sustainability commitment into a contract that actually moves a project, and in turn, a market.

Download the report now, and read on for some takeaways.

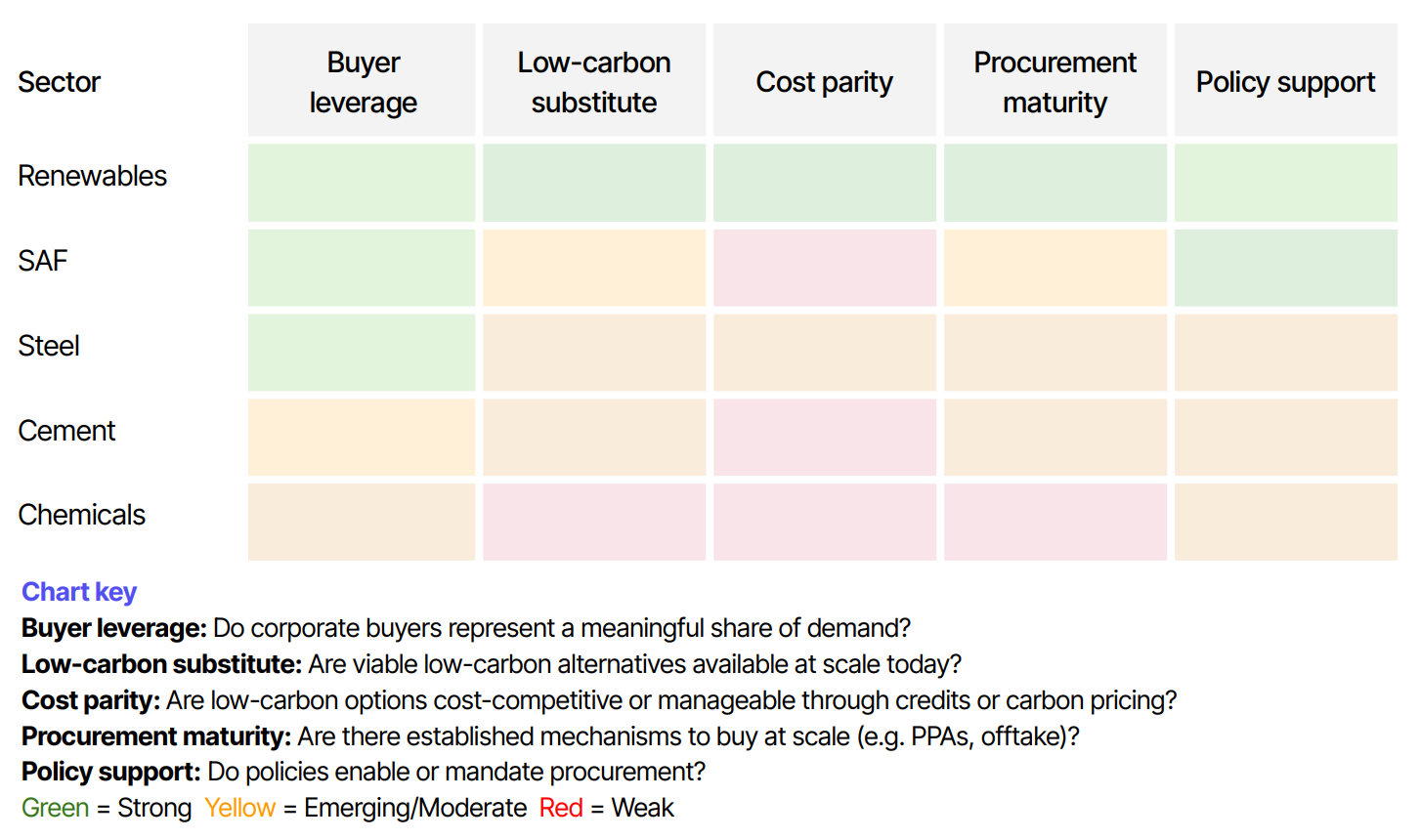

How to scale offtake, sector-by-sector

The speed of corporate offtake and adoption depends on the ecosystem. Where low-carbon options are available and policy supports them, corporate procurement follows. But without them, most companies will default to conditional agreements or partnerships, i.e., sure, if you get your project online, and the price is right, I'll buy from you.

