Looking to the future, what lies in store for the packaging industry? The quickly changing landscape of geopolitics and trade, along with the continued growth of e-commerce and ongoing sustainability expectations, indicate two materials will come out as clear winners: paper and flexible plastics.

That’s according to Boston Consulting Group (BCG) in ‘Flexible by Design: The New Playbook for Packaging in North America.’ BCG ran extensive quantitative modelling of product categories and packaging types to map what they see as growing megatrends. They believe packaging industry leaders will future-proof their portfolios, build more agile and resilient supply chains, get smarter about pricing and push sustainable innovation forward, ideally by collaborating across the value chain, not going it alone.

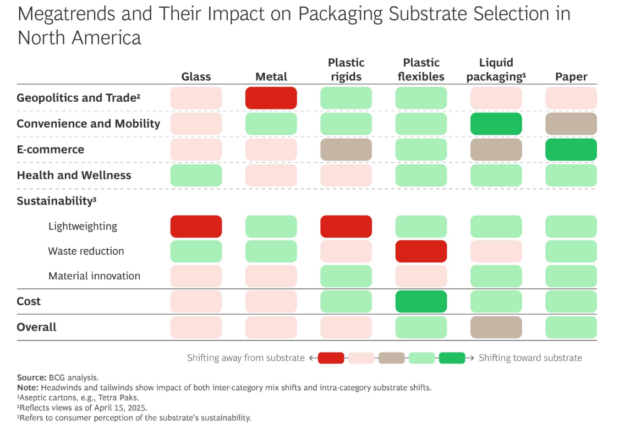

Chart courtesy Two Sides North America.

BCG researchers identified what they call ‘major’ megatrends, driven by long-term economic and structural shifts, that will reshape North America’s packaging industry over the next five to 10 years. These will change not just what packaging is made of, but also how companies think about innovation. While cost and performance still matter, they no longer are the only factors in material decisions. The next packaging choices will be shaped by a much more complicated mix of forces already in play, some of which may seem contradictory:

Global trade

Rules are shifting and the packaging industry is feeling it. While tariff outcomes are still evolving, one thing is clear: their impact on global trade and on packaging costs will be lasting. As protectionism and regionalization continue to grow, companies are being forced to rethink how and where they source materials. That’s pushing many to diversify suppliers, swap out substrates and revisit long-standing packaging choices.

Convenience and mobility

Convenience is still king for North American consumers. Busier, more mobile lifestyles are driving demand for packaging that’s easy to use and take on the go, including resealable packs, single-serve formats and ready-to-use products. At the same time, unit sizes are getting smaller, which often means more packaging overall, even as individual packages shrink.

E-commerce

As online shopping keeps growing, packaging has to do double duty: it needs to protect products through shipping, while also acting as part of the brand experience when the box shows up at the door. That’s fuelling demand for simpler, sturdier and more sustainable packaging, cutting down on excess materials while still delivering a great ‘unboxing’ experience.

Health and wellness

Health-conscious consumers are changing what they buy, favouring options that feel fresher and better for them. That shift is influencing packaging, too. Formats need to preserve freshness and product integrity, especially for food, supplements and cosmetics, while avoiding materials consumers associate with health risks, like microplastics. The result is growing demand for stronger barrier performance and safer-perceived materials.

Sustainability

Sustainability continues to be a top priority for global brands. Across substrates, one trend stands out: increased use of post-consumer recycled content. The real challenge for packaging players is making all of this work at scale without sacrificing performance or blowing up costs.

Paper vs. plastic

How are these megatrends changing real-world packaging decisions? To find out, BCG built quantitative models across more than 350 product categories and 50 packaging formats in eight end markets. They paired that analysis with hands-on expertise in climate policy and tariff legislation to see how each trend would play out across major packaging materials.

The big takeaway was that paper and flexible plastic will come out ahead. While sustainability concerns continue to put pressure on plastic, its cost and performance keeps it a strong paper competitor. For paper, the key barrier continues to be innovation; can the industry scale cost-competitive barrier technologies? If this proves doable, paper adoption could potentially accelerate, especially in food and beverage.

Zooming out to a bird’s-eye view, a few clear patterns start to emerge. The growing concern by consumers regarding plastic’s low circularity rate and microplastic pollution is a significant contributor. Over time, BCG predicts paper will steadily take shares from plastic.

Two Sides North America (TSNA) is a member-supported non-profit advocacy organization for the graphic communications, paper and paper-based packaging industries. For more information, visit www.twosidesna.org.