The report dives into five sectors: renewables, sustainable aviation fuel (SAF), steel, cement, and chemicals. It’s a patchwork of progress. Companies buying renewable electricity as part of the RE100 initiative are at 42% of their 100% target, with access tightening as demand grows. Scaling to 100% renewable electricity by 2040 would require increasing procurement to around 544 TWh.

For SAF, rising blending mandates make long-term supply crucial – 2030 SAF blending targets imply demand of approximately 5.2Mt of SAF for major carriers, against roughly 250kt consumed today.

Met-zero goals and buyers clubs like the First Movers Coalition (FMC) kickstarted corporate offtake for low-carbon steel, but it’s mostly recycled content for now, as hydrogen-based steel production has stalled.

Download the full report for the sector-by-sector breakdown.

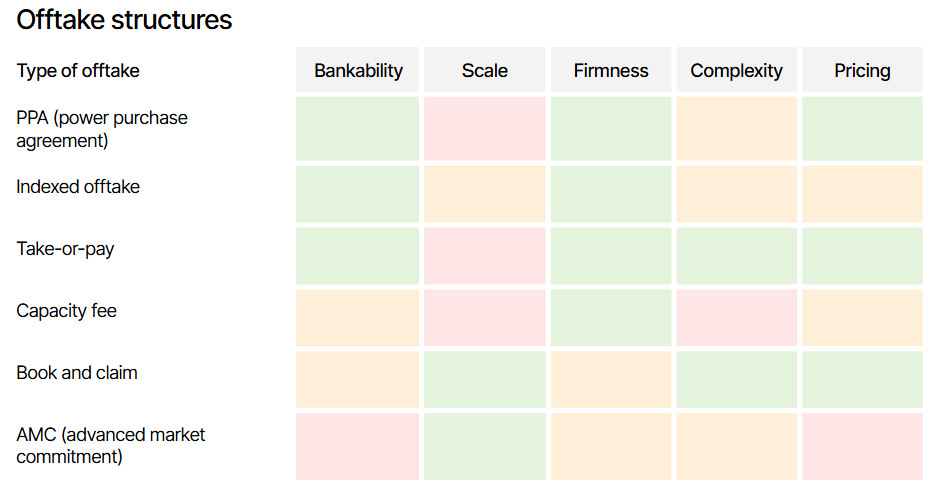

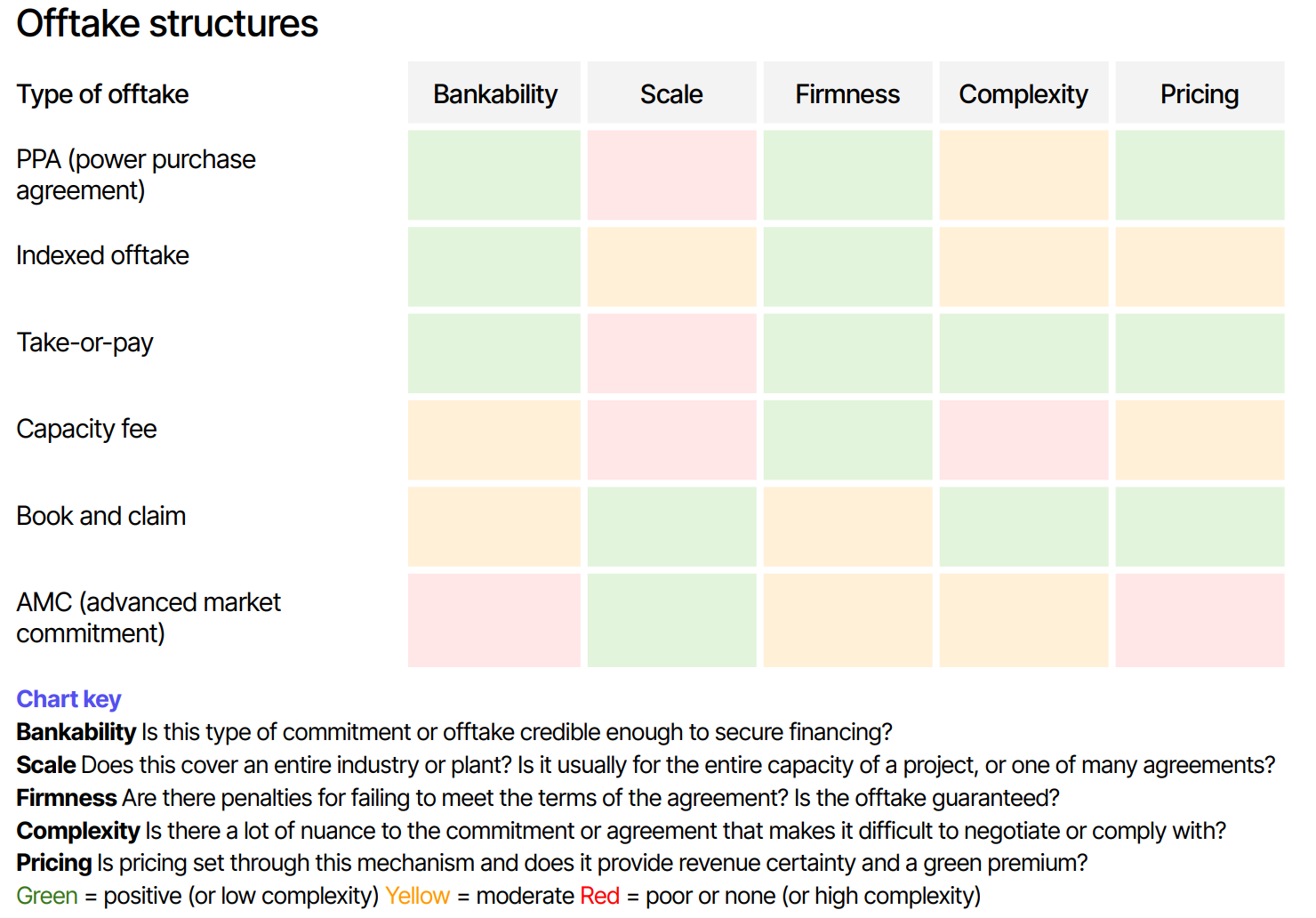

Types of offtake

Offtake can take several different structures, with different purposes. Offtake is sometimes used to give signals to lenders and suppliers on the scale of demand (AMCs, like Frontier for carbon removal), to address a particular supply chain or delivery hurdle (PPAs, book and claim), or to give more certainty and flexibility on pricing (indexed offtake, take-or-pay, capacity fee).

Structures that guarantee a price and a volume are the most bankable, but also often require policy mandates or subsidies from governments as motivating factors in the background. These are typically motivated either by policy, or by corporate sustainability commitments.

Still, not all offtake is the same. In the report, dive into full checklists of what each type requires, plus standards, certifications, implementation, and market coverage. In addition, check out the case studies on how Google and Fervo Energy, IAG and Infinium, Form Energy and Crusoe, and others got these deals done. The intent is to provide a playbook for corporate buyers to understand the options available and how to evaluate them, and give sellers a view into what corporates actually need from a deal.

Key takeaways

Early partnerships secure access to competitive markets. Many procurement mandates have targets far in the future. But capacity can take years to build, and companies that haven’t secured supply early can be left paying the highest prices for constrained supply. If you’ll need a market in the future, early offtake with a premium is the best way to ensure it’ll deliver in time, and start its journey down the cost curve. And not just offtake, as sales channel partnerships, preferential supply agreements, and colocation all reduce project execution risk.

Cost is not the only consideration. Very little early-stage offtake is cost competitive, but co-benefits can still drive procurement. The first solar and wind PPAs offered price certainty, a way to escape the volatility of electricity markets and fuel prices. Offtake contracts today can help hedge supply chain risk, increase deployment speed, or offer supply certainty in competitive (usually compliance driven) markets.

Data centers are some of the best offtakers FOAK has ever had. Price-insensitive, experienced in procurement, and under pressure to move fast. Hyperscalers are already signing deals for enhanced geothermal, long-duration storage, and advanced nuclear at $107-150/MWh. For any clean firm power developer, this is the cheapest path to FID right now.

You can’t escape policy. The strongest offtake agreements are backed by procurement mandates, like the UK and EU’s SAF blending requirements. Even voluntary carbon offset purchases were driven by a belief that carbon pricing or climate risk disclosures would make them mandatory. Corporates drive markets forward, but policy still often creates them.

Deals of the Week (6/29 – 7/5)

VC / Growth

🚗 Urtopia, a Yau Tsim Mong, Hong Kong-based electric bike developer, raised $29m in Series B funding from Brizan Ventures, Gao Bingqiang, Guangyuan Capital, Kungho Fund, and Tongxiang Municipal Government Industrial Fund.

⚡ Gaussion, a London, England-based developer of magnetic control for fast charging batteries, raised $28m in Series A funding from AlbionVC, Business Growth Fund (BGF), Autotech Ventures, DN Capital, Future Ventures, and other investors.

🥩 The Protein Brewery, a Breda, Netherlands-based plant-based protein producer, raised $21m in Series B funding from ABN AMRO, BOM (Brabant Development), Invest-NL, Madeli, and Novo Holdings.

💨 Stenon, a Potsdam, Germany-based real-time soil health analysis provider, raised $20m in Series B funding from Pymwymic, Atlantic Labs, DeepTech & Climate Fonds (DCTF), Founders Fund, Oyster Bay Ventures, and other investors.

✈️ Mako, a Sydney, Australia-based drag reduction technology developer for the aviation industry, raised $19m in Series A funding from Virescent Ventures, Grok Ventures, International Airlines Group (IAG), IP Group, Skip Capital, TreeArc Investment Group, and other investors.

🚗 Alva Industries, a Trondheim, Norway-based electric motor developer, raised $18m in Series A funding from Emerald Technology Ventures, Nysnø, Sandwater, EnvisionTech, and Statkraft Ventures.

🔋 BatX Energies, a Gurgaon, India-based lithium-ion battery recycler, raised $11m in Series A funding from IvyCap Ventures, Excel Industries, JITO Incubation and Innovation Foundation, Mankind Group Family Office, and Zephyr Peacock India.

⚡ Arcturus, a Los Angeles, CA-based nanomaterial-infused metals developer, raised $8m in Seed funding from Initialized Capital, 1517 Fund, Breakthrough Energy Discovery, Toyota Ventures, and Wireframe Ventures.

⚒️ Altillion, a Houston, TX-based direct lithium extraction technology developer, raised $5m in Seed funding from EIC Rose Rock and Flathead Forge.

🏭 Digiclean, a Borås, Sweden-based developer of AI sensors for industrial fluid monitoring and efficiency, raised $2.9m in Seed funding from Almi Invest GreenTech, Unconventional Ventures, Feminvest Ventures, Impact Shakers, and S-E Bankens Utvecklingsstiftelse.

⚡ Archimede, a Siracusa, Italy-based developer of off-grid infrastructure monitoring solutions, raised $1.7m in Seed funding from Primo Capital, 40Jemz Ventures, CDP Venture Capital, ELIS Group, Irritec, and other investors.

🏠 Albatross Energetics, a Mumbai, India-based energy-efficient industrial air conditioning designer, raised $1.1m in Seed funding from Transition Ventures.

Project Finance / Debt

⚡ Vena Energy, a Singapore, Singapore-based Asia-Pacific renewable energy independent power producer, raised $483m in PF Debt funding from BNP Paribas, Bank of China, DBS Bank, ING Group, Intesa Sanpaolo and other investors.

⚡ British Solar Renewables, a Shepton Mallet, England-based solar project developer, raised $173m in Debt funding from Eiffel Investment Group.

🌾 InSoil, a Vilnius, Lithuania-based financial solutions provider for sustainable agriculture, raised $137m in Debt funding from Pollen Street Capital.

⚡ OX2, a Stockholm, Sweden-based solar and wind project developer, raised $73m in PF Debt funding from CaixaBank and Norddeutsche Landesbank (Nord/LB).

Exits

⚡ China Resources New Energy, a Shenzhen, China-based wind and solar developer, announced an IPO raising $3.6bn at an implied valuation of $20bn.

🛵 Lime, a San Francisco, CA-based shared electric micromobility solutions provider, announced an IPO raising $167m at an implied valuation of $1.7bn.

🔋 Green Energy Storage, a Breda, Netherlands-based BESS project developer, was acquired by Vopak for an undisclosed amount.

☀️ DAS Solar, a Quzhou, China-based photovoltaic module and systems developer, was acquired by TCL Zhonghuan for an undisclosed amount.

🥩 BettaFish, a Berlin, Germany-based plant-based alternative seafood producer, was acquired by Bayou Best Foods for an undisclosed amount.

💨 NovoNutrients, a Sunnyvale, CA-based gas-fed microbial protein producer, was acquired by Biosphere for an undisclosed amount.

This is a sample of deals available for Currence clients. Can’t get enough deals?

Reading List

⚖️ A federal appeals court rejected the EPA's move to scuttle Biden-era rules toughening air quality standards for soot particles from coal-fired power, construction, tailpipes, and wildfires. [Link]

A rare court win for the environment, and a reminder that regulation rollbacks require actual legal process to survive. The soot standard has significant downstream implications, from coal plant retirements to distributed generation permits at data center sites, so keeping it intact matters.

⚖️ The Supreme Court ruled the president can dismiss heads of independent agencies without cause, locking in what Trump already did to the NRC. [Link]

Short-term bullish for advanced nuclear: the NRC is moving faster and Part 57 is progressing. However, the long-term risk is more subtle, a regulator perceived as partisan loses safety credibility domestically and internationally, which matters for US nuclear exports. And it’s not just the NRC, it also could apply to FERC, especially as ratemaking and energy affordability becomes a hot button issue.

💧 Air Products walked away from its Louisiana blue hydrogen project, while finalizing a green ammonia offtake deal with Yara from NEOM's Saudi Arabia hub. [Link, Link]

The economics of large US low-carbon hydrogen projects aren't holding without policy support that the scrapped Biden-era 45V rules can no longer provide anymore, while the biggest green ammonia buildout in the world (NEOM) is landing its offtake despite delayed timelines. Yara-NEOM is also the first major green ammonia offtake at real scale.

🌐 Google's 2026 Environmental Report is out, showing operational emissions down 2% YoY despite a 37% jump in electricity demand, its largest load growth ever. Also jumping, Scope 3 supply chain emissions by 25%. [Link]

Google signed a record 12 GW of net-new clean energy in 2025 (8x its 2019 total) and cut per-prompt Gemini energy by 33x, which is how it decoupled ops emissions from AI growth. But data center construction alone hit 2.3M tCO2e (20% of ambition-based Scope 3).

🏛 Washington State moved to link its carbon market with California and Québec's WCI system. [Link]

Linking these North American carbon markets creates a larger, more liquid market and gives WA compliance entities access to CA's deeper offset supply.

📊 Terraset published a sharp piece on how biochar is finally becoming bankable. [Link]

Biochar has been the workhorse of near-term durable CDR but has struggled to attract project finance the way DAC and BiCRS have. Terraset’s interesting case study shows how underwriting could catch up, with standardized methodologies and long-tenor offtake are converging.

🌏 Venture Climate Alliance released a market profile of Singapore for portfolio companies considering expansion, covering structural benefits and government incentives. [Link]

Singapore keeps coming up. This guide shows climate founders how to play: the grants are generous, the positioning is uniquely valuable as an ASEAN gateway, but you need people on the ground to work the system.

⏰ The IRA/OBBBA Section 45Y/48E construction-start deadline for wind and solar is here. Projects must have begun physical construction (or clear the 5% safe harbor) by July 5 to qualify. [Link]

💨 Deep Sky delivered North America's first DAC-issued carbon credits, a milestone for the Canadian carbon removal buildout. [Link]

Opportunities & Events

📅 Climate Communications Series: Everything Is an Energy Story: Register for a webinar on July 15th at at 1:00 PM EST and hear from leading journalists at TIME, Associated Press, and HEATED about how they’re approaching energy and climate coverage in 2026.

📅 Aspen Ideas: Climate: The solutions-focused conference hosted by the Aspen Institute and Chicago Climate Corps spans mainstage plenaries, panels, workshops, private roundtables, and city excursions, from July 20th – 22nd.

Jobs

VP, Communications @XPrize

Senior Manager / Director, Communications @Carbon Removal Canada

Finance & Ops AI Lead – Associate @Keyframe

Energy & Climate Policy Engagement Lead @Coreweave

📩 Feel free to send us deals, announcements, or anything else at hello@ctvc.co. Have a great week ahead